This is likely to be one of the most eventful weeks we’ve had in a while. Not only do three major central banks meet, but four EM central banks also meet, and we get important June and July data from the US, the first Q2 GDP reading from China, an OPEC+ meeting, and an EU summit. This comes as markets are grappling with still-rising virus numbers in the US and resurgent numbers in many other countries that call into question the durability of the economic recovery. With so many events impacting virtually all assets, we expect a volatile week ahead for the markets and may serve as a gut punch to risk assets like EM. AMERICAS Colombia reports May manufacturing production and IP Wednesday. The former is expected to contract -28.0% y/y and the latter by -28.7% y/y.

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, emerging markets, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

![]() This is likely to be one of the most eventful weeks we’ve had in a while. Not only do three major central banks meet, but four EM central banks also meet, and we get important June and July data from the US, the first Q2 GDP reading from China, an OPEC+ meeting, and an EU summit. This comes as markets are grappling with still-rising virus numbers in the US and resurgent numbers in many other countries that call into question the durability of the economic recovery. With so many events impacting virtually all assets, we expect a volatile week ahead for the markets and may serve as a gut punch to risk assets like EM.

This is likely to be one of the most eventful weeks we’ve had in a while. Not only do three major central banks meet, but four EM central banks also meet, and we get important June and July data from the US, the first Q2 GDP reading from China, an OPEC+ meeting, and an EU summit. This comes as markets are grappling with still-rising virus numbers in the US and resurgent numbers in many other countries that call into question the durability of the economic recovery. With so many events impacting virtually all assets, we expect a volatile week ahead for the markets and may serve as a gut punch to risk assets like EM.

AMERICAS

Colombia reports May manufacturing production and IP Wednesday. The former is expected to contract -28.0% y/y and the latter by -28.7% y/y. The central bank cut rates 25 bp to 2.5% last month, slowing the pace from 50 bp cuts previously amidst rising concerns about capital outflows. The vote was 5-2, with the two dissents in favor of a 50 bp cut. Next policy meeting is July 31 and another 25 bp cut is expected. However, the language will be very important in determining how much more easing may be in the pipeline. May trade data will be reported Friday.

Chile central bank meets Wednesday and is expected to keep rates steady at 0.50%. At its last meeting June 16, the bank kept rates steady but increased its credit line to local banks to boost lending. Minutes from that meeting suggest the policy rate will remain at its technical minimum for longer than initially estimated, and that any further easing will come from unconventional measures. CPI rose 2.6% y/y in June, the lowest since October and in the bottom half of the 2-4% target range.

EUROPE/MIDDLE EAST/AFRICA

Turkey reports May current account and IP data Monday. The current account is expected to be in deficit by -$3.75 bln, while IP is expected to contract -24.0% y/y vs. -31.4% in April. The economy remains weak but the central bank surprised markets at its last meeting June 25 by leaving rates unchanged at 8.25%. Inflation accelerated further to 12.62% y/y in June and so it seems likely that the bank will remain on hold again at the next meeting July 23.

Israel reports June trade Monday. CPI will be reported Wednesday. Headline inflation is expected at -1.0% y/y vs. -1.6% in May. If so, it would be the first “acceleration” since December but would be the third straight month of deflation and well below the 1-3% target range. The Bank of Israel just met and expanded its QE to include corporate debt. Next policy meeting August 24 and further easing measures are possible if the shekel remains firm. The bank may also step up its intervention to weaken the currency. However, we do not expect the bank to go negative.

National Bank of Poland meets Tuesday and is expected to keep rates steady at 0.10%. After surprising markets with a 40 bp cut in May, the bank kept rates steady in June and sounded a bit more upbeat. For now, we think the bank will remain in wait and see mode. Poland also reports May trade and current account data Tuesday. Minutes will be released Thursday and its quarterly inflation report will be released Friday.

South Africa reports June CPI Wednesday. Headline inflation is expected to fall to 2.2% y/y vs. 3.0% in May. If so, it would be the lowest since September 2004 and below the 3-6% target range. This will be followed by June PPI Thursday, where headline inflation is expected at -0.1% y/y vs. 1.2% in May. This would point to further deflation ahead at the consumer level. Next SARB meeting is July 23 and another cut is expected then.

ASIA

India reports June CPI Monday. Headline inflation is expected at 5.32% y/y vs. 5.84% in May. If so, it would be the lowest since October and move further within the 2-6% target range. This will be followed by June WPI Tuesday, which is expected to fall -2.39% y/y vs. -3.21% in May. Next RBI meeting is August 6 and another cut is expected then after cutting 40 bp at the last meeting May 22. June trade data will be reported Wednesday.

Singapore advance Q2 GDP will be reported Tuesday. The economy is expected to contract -11.3% y/y (-36.7% SAAR) vs. -0.7% y/y (-4.7% SAAR) in Q1. June trade will be reported Friday, with NODX expected to rise 4.9% y/y vs. -4.5% in May. The ruling PAP is reeling from a huge drop in support in last week’s elections. It won 83 seats out of a total 93 with 61.2% of the vote. In any other country, this would be considered a huge success, but here in Singapore, it was the PAP’s worst showing ever. The opposition’s 10 seats are the most ever.

