The virus news stream is mostly positive today; yet risk assets are starting the week under some modest pressure The dollar took a hit last week but we think it will recover; some US data releases from Good Friday are worth repeating With most of Europe closed today, the news stream from the region is very light; oil prices could not extend their gains today after OPEC+ finalized output cuts over the weekend India March CPI is expected to ease to 5.90% y/y from 6.58% in February The dollar is mostly firmer against the majors in thin holiday trading. Sterling and yen are outperforming, while Nokkie and euro are underperforming. EM currencies are mostly weaker. IDR and RUB are outperforming, while TRY and KRW are underperforming. MSCI Asia Pacific was down 0.6% on

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, Daily News, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

- The virus news stream is mostly positive today; yet risk assets are starting the week under some modest pressure

- The dollar took a hit last week but we think it will recover; some US data releases from Good Friday are worth repeating

- With most of Europe closed today, the news stream from the region is very light; oil prices could not extend their gains today after OPEC+ finalized output cuts over the weekend

- India March CPI is expected to ease to 5.90% y/y from 6.58% in February

The dollar is mostly firmer against the majors in thin holiday trading. Sterling and yen are outperforming, while Nokkie and euro are underperforming. EM currencies are mostly weaker. IDR and RUB are outperforming, while TRY and KRW are underperforming. MSCI Asia Pacific was down 0.6% on the day, with the Nikkei falling 2.3%. MSCI EM is down 0.6% so far today, with the Shanghai Composite falling 0.5%. European markets are closed today for Easter Monday, while US futures are pointing to a lower open. 10-year UST yields are flat at 0.72%, while the 3-month to 10-year spread is flat to stand at +54 bp. Commodity prices are mostly lower, with Brent oil down 0.5%, copper up 3.1%, and gold down 0.3%.

The virus news stream is mostly positive today. The WHO confirmed there are 70 coronavirus vaccines in development worldwide, with three already being tested in clinical trials. Elsewhere, new cases in Spain and Italy were the fewest in three weeks. Korea confirmed that it will start exporting test kits to the US starting this week.

Yet risk assets are starting the week under some modest pressure. Perhaps it’s just a correction from last week’s big rally, but it might be something deeper. When all is said and done, the global economy won’t avoid recession and the economic numbers are likely to worsen significantly before they get better.

The dollar took a hit last week but we think it will recover. Last time this happened back in March, the dollar eventually recovered and we see the same dynamic in play now. For DXY, support near the 99.286 is crucial, as a break below would set up a test of the March 27 low near 98.27. That support was tested today but has held.

AMERICAS

Last Thursday, the Fed introduced more stimulus measures. The dollar typically takes a hit when this happens, only to recover later. We’ve seen this dynamic time and time again during this crisis and we believe this will continue to be the case this time. There are no US data releases or Fed speakers today and so trading is likely to be light but choppy.

Some US data releases from Good Friday are worth repeating. March CPI inflation came in lower than expected, with headline at 1.5% y/y and core at 2.1% y/y. Both decelerated from February and this is likely to continue. March budget deficit came in lower than expected at -$119 bln, leading the 12-month total to drop slight to -$1.034 trln. This is likely to be the last “good” number for a long, long time.

EUROPE/MIDDLE EAST/AFRICA

With most of Europe closed today, the news stream from the region is very light. Italy is likely to extend its lockdown to early May, and plans to ask for significant budget deficit deviation due to the impact of the virus. UK Prime Minister Johnson was discharged from the hospital Sunday but said he will not go back to work right away.

In the absence of any fundamental developments, let’s see what the technicals say. The euro’s bounce ran out of steam today near $1.0970, which happens to be the 50% retracement objective of the March-April drop. Markets are thin today and so we may need another day or two to get a clearer signal. Sterling traded at its highest level today since March 13 near $1.2535. The $1.2515 level is key, as it represents the 62% retracement objective of the March drop. Clean break above that would set up a test of the March 9 high near $1.32. The 200-day moving average near $1.2655 currently would likely offer some intermediate resistance.

Oil prices could not extend their gains today after OPEC+ finalized output cuts over the weekend. Perhaps it was because the 9.7 mln bbl/day cut came in below the 10 mln number that was tossed about. Or perhaps it was because the full amount of OPEC+ cuts will only be in effect for two months, tapering to 7.6 mln by end-2020 and then to 5.6 mln by end-2021, which will last until April 2022. Either way, we are seeing some “buy the rumor, sell the fact” price action today. Going forward, much will depend on how deep the global recession turns out to be.

