Social Security is an important part of almost every retirement plan, whether you’ve saved enough or not. That’s why it’s important to know as much about your Social Security situation as possible. And you don’t want to wait until you’re about to retire to gather the facts and take appropriate steps. Social Security planning needs to start 5 years before your target retirement date. Check your estimated benefit amount The easiest way to check Social Security’s estimate of how much you’ll receive is to check online. Go to ssa.gov and create a My Social Security account. This is where you can find: Estimates of how much you’ll receive if you claim benefits early, at your Full Retirement Age (FRA) or at age 70. Your most recent Social Security statement Your

Topics:

Bob Williams considers the following as important: 5.) Alhambra Investments, Featured, Financial Planning, newsletter, retirement income

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Social Security is an important part of almost every retirement plan, whether you’ve saved enough or not. That’s why it’s important to know as much about your Social Security situation as possible. And you don’t want to wait until you’re about to retire to gather the facts and take appropriate steps. Social Security planning needs to start 5 years before your target retirement date.

Check your estimated benefit amount

The easiest way to check Social Security’s estimate of how much you’ll receive is to check online. Go to ssa.gov and create a My Social Security account. This is where you can find:

- Estimates of how much you’ll receive if you claim benefits early, at your Full Retirement Age (FRA) or at age 70.

- Your most recent Social Security statement

- Your eligibility for Social Security

- Your full earnings record according to SSA

There is another benefit of creating a My Social Security account. Once it’s open, no one else can create an account using your Social Security number. Only you can access your information.

Check your earnings record

Since your benefit is based on your earnings record, it’s important to make sure SSA has it right. However, there is a strict time limit on corrections. According to Social Security Handbook:

An earnings record can be corrected at any time up to three years, three months, and 15 days after the year in which the wages were paid or the self-employment income was derived. “Year” means “calendar year” for wages and “taxable year” for self-employment income. If the last day of that period falls on a Saturday, Sunday, legal holiday, or other non-work day for Federal employees set by statute or Executive Order, the period for correction is extended to the end of the next work day.

There are some limited exceptions that allow you to make earnings corrections past the regular time limit. It’s somewhat cumbersome, but here goes.

- To correct an entry established through fraud;

- To correct a mechanical, clerical, or other obvious error;

- To correct errors in crediting earnings to the wrong person or to the wrong period;

- To transfer items to or from the Railroad Retirement Board (if reported to the wrong agency), or to add railroad earnings to Social Security earnings records when the law permits;

- To add wages paid in a period by an employer who made no report of any wages paid to the worker in that period, or if the employer is increasing the originally reported amount for the period;

- To add or remove wages in accordance with a wage report filed by the employer with IRS; or, if a State or local governmental employer, with SSA if the report is filed within the time limitation specified for assessment, refund, or credit under a State’s coverage agreement;

- To add self-employment income in a taxable year if an individual or the individual’s survivor establishes that:

- A self-employment tax return for that year was filed before the time limit ran out; and

- Either no self-employment income for that year has been recorded in the individual’s earnings record, or the recorded self-employment income for that year is less than the amount reported on the self-employment tax return; or

- To add self-employment income for any taxable year up to the amount of earnings that were wrongly recorded as wages and later deleted. This can be done only if a tax return reporting such self-employment income is filed within three years, three months, and 15 days after the taxable year in which the earnings wrongly recorded as wages were deleted. The self-employment income must:

- Be for the same taxable year as the year in which the wages were removed; and

- Have already been included on the individual’s Social Security record.

- Prior to the expiration of the time limit the worker or the worker’s survivor has:

- Applied for benefits and stated that the earnings for a year(s) were incorrect; or

- Requested a revision of his or her earnings record for a year(s).

Decide what age you’ll claim benefits

Retiring and claiming Social Security benefits doesn’t always happen at the same time. Some people decide to wait a while after retiring before they file for Social Security because the longer you wait until age 70 the bigger your benefit. So, deciding when you’ll file is an important part of the planning process.

