It’s gotten to the point that pretty much everyone is now aware of the risks. Public surveys, market behavior, on and on, hardly anyone outside politics thinks the economy is in a good place. Gasoline, sentiment, whatever, Euro$ #5 in total is much more than what’s shaping up inside the American boundary. Globally synchronized of which the US is proving to be a close part. The destination, or depth, really, is what’s left to argue. As noted yesterday, even President Joe Biden has taken to talking down economic expectations. . He singled out the labor market, in particular, for the reasons I discussed – making him President Phillips from here on. In consultation with the rate-hikers at the Fed, he’s been coached into the Phillips Curve – pretending that the

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, currencies, economy, employment, Featured, Federal Reserve/Monetary Policy, Joe Biden, Labor market, manufacturing, Markets, newsletter, payrolls, Unemployment

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| It’s gotten to the point that pretty much everyone is now aware of the risks. Public surveys, market behavior, on and on, hardly anyone outside politics thinks the economy is in a good place. Gasoline, sentiment, whatever, Euro$ #5 in total is much more than what’s shaping up inside the American boundary. Globally synchronized of which the US is proving to be a close part.

The destination, or depth, really, is what’s left to argue. As noted yesterday, even President Joe Biden has taken to talking down economic expectations. |

. |

He singled out the labor market, in particular, for the reasons I discussed – making him President Phillips from here on.

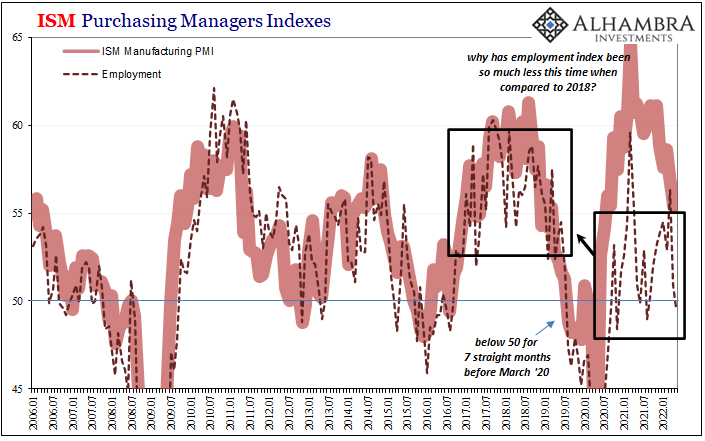

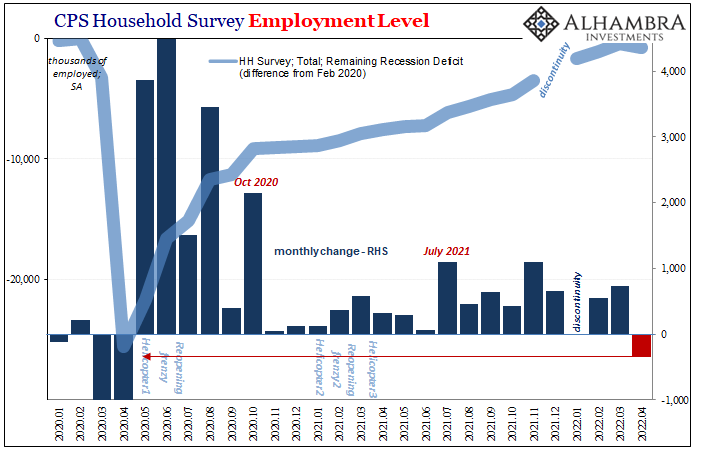

The slowdown part now inarguable, wouldn’t you know it, the prospects for serious downturn have already shown up in a variety of domestic labor data. I cited the most recent ISM figures for employment (less than 50) to go along with the first decline in the BLS Household Survey (in April) since 2020 (the May estimates will be released tomorrow, and it wouldn’t be at all surprising nor inconsistent if the HH figure rebounded). |

