Stop me if you’ve heard this before: About US5 billion (about SDR 193 billion) of the new allocation will go to emerging markets and developing countries, including low-income countries. This from the IMF’s July 30, 2021, statement gleefully announcing its governing body(ies) has(d) agreed to a general allocation of 0 billion in SDR’s, biggest in history, according to existing quotas. The purpose: “to boost existing liquidity.” This really does sounds very familiar: The equivalent of nearly US0 billion of the general allocation will go to emerging markets and developing countries, of which low-income countries will receive over US billion. The latter taken from the IMF’s August 13, 2009, statement giddily announcing its governing body(ies) has(d)

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, currencies, economy, EuroDollar, Featured, Federal Reserve/Monetary Policy, global reserve currency, IMF, Markets, newsletter, quota, SDR

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Stop me if you’ve heard this before:

About US$275 billion (about SDR 193 billion) of the new allocation will go to emerging markets and developing countries, including low-income countries.

This from the IMF’s July 30, 2021, statement gleefully announcing its governing body(ies) has(d) agreed to a general allocation of $650 billion in SDR’s, biggest in history, according to existing quotas. The purpose: “to boost existing liquidity.”

This really does sounds very familiar:

The equivalent of nearly US$100 billion of the general allocation will go to emerging markets and developing countries, of which low-income countries will receive over US$18 billion.

| The latter taken from the IMF’s August 13, 2009, statement giddily announcing its governing body(ies) has(d) agreed to a general allocation of $250 billion in SDR’s, biggest in history [to that point], according to existing quotas. The purpose: “to provide liquidity to the global economic system by supplementing Fund’s member countries’ foreign exchange reserves.”

Sure, eleven years in between means a lot can happen; and a lot did, that’s the problem. It was nothing the 2009 SDR’s solved, though it was a near-continuous stream of international monetary illiquidity. These unjoyful IMF accounting conventions were supposed to aid particularly emerging and low-income nations who suffer most when international money grows scarce (leaving their economies starved for legit economic growth and all the debt problems this condition amplifies). A quarter-trillion in ’09 was a huge number, like all the others thrown around back then from ARRA to numerous QE’s. And now, just like ARRA and the QE’s, the SDR allocations have to be repeated, too. |

. |

| Because they worked so well?

Ahem.

If it was a matter of raw survival in 2016, what can it be in 2021? The IMF would have you believe this is a wonderful development, a serious expansion of monetary capacities for nations all around the world. Rich and poor. |

. |

Mere sophistry, the raise of purposefully huge numbers to tickle the emotions of the unaware (practically the entire planet, including all those in position of authority mentioned here; sophistry born from desperation bred of ignorance and repeated failure).

Which private bank in Africa will be supported by the latest SDR193 billion sent to the world’s poorest countries? That bank – unable to secure dollars – will do what?

After an unusually terse period of financial and economic destruction, joined by others in its same situation, the bank can appeal to its government or central monetary authority who, having no dollars, either, are the only ones to whom SDR’s are made available. Authorities will mark down on their books that their devastating national current dollar shortfall was covered in transition to another in the same situation by a “currency” neither banks nor their customers anywhere in any part of the real economy or financial system has any use.

Liquidity doesn’t mean what they think it means, apparently.

When a rush of private banks in poor countries are further deprived of eurodollars, they’ll create such a mess that the IMF will enter if only afterward to make a big splash of SDR’s being deployed on some official level far, far away from the monetary playing fields of useful currency. What’s the difference between IMF SDR’s, once likewise depleted, and the botched dollar rescues at Argentina? A different name for the same unfixable problem.

No wonder money-deprived El Salvador is serious about Bitcoin (even after consulting earlier with…the IMF).

How else did Euro$ #2 then #3 followed by #4 and then a second GFC all occur, and viciously harm the poorest countries the most, with that first ’09 quarter trillion available to all? It was sitting there in the pot last March, too.

SDR’s aren’t useful liquidity any more than US$ bank reserves. Both equally proved in fact by these very same eleven years in between the last quota dodge and the current one. Pure sophistry. But that, again, is the point.

You Might Also Like

SNB Sight Deposits: Inflation Fear Decreasing, SNB Selling Euros

SNB Sight Deposits: Inflation Fear Decreasing, SNB Selling Euros

2021-08-04

Sight Deposits have fallen: The change is -0.2 bn. compared to last week, this means the SNB is selling euros and dollars.