China reports June trade data Tuesday. Exports are expected to contract -2.0% y/y and imports by -9.0% y/y. Q1 GDP and June retail sales and IP will be reported Thursday. GDP is expected to rise 2.2% y/y vs. -6.8% in Q1, sales are expected to rise 0.5% y/y vs. -2.8% in May, and IP is expected to rise 4.8% y/y vs. 4.4% in May. Data last week suggest that loan and aggregate financing growth remain robust in response to previous easing measures.

Bank Indonesia meets Thursday and is expected to cut rates 25 bp to 4.0%. It cut rates 25 bp at its last meeting June 18 and said it “sees room for lower interest rates in line with low inflationary pressure.” CPI rose only 1.96% y/y in June, the lowest since May 2000 and below the 2.5-4.5% target range. We expect the bank to continue the easing cycle well into H2, especially in light of the relatively firm rupiah.

Bank of Korea meets Thursday and is expected to keep rates steady at 0.5%. The bank cut rates 25 bp at its last meeting May 28 and suggested it was nearing the lower bound. Governor Lee suggested then that the bank could resort to unconventional measures if further stimulus was needed but offered no further details. Perhaps the bank could clarify its position at this week’s meeting.

You Might Also Like

Risk assets remain hostage to swings in market sentiment. Stronger than expected US jobs data last week was welcome news. However, the tug of war between improving economic data and worsening viral numbers is likely to continue this week, with many US states reporting record high infection rates.

The spread of the coronavirus continues and is likely to weigh on risk assets and EM. Most markets in Emerging Asia are closed for all or part of this week due to the Lunar New Year holiday. China has extended the holiday until February 2 as it struggles to contain the virus.

EM Preview for the Week Ahead

EM Preview for the Week Ahead

EM remains vulnerable to deteriorating risk sentiment as the coronavirus spreads. China announced a series of measures over the weekend to help support its financial markets, but this may not be enough to turn sentiment around yet. China markets reopen Monday after the extended Lunar New Year holiday and it won’t be pretty.

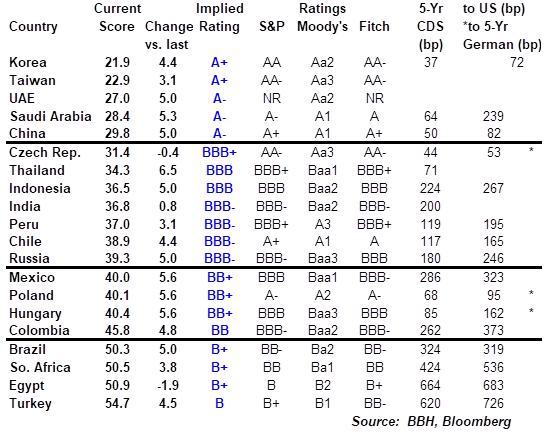

EM Sovereign Rating Model For Q2 2020

EM Sovereign Rating Model For Q2 2020

The major ratings agencies are punishing Emerging Markets (EM) credits much more than their DM counterparts. Our own sovereign ratings model suggests that there is still more pain to come.

We have produced this interim ratings model to assist investors in assessing relative sovereign risk across the major EMs.

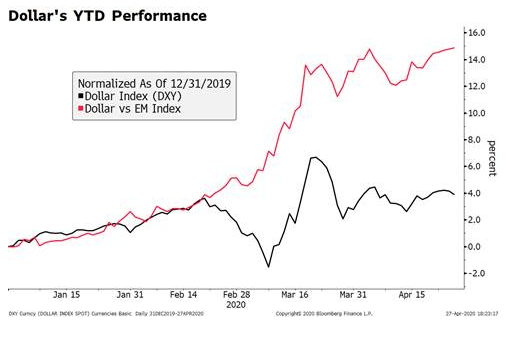

Some Thoughts on Recent Foreign Exchange Intervention

Some Thoughts on Recent Foreign Exchange Intervention

Dollar softness this week will take some pressure off of the foreign currencies but it’s too early to sound the all clear. This piece focuses on how central banks around the world may be intervening to influence their currencies. Most of the world, particularly EM, is grappling with supporting weak currencies but a select few are dealing with stronger currencies. This is a very opaque process and so we are simply making our best guesses.

Risk assets came under pressure last week as the virus news stream worsened. It’s clear that large parts of the US will be forced to delay reopening until their virus numbers improve. Markets had gotten too bullish on the US recovery story and so this reality check soured sentiment. This is a very important week for US data, and we think risk sentiment will remain under pressure ahead of what we think will be a likely downside surprise in the US jobs number Thursday.

Dollar Begins the Week Under Pressure Again

Dollar Begins the Week Under Pressure Again

The virus news stream remains negative; pressure on the dollar has resumed. The US economy is taking a step back just as Q3 is about to get under way; there are some minor US data reports today. UK Labour leader Starmer overtook Prime Minister Johnson in the latest opinion poll; Macron’s party did poorly in French local elections.

Dollar Bid as Market Sentiment Yet to Recover

Dollar Bid as Market Sentiment Yet to Recover

The US has started the formal process of withdrawing from the WHO; the dollar continues to benefit from risk-off sentiment but remains stuck in recent ranges. The White House is asking Congress to pass another $1 trln stimulus plan by early August; President Trump hosts Mexican President AMLO for a two-day visit.

Tags: Articles,Emerging Markets,Featured,newsletter