Overview: News that the separatists were calling on Moscow for military assistance began the risk-off move, and Russia hitting targets across Ukraine has rippled across the capital markets. Equites have been upended. Most bourses in the Asia Pacific region were off 2%-3%, while the Stoxx 600 in Europe gapped lower and is off around 3.5% in late morning dealings. It is at the lowest level since May last year. US futures are sharply lower, and the S&P 50 is set to extend its losing streak for a fifth session, while the NASDAQ is off for the sixth consecutive session. Benchmark 10-year yields are sharply lower. The 10-year US Treasury yield, which approached 2.0% yesterday fell to almost 1.85% today before stabilizing. European yields are mostly 6-10 bp

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movement, Featured, Hungary, newsletter, Russia, Taiwan, Ukraine, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Overview: News that the separatists were calling on Moscow for military assistance began the risk-off move, and Russia hitting targets across Ukraine has rippled across the capital markets. Equites have been upended. Most bourses in the Asia Pacific region were off 2%-3%, while the Stoxx 600 in Europe gapped lower and is off around 3.5% in late morning dealings. It is at the lowest level since May last year. US futures are sharply lower, and the S&P 50 is set to extend its losing streak for a fifth session, while the NASDAQ is off for the sixth consecutive session. Benchmark 10-year yields are sharply lower. The 10-year US Treasury yield, which approached 2.0% yesterday fell to almost 1.85% today before stabilizing. European yields are mostly 6-10 bp lower. The dollar is rising against all the major currencies but the Japanese yen. The Scandis (~-1.8%) are hit the hardest. Emerging market currencies are under pressure. The Russian rouble is off a little more than 2.7%, while central European currencies are down around 2.5%. After falling by 1.15% yesterday, the JP Morgan Emerging Market Currency Index has shed another 0.35% so far today. Gold is approaching $1975. It finished last week slightly below $1900. Brent crude oil is above $100 a barrel and the April WTI contract extended its advance for the fourth consecutive session and is straddling the $100 mark. US natural gas prices are up over 6% to a three-week high. Europe's Dutch benchmark is up around 30%. The index finished last week around 72.15 and is now around 116.00. Iron ore prices slipped fractionally after rising almost 1.8% yesterday. Copper prices are snapping a four-day decline with a 2% bounce.

Asia Pacific

Australia is willing to tap its fuel reserves held in the US as a coordinated attempt to contain the rise in oil prices is sought. Australia reportedly holds around 1.7 mln barrels in reserves. Japan also suggested it would act in coordination.

Taiwan boosted its growth and inflation forecasts earlier today. The government is giving the central bank an ok to raise rates. GDP is now expected to rise by 4.42% this year (up from 4.15%). Inflation is now projected to be 1.93% (1.61% previously). The government's new forecasts are above the median projections in Bloomberg's survey. Taiwan's CPI stood at 2.8% in January. The core measure, excluding vegetables, fruits and energy rose 2.4% in January, the most since January 2009. The government has capped fuel and gas prices for households. It has also temporarily suspended sales and import duties on key food staples (e.g., corn, wheat, and soy).

The US dollar fell to three-week lows near JPY114.40 in late Asian turnover after initially probing JPY115.00. It recovered toward JPY114.80 in the European morning. Given the "fog of war", the upticks may have largely run their course. The Australian dollar rose to its best level yesterday since mid-January around $0.7285 and slumped to $0.7170 today. The $0.7165 area is the first (38.2%) retracement of the rally that began in late January near $0.6970. The next retracement (50%) is around $0.7125. The $0.7200 area offers a cap now. The greenback initially fell to almost CNY6.3100, a new four-year low before recovering to poke back above CNY6.32. The PBOC dollar fixing met projections (Bloomberg survey) at CNY6.3280. Bloomberg has the trade-weighted basket rising to its best level since at least 2007. A break of CNY6.30 would target CNY6.25 and then CNY6.20.

Europe

Russian forces attacked multiple targets across Ukraine. Russian forces had surrounded Ukraine on three sides, and Ukraine border guards reportedly acknowledged that it was being shelled from five regions, including Crimea and Belarus. Putin vowed to "demilitarize" the country and replace its leaders. Kyiv, the Ukraine capital was under attack. Putin claimed that Russia does not plan to "occupy" Ukraine. Reports indicate that columns of Russian tanks had entered the Luhansk region, and there is an attempt to take Ukraine's Zmiinyi island in the Black Sea. An emergency EU summit is being arranged for later today and the G7 heads of state will reportedly hold a conference call today as well. Russia's MOEX stock index was down more than 40% at one point and is still off more than 27% today. The rouble had fallen almost 6.5% against the dollar. The Moscow Exchange halted trading and the rouble is now off around 3.5% today to bring it cumulative loss to almost 11% since the US warning on February 11 of a Russian attack.