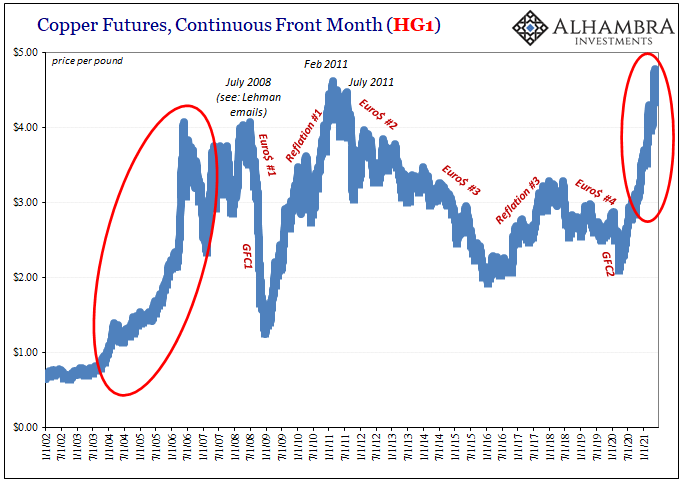

Copper Corroding PPI

Copper Corroding PPI

2021-06-17

Yesterday, lumber. Today, copper. The “doctor” has been in reverse for better than two months now, with trading in the current session pounding the commodity to a new multi-month low. Down almost $0.19 for the day, an unusual and eye-opening loss, this brings the cumulative decline to 9.2% since the peak way back on May 11.

Rechecking On Bill And His Newfound Followers

Rechecking On Bill And His Newfound Followers

2021-04-09

The benchmark 10-year US Treasury has obtained some bids. Not long ago the certain harbinger of bond rout doom, the long end maybe has joined the rest of the world in its global pause if somewhat later than it had begun elsewhere (including, importantly, its own TIPS real yield backyard).

Real Dollar ‘Privilege’ On Display (again)

Real Dollar ‘Privilege’ On Display (again)

2021-04-08

Twenty-fifteen was an important yet completely misunderstood year. The Fed was going to have to become hawkish, according to its models, yet oil prices crashed and the dollar continued to rise. Both of those things were described as “transitory” by Janet Yellen, and that they were helpful or positive (rising dollar means cleanest dirty shirt!), but domestically American policymakers’ clear lack of conviction and courage about that rate hike regime showed otherwise.

JOLTS Revisions: Much Better Reopening, But Why Didn’t It Last?

JOLTS Revisions: Much Better Reopening, But Why Didn’t It Last?

2021-03-12

According to newly revised BLS benchmarks, the labor market might have been a little bit worse than previously thought during the worst of last year’s contraction. Coming out of it, the initial rebound, at least, seems to have been substantially better – either due to government checks or, more likely, American businesses in the initial reopening phase eager to get back up and running on a paying basis again.

There’s Two Sides To Synchronize

There’s Two Sides To Synchronize

2021-03-03

The offside of “synchronized” is pretty obvious when you consider all possibilities. In economic terms, synchronized growth would mean if the bulk of the economy starts moving forward, we’d expect the rest to follow with only a slight lag. That’s the upside of harmonized systems, the period everyone hopes and cheers for.

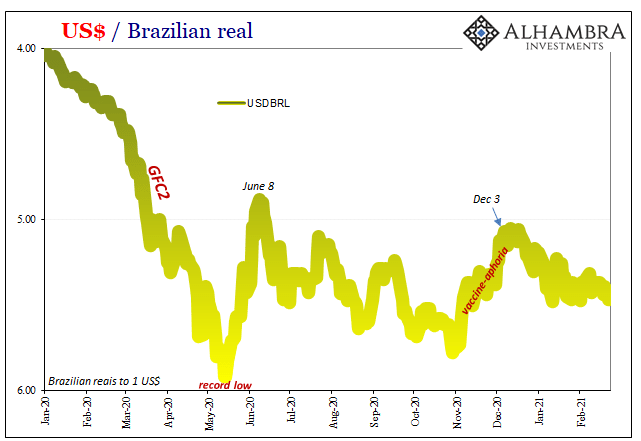

For The Dollar, Not How Much But How Long Therefore How Familiar

For The Dollar, Not How Much But How Long Therefore How Familiar

2021-02-24

Brazil’s stock market was rocked yesterday by politics. The country’s “populist” President, Jair Bolsonaro, said he was going to name an army general who had served with Bolsomito (a nickname given to him by supporters) during that country’s prior military dictatorship as CEO of state-owned oil giant Petróleo Brasileiro SA. Gen. Joaquim Silva e Luna is being installed, allegedly, to facilitate more direct control of the company by the federal government.With the economy still gripped by the latest recession, and oil prices rising worldwide as supplies continue to be squeezed, Brazilians have been caught in the vise between fuel prices and unemployment – pure misery for a nation still reeling from Euro$ #3’s (2014-16) crushing impacts. A depression for years before COVID…and now this.

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

2021-02-19

It’s worth taking a look at a couple of extremes, and the putting each into wider context of inflation/deflation. As you no doubt surmise, only one is receiving much mainstream attention. The other continues to be overshadowed by…anything else.

Tags: currencies,economy,EuroDollar,Featured,Federal Reserve/Monetary Policy,global reserve currency,IMF,Markets,newsletter,quota,SDR