. |

. |

|

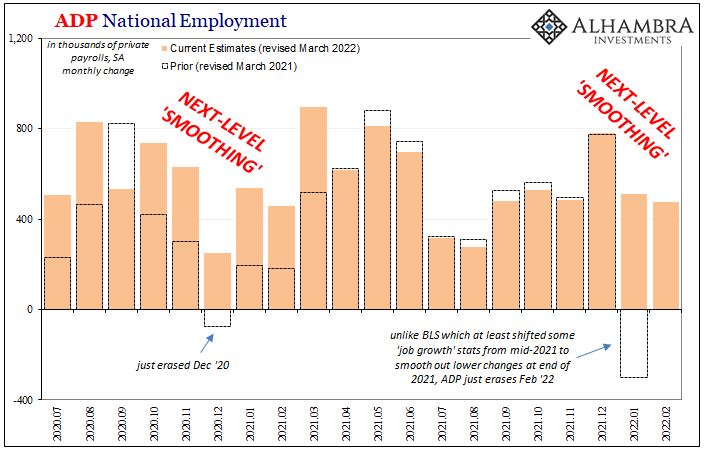

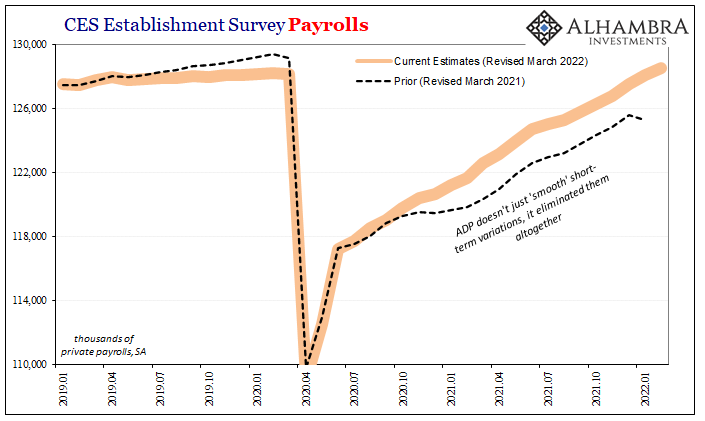

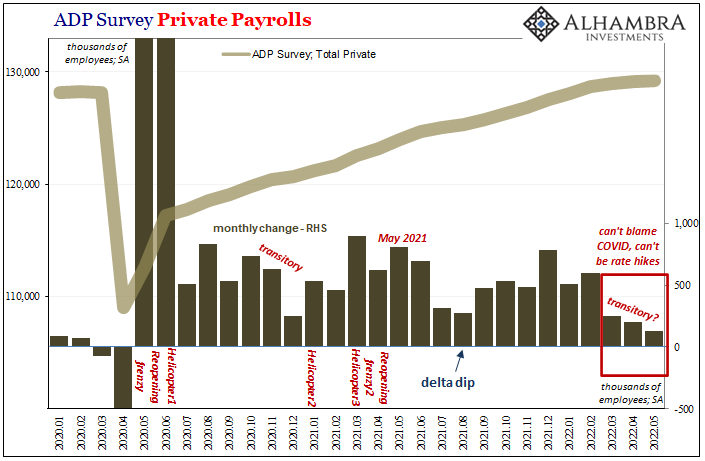

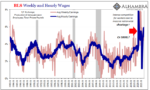

| Today we add ADP – though we do so acknowledging how we have to take it with huge grains of benchmark salt. This particular data series had done this before, pointing to a material labor market slowdown only to completely revise it away trying to catch up and stay up with discontinuities in the BLS’s CPS (you can read about those here).

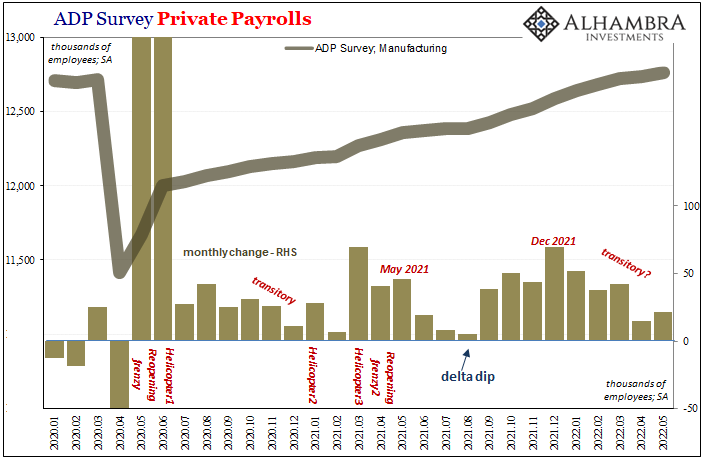

A key piece of this new slowdown in ADP data begins with, sure enough, recent revisions (not benchmarks) especially to the March 2022 estimate (reduced by more than 200,000). A similar-sized downward revision for April with now a low in May, a gain of just 128,000, lowest since April 2020, and Biden’s forecast is looking good months before he made it. Increasing uncertainty, at least, is apparent in the ADP data for manufacturing jobs, too, despite the fact the goods economy is supposed to be still on a tear. |

. |

| On the contrary, manufacturing employment has struggled all along before this current downshift (blamed on a labor shortage that just doesn’t make sense). |

. |

| And, like Germany’s retail sales crash in April, this can’t be blamed on COVID. It will be attributed to the Putin Price Hike or in some ways tied to the Fed’s inflation-fighting rate hikes and QT, though the hikes had only been first begun back in March and balance sheet runoff yet to commence (they’ll absurdly claim monetary policy tightening “sentiment” and forward guidance had been working from late last year).