ASIA

India March CPI is expected to ease to 5.90% y/y from 6.58% in February. If so, it would be within the 2-6% target range for the first time since November. WPI will be reported Tuesday and is expected to ease to 1.33% y/y from 2.26% in February, which suggests pipeline price pressures as easing. RBI minutes from the emergency meeting in March show the bank is willing to use “any instrument – conventional and unconventional” to deal with the virus. All told, the RBI is likely to continue cutting rates after this last 75 bp move.

You Might Also Like

Dollar Firm as Europe Fails to Deliver

Dollar Firm as Europe Fails to Deliver

The dollar is stabilizing; reports suggest the White House is developing a plan to reopen the US economy sooner rather than later. Both Hong Kong and Singapore just tightened restrictions on gathering and movement. FOMC minutes for the March 15 decision will be released today.

Dollar Firm as Two-Day FOMC Meeting Begins

Dollar Firm as Two-Day FOMC Meeting Begins

The dollar continues to gain traction as the two-day FOMC begins; US political uncertainty has entered a new phase. Yesterday marked the third time that UK Prime Minister Johnson lost a vote for elections; he will try again today. Weak South Africa data support our call for imminent easing; the threat of sanctions against Turkey are back on the table.

Dollar Rally Stalls as Fresh Drivers Awaited

Dollar Rally Stalls as Fresh Drivers Awaited

US-China relations continue to improve with news of cooperation in a major fentanyl case. Eurozone final services and composite PMIs surprised on the upside; UK Parliament will be dissolved today. Poland is expected to keep rates steady at 1.5%; Russia October CPI is expected to rise 3.8% y/y. China sold €4 bn in its first euro-denominated bond since 2004; Thailand cut rates 25 bp to 1.25%, as expected.

Tentative Stabilization

Tentative Stabilization

Risk-off continues in Asia, but moves have been less dramatic. European market jittery but stable. Implied rates now pricing in a full Fed cut by September. The UK will announce its decision on Huawei’s access to the country’s 5G network.

Dollar Firm Ahead of US Jobs Report

Dollar Firm Ahead of US Jobs Report

The number of confirmed coronavirus cases and deaths continue to rise; the dollar continues to climb. The January jobs data is the highlight for the week; Canada also reports jobs data. The Fed submits its semiannual Monetary Policy Report to Congress today; Mexico and Brazil report January inflation data.

Virus Concerns Resurface

Virus Concerns Resurface

Markets are reacting badly to upward revisions to coronavirus cases in China. The euro fell to the weakest level since mid-2017 against the dollar. UK housing data adds to relatively upbeat figures since the December elections. Malaysia’s government is joining in the counter-cyclical fiscal effort.

Dollar Firms, Equities Sink Ahead of ECB Decision as US Fails to Deliver

Dollar Firms, Equities Sink Ahead of ECB Decision as US Fails to Deliver

President Trump spoke to the nation last night and did little to calm markets; reports suggest that the Democrats are working on a bill. Fed easing expectations are intensifying. The ECB decision will be out at 845 AM ET; over the past 17 ECB decision days, the euro has finished lower in 11 of them.

Dollar Mixed, Equities Higher as Virus News Stream Improves

Dollar Mixed, Equities Higher as Virus News Stream Improves

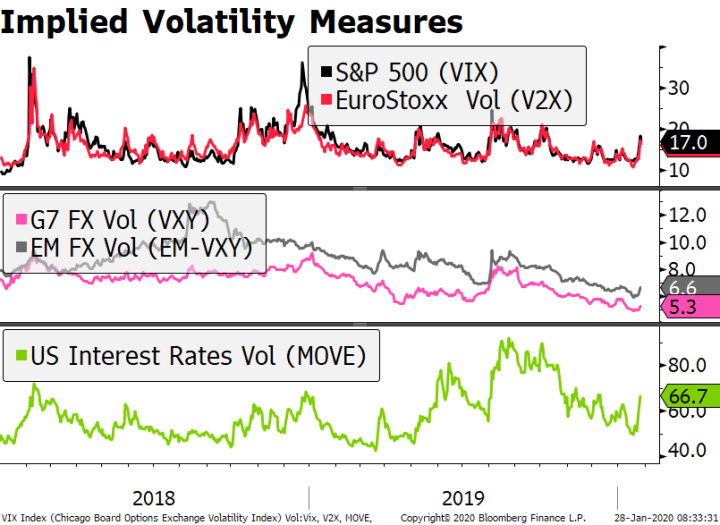

It was a relatively good weekend in virus-related news; measures of implied volatility continue to trend lower. The dollar is trying to build on its recent gains; investors continue to try and gauge just how bad the US economy will get hit. The outlook for oil prices remains highly uncertain and volatile.

Tags: Articles,Daily News,Featured,newsletter