If you claim your Social Security benefit before your Full Retirement Age (FRA), say 62, you’ll receive a permanently reduced benefit which could be as much as 30 percent less than if you waited until your FRA. If you wait until age 70 to collect, you may receive up to 32 percent more than if you take Social Security at FRA. You can find your Full Retirement Age here.

Create a claiming strategy with your spouse

If you and your spouse are both entitled to Social Security benefits, working together to create a claiming strategy can bring more retirement dollars into your house.

Here’s an example of a couple I know. The wife has not worked outside the home in 20 years. At 63, she claimed a reduced benefit on her own work history and began to receive a monthly benefit. Her husband doesn’t plan to claim benefits until 70, allowing his payout to grow. When he files for his Social Security at 70, the wife will be able to switch from her benefit to a spousal benefit based on the husband’s earnings history. The husband will receive a much larger payment by waiting and the wife’s spousal benefit will more than double what she’d been receiving. That strategy will increase the couple’s total retirement income.

Another strategy is delaying Social Security benefits until 70 for the higher-earning spouse. That spouse receives delayed credits that increase the amount to be received by 8 percent a year between their Full Retirement Age and age 70. Then, if the higher-earning spouse dies, the surviving spouse can collect a survivor’s benefit equal to 100 percent of what the deceased spouse was receiving at death, which includes the delayed credits. If a person collects only the spousal benefit, they’re benefit is based on a percentage of what the other spouse was entitled to at Full Retirement Age and does not include any delayed credits.

Who knew there’s so much to Social Security planning? Strategies vary. And that’s why it’s important to plan ahead. Don’t wait until you’re ready to claim your benefit before you do anything about it.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-03-08

Update March 08 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -1.0 bn. compared to last week, this means the SNB is selling euros and dollars.

The Insatiable Appetite to Tax Social Security Benefits

The Insatiable Appetite to Tax Social Security Benefits

2021-02-09

First, it was 10%, then 20%, and today more than 50% of U.S. retirees pay taxes on their Social Security benefits, and the number is expected to go even higher. The cause seems to be that one government hand doesn’t know, or care, what the other government hand is doing.

Take Advantage of These COVID Estate Planning Opportunities by the End of 2020

Take Advantage of These COVID Estate Planning Opportunities by the End of 2020

2020-12-07

May you live in interesting times. Although that sounds like an ancient blessing, it’s believed to be a Chinese curse casting instability and uncertainty on the person who hears it. Blessing or curse, it’s a great description of the year we’ve just come through, and in spite of all the turmoil, there are some things you can do before the end of 2020 to take advantage of all the madness.

How Much Taxes Will Retirees Owe on Their Retirement Income

How Much Taxes Will Retirees Owe on Their Retirement Income

2020-11-10

Planning for retirement. We spend most of our working career preparing for it, saving for it, covering every contingency. When you finally wave goodbye to the company, you’re ready for all that planning to take over. But does your planning take into account the taxes you’ll have to pay on your retirement income? It’s one of the biggest retirement planning mistakes people make.