But even the reason (Euro$ #5), to some degree, is now beside the point. Instead, as the chances of this downside approach certainty, any leftover consideration is, as I started, about how far down. The official political view is that any slowdown is a good thing, a necessary development to Phillips Curve the crap out of inflation while starting the fight from a good place. |

. |

. |

|

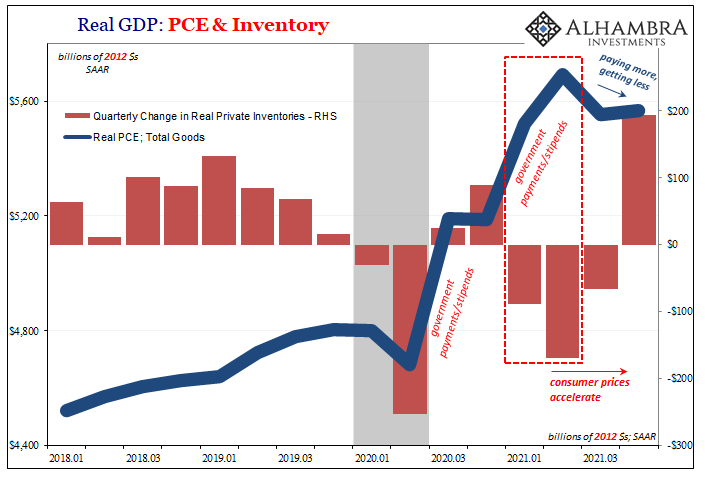

All the actual data, however, shows that “inflation” instead had played a central role in keeping the economy’s rebound from doing any better than insufficient.

Currently, analysts are expecting Establishment Survey payrolls to have downshifted, too, though not quite all the way to the 150,000 per month pace President Phillips had cited. Updated data, including, provisionally, ADP, suggests that’s just the best-case scenario and not all that probable of one. |

. |

You Might Also Like

President Phillips Emerges To Reassure On Growing Slowdown

President Phillips Emerges To Reassure On Growing Slowdown

2022-06-02

Just the other day, President Biden took to the pages of the Wall Street Journal to reassure Americans the government is doing something about the greatest economic challenge they face. Biden says this is inflation when that’s neither the actual affliction nor our greatest threat.

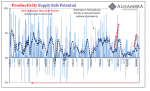

Neither Confusing Nor Surprising: Q1’s Worst Productivity Ever, April Decline In Employed

2022-05-13

Maybe last Friday’s pretty awful payroll report shouldn’t have been surprising; though, to be fair, just calling it awful will be surprising to most people. Confusion surrounds the figures for good reason, though there truly is no reason for the misunderstanding itself. Apart from Economists and “central bankers” who’d rather everyone look elsewhere for the real problem.

Worry Walls Don’t Explain Repeated Falls

Worry Walls Don’t Explain Repeated Falls

2022-04-09

Someone once said that the stock market is always climbing a wall of worry. Maybe that had been true in some long-ago day, but whether or not it might nowadays is beside the point. The nugget of truth which makes the prosaism memorable is the wall rather than the climber. There’s always something going on somewhere to get worked up over.

For The Fed, None Of These Details Will Matter

For The Fed, None Of These Details Will Matter

2022-03-06

Most people have the impression that these various payroll and employment reports just go into the raw data and count up the number of payrolls and how many Americans are employed. Perhaps the BLS taps the IRS database as fellow feds, or ADP as a private company in the same data business of employment just tallies how many payrolls it processes as the largest provider of back-office labor services.That’s just not how it works, though. In fact, sampling and statistical processing first, and then something called trend-cycle (cringe). Benchmarking is in many ways about just this; subjectively estimating the “baseline” economic trend and then for the high frequency data marking up or down any monthly changes from it (I’m oversimplifying on purpose). For employment data more than any other

Taper Discretion Means Not Loving Payrolls Anymore

Taper Discretion Means Not Loving Payrolls Anymore

2022-01-10

When Alan Greenspan went back to Stanford University in September 1997, his reputation was by then well-established. Even as he had shocked the world only nine months earlier with “irrational exuberance”, the theme of his earlier speech hadn’t actually been about stocks; it was all about money.The “maestro” would revisit that subject repeatedly especially in the late nineties, and it was again his topic in California early Autumn ’97.

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?

2022-01-05

Since the Federal Reserve is not in the money business, their recent hawkish shift toward an increasingly anti-inflationary stance is a twisted and convoluted case of subjective interpretation.

A Global JOLT(s) In July

A Global JOLT(s) In July

2021-12-09

The Bureau Labor Statistics reported today another huge month for Job Openings (JO). According to their methodology (which I still believe is flawed, but that’s not our focus this time), the level for October 2021 (JOLTS updates are for one month further back than payrolls) was a blistering 11.03 million.

The Productive Use Of Awful Q3 Productivity Estimates Highlights Even More ‘Growth Scare’ Potential

The Productive Use Of Awful Q3 Productivity Estimates Highlights Even More ‘Growth Scare’ Potential

2021-12-08

What was it that old Iowa cornfield movie said? If you build it, he will come. Well, this isn’t quite that, rather something more along the lines of: if you reopen it, some will come back to work. Not nearly as snappy, far less likely to sell anyone movie tickets, yet this other tagline might contribute much to our understanding of “growth scare” and its affect on the US labor market.

Tags: currencies,economy,employment,Featured,Federal Reserve/Monetary Policy,Joe Biden,Labor Market,manufacturing,Markets,newsletter,payrolls,Unemployment