Earlier this week, the central bank of Hungary lifted the base rate to 3.4% from 2.90%. However, the key rate has shifted from the base rate to the one-week deposit rate. The one-week deposit rate was hiked today by 30 bp to 4.60%, in line with expectations. The one-week deposit rate finished last year at 3.8%. It had begun being lifted last June from 0.75%.

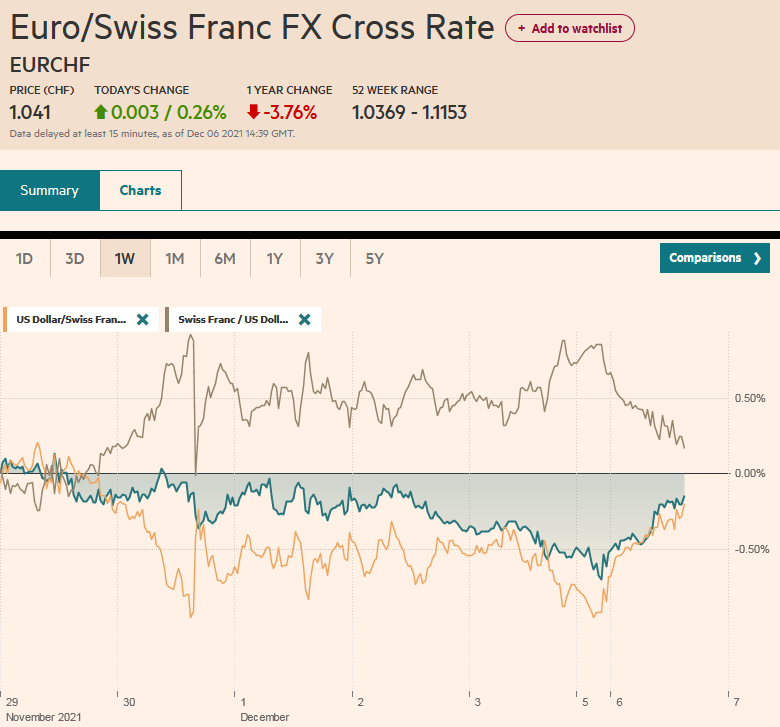

The euro was turned back from $1.14 at the start of the week and is being offered below $1.1170 near midday in Europe. The low set late last month near $1.1120 had not been seen since mid-2020. There is little chart support now ahead of that. Judging from the positioning in the futures market, the trend-following and momentum traders are caught on the wrong side. They had built the largest net long euro position in the futures market since last August. Below there, potential exists toward $1.1000-$1.1050. Sterling has tried repeatedly to establish a foothold above $1.36 with little success. It finished poorly yesterday and has been sold through the $1.35 area to about $1.3420, new lows for the month. The next important technical area is $1.3360-$1.3395. The euro fell below CHF1.03 briefly to record its lowest level in almost seven years.

America

The US announced new sanctions against construction companies and executives involved with constructed the Nord Stream II pipeline. The pipeline had been completed but had not been certified by German authorities and now that process has been suspended. Still, European energy ties to Russia have survived Russia's aggression in Georgia, Moldova, Crimea, and the poisoning of Putin's enemies even outside the country. The Biden administration is going to sell/loan oil from its strategic reserves and is working toward coordinating such efforts.

Geopolitics will overshadow economic factors today. The US reports weekly initial jobless claims. With February nonfarm payrolls to be reported next week and around a 400k increase expected, the weekly jobless claims would not be a likely market mover in any event. Halfway through Q122 revisions to Q4 21 GDP (a little higher on the back of greater inventory accumulation) were also unlikely drivers today. January new home sales soared by nearly 12% in December, so a small pullback in January would not be surprising. Several Fed officials (Barkin, Bostic, Mester, Daly, and Waller) speak today. The market had toyed with the possibility of a 50 bp hike at next month's FOMC meeting. It reached a little above 80% on February 10, the day before the US warned that Russia was prepared to invade Ukraine. There was a 40% chance priced in on Tuesday after Fed Governor Bowman said it was possible. Now it is seen as around a 1-in-5 chance.

The Bank of Canada meets next week, and the swaps market is pricing in a nearly 75% chance that it hikes by 50 bp to initiate the tightening cycle. Its economic calendar is light today. We incorrectly had Mexico's bi-weekly CPI and January retail sales yesterday. They will be reported today. The takeaway is that after easing a bit in recent weeks, Mexico's bi-weekly CPI likely rose again. Without much fiscal support, the economy has had to bear the shocks and the higher interest rates. The economy contracted in Q3 21 and Q4 21.