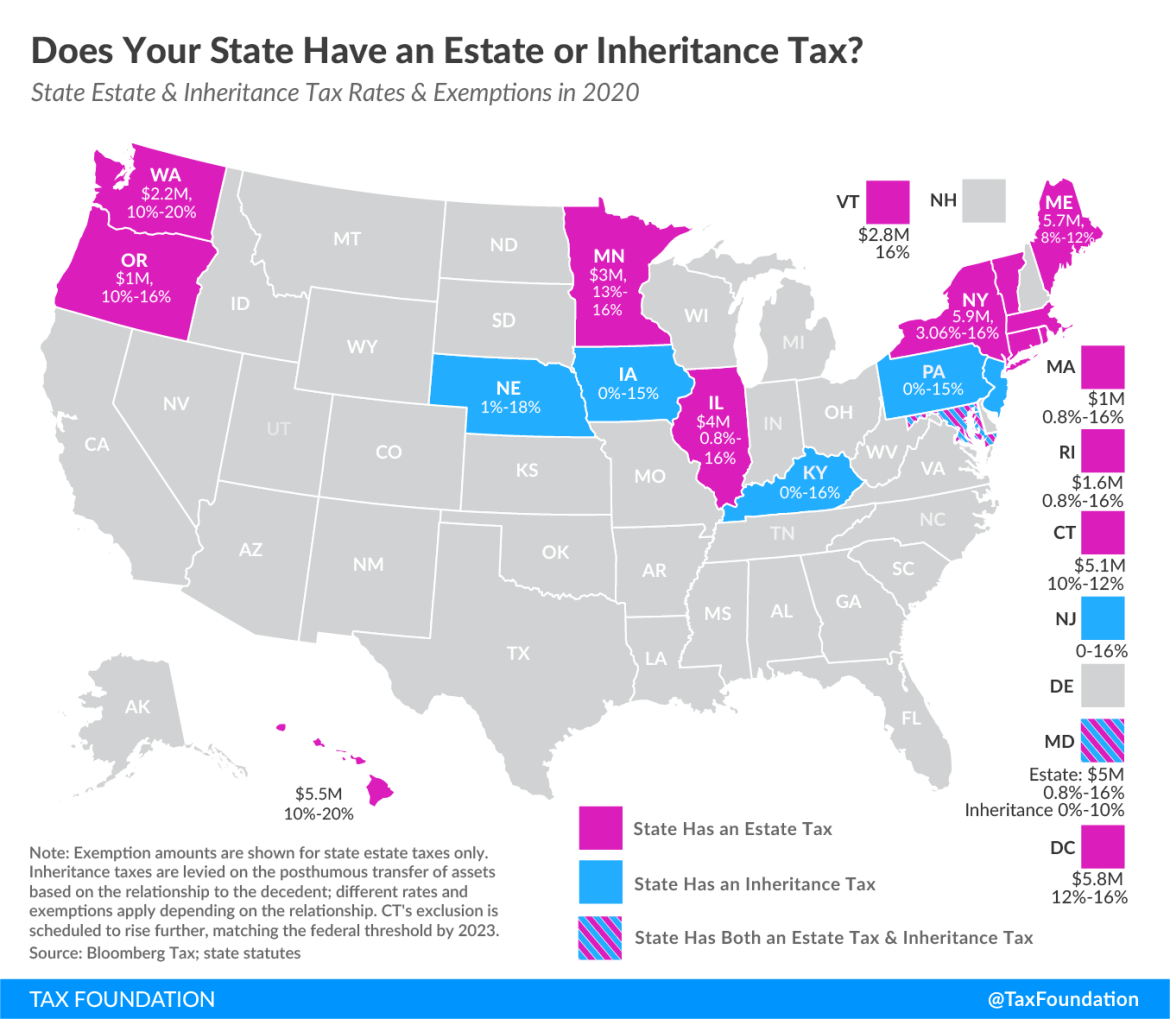

17 States that Charge Estate or Inheritance Taxes

17 States that Charge Estate or Inheritance Taxes

2020-11-03

Death tax, inheritance tax, estate tax—call it what you will, they all mean that some government entity wants to put its hand in your pocket or your heirs’ pockets, after your demise.

5 Estate Planning Myths That Can Derail Your Estate Plan

5 Estate Planning Myths That Can Derail Your Estate Plan

2020-10-18

You spend a lifetime earning, saving, acquiring. But the old adage is true—you can’t take it with you. So, what do you do with your assets when you’re gone? How do you want them distributed? That’s where a good estate plan comes in.

Reopening Inertia, Asian Dollar Style (Still Waiting On The Crash)

Reopening Inertia, Asian Dollar Style (Still Waiting On The Crash)

2020-09-20

Why are there still outstanding dollar swap balances? It is the middle of September, for cryin’ out loud, and the Federal Reserve reports $52.3 billion remains on its books as of yesterday.

12 States That Keep Retirement Dollars in Your Pocket

12 States That Keep Retirement Dollars in Your Pocket

2020-09-18

“Will I outlive my money?” That’s one of the biggest concerns for most retirees. There’s the high cost of medical care, which gets more expensive all the time. There’s inflation, which raises the cost of goods and services, eating into your retirement budget.

Tags: Featured,Financial Planning,newsletter,retirement income