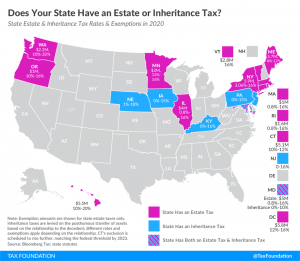

In 2012, the American Taxpayer Relief Act (ATRA) established, for the first time, a permanent estate tax and gift tax exemption. The exemption is the amount an individual can pass on at death without paying estate taxes. The legislation set the exemption at $5 million per person, indexed for inflation.

Five years later, Congress decided the exemption was not large enough and passed the Tax Cuts and Jobs Act of 2017 (TCJA), which increased the lifetime exemption amount to $11,180,000 per person. As with the previous legislation, the new exemption was indexed for inflation.

Coming up in 2023, the new exemption amount will take a substantial jump to $12,920,000 per person or $25,840,000 per couple, up from the $12,060,000 and $24,120,000 respectively that were

The IRS Will Tax Less of an Estate in 2023

November 17, 2022