After repeatedly trying in since late last month, the US dollar finally broke above CAD1.2800. It reached almost CAD1.2830 in the European morning, it best level this year. The next target is the CAD1.2840-CAD1.2850 area. There is a $335 mln option at CAD1.2850 that expires today. Here too, the speculative market appears to have been caught on the wrong side. Non-commercials (speculators) in the futures market have one of the largest net long Canadian dollar positions since last July. The greenback had been spending most of the past six sessions below the 200-day moving average against the Mexican peso (~MXN20.35). The surge of risk-off activity has propelled the US dollar to around MXN20.48, its 20-day moving average. The next technical target is around MXN20.5360. The same risk-off move will likely lift the dollar against the Brazilian real. Yesterday, the greenback slipped below BRL5.0 for the first time since last July. Near-term potential may extend toward BRL5.10.

You Might Also Like

FX Daily, December 6: Semblance of Stability Returns though Geopolitical Tensions Rise

FX Daily, December 6: Semblance of Stability Returns though Geopolitical Tensions Rise

2021-12-06

The absence of negative developments surrounding Omicron over the weekend appears to be helping markets stabilize today after the dramatic moves at the end of last week. Asia Pacific equities traded heavily, and among the large markets, only South Korea and Australia escaped unscathed today.

Market Shrugs Off Chinese Signals and Keeps the Yuan Bid

Market Shrugs Off Chinese Signals and Keeps the Yuan Bid

2021-11-22

Overview: The US dollar has come back bid from the weekend against most currencies following the talk by a couple of Fed governors about the possibility of accelerating the tapering at next month’s FOMC meeting. The weekend also saw protests against the social restrictions being imposed by several European countries in the face of a surge in Covid cases. The Swedish krona, yen, and sterling are the weakest, while the dollar-bloc currencies are resisting the greenback’s tug. Most of the freely accessible and liquid currencies among emerging market currencies, including Russia, Hungary, South Africa, and Mexico, are heavy. At the same time, the Turkish lira recoups a little of the ground lost last week, and the Chinese yuan shrugged off apparently warnings from the PBOC to post its first

Euro Bounces Back, but the Turkish Lira Remains Unloved

Euro Bounces Back, but the Turkish Lira Remains Unloved

2021-11-18

Overview: The US dollar’s sharp upside momentum stalled yesterday near JPY115 and after the euro met (and surpassed) a key retracement level slightly below $1.1300. Led by the Antipodean currencies today, the greenback is mostly trading with a heavier bias. Among the majors, helped by a steadying of US yields, the yen is soft. In the emerging market space, the Turkish lira continues its headlong plunge while the yuan softened and the Mexican peso is off. Hungary’s central bank surprised with a 70 bp hike in the one-week deposit rate. The JP Morgan Emerging Market Currency Index is posting a small gain through the European morning. Disappointing tech results in China (Baidu and Bilibili) weighed on Chinese shares, but most markets in the region fell but Australia and Taiwan.

The Euro and Sterling Remain within Tuesday’s Ranges

The Euro and Sterling Remain within Tuesday’s Ranges

2021-10-22

Overview: A new record high in the S&P 500 yesterday and news that Evergrande had made an interest rate payment failed to lift most Asia Pacific bourses, though Japan and Hong Kong, among the large markets, posted modest gains. The Dow Jones Stoxx 600 is pushing higher in the European morning to put its finishing touches on its third consecutive weekly gain. US tech is trading off, and this is weighing on the NASDAQ futures while the S&P 500 is little changed. The US 10-year yield had probed 1.70% yesterday and is coming back a basis point or two lower. European benchmark yields are mostly a little higher, but soft UK data are helping the Gilts outperform. The Antipodeans are recovering from yesterday’s fall and leading the major currencies higher against the dollar. Sterling is

Dollar Slumps

Dollar Slumps

2021-10-19

Overview: While equities and bonds are firmer, it is the dollar’s sell-off that stands out today. The greenback has retreated broadly.

What to Expect When You are Expecting

What to Expect When You are Expecting

2021-09-22

Overview: The markets have stabilized since Monday’s panic attack but have not made much headway. China and Taiwan returned from the extended holiday weekend. Mainland shares were mixed. Shanghai rose by about 0.4%, while Shenzhen fell by around 0.25%.

How (Not) to Win Friends and Influence People

How (Not) to Win Friends and Influence People

2021-09-13

Overview: There are two big themes in the capital markets today. The first is the ongoing push of the Chinese state into what was the private sector. Today’s actions involve breaking Ant’s lending arms into separate entities, with the state taking a stake. This weighed on Chinese shares and Hong Kong, where many are lists. On the other hand, Japanese markets extended their recent gains.

Tags: #USD,Currency Movement,Featured,Hungary,newsletter,Russia,Taiwan,Ukraine