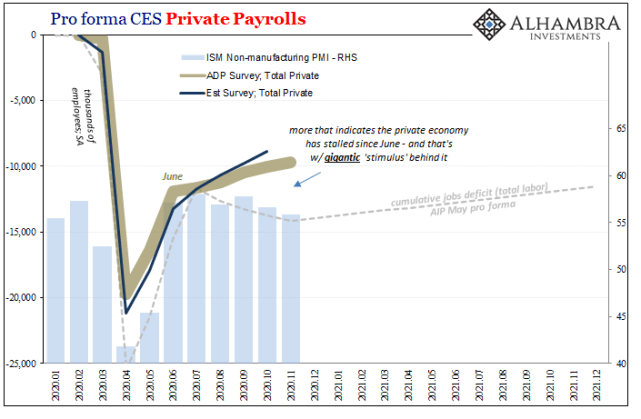

The ISM’s Non-manufacturing PMI continued to decelerate from its high registered all the way back in July 2020. In that month, the headline index reached 58.1, the best since early 2019, and for many signaling that everything was coming up “V.” Since, however, it’s been a slow downward trend that, when realizing early 2019 wasn’t exactly robust, only reconfigures the very nature of this rebound. When comparing comebacks from outsized economic contractions, the best level in 2020 was entirely too equal to the best from 2010-11 – which, as we unlike Economists know, didn’t equate to recovery then, either. Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge Sure, the economy is still moving positively but barely. Given now this summer slowdown has

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, currencies, economy, employment, Featured, Federal Reserve/Monetary Policy, Initial Jobless Claims, ism non manufacturing index, jobless claims, Labor market, Markets, newsletter, unemployment insurance

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The ISM’s Non-manufacturing PMI continued to decelerate from its high registered all the way back in July 2020. In that month, the headline index reached 58.1, the best since early 2019, and for many signaling that everything was coming up “V.” Since, however, it’s been a slow downward trend that, when realizing early 2019 wasn’t exactly robust, only reconfigures the very nature of this rebound.

When comparing comebacks from outsized economic contractions, the best level in 2020 was entirely too equal to the best from 2010-11 – which, as we unlike Economists know, didn’t equate to recovery then, either. |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

| Sure, the economy is still moving positively but barely. Given now this summer slowdown has extended into its fourth or fifth month (depending which data point), the “V” is surely dead. Add this ISM number on top of the multitude of others already nailed into its coffin.

Further, to reinforce the point that even the non-manufacturing 58.1 wasn’t indicative of recovery rather than rebound, the underlying employment index has remained stuck – at best – around neutral. There just was never enough momentum or even raw activity (or functional dollar liquidity) which would have persuaded businesses to robustly rehire let alone hire a lot more workers. |

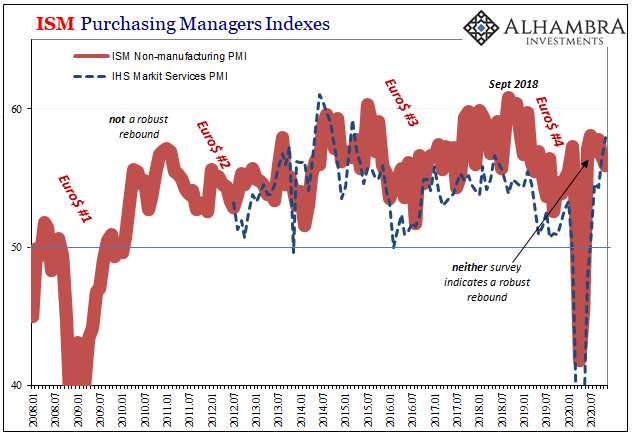

ISM Purchasing Managers Indexes, 2008-2020 - Click to enlarge |

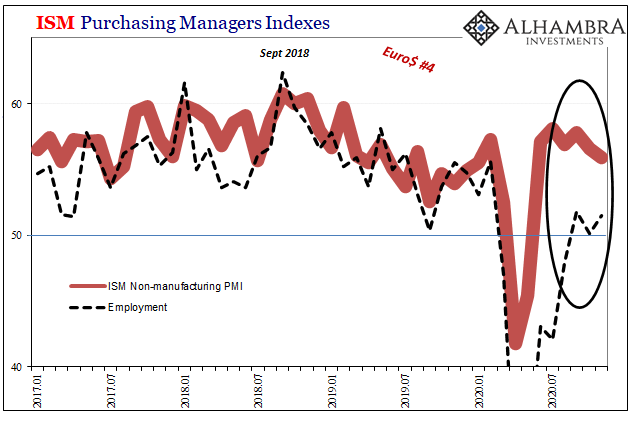

ISM Purchasing Managers Indexes, 2017-2020 - Click to enlarge |

|

| At least in the ISM’s employment components, both manufacturing and non-manufacturing, they quite easily fit with the troubling picture of a labor market likewise experiencing a summer slowdown way, way short of sufficient. Weakness is far more apparent in levels, too, not just these lacking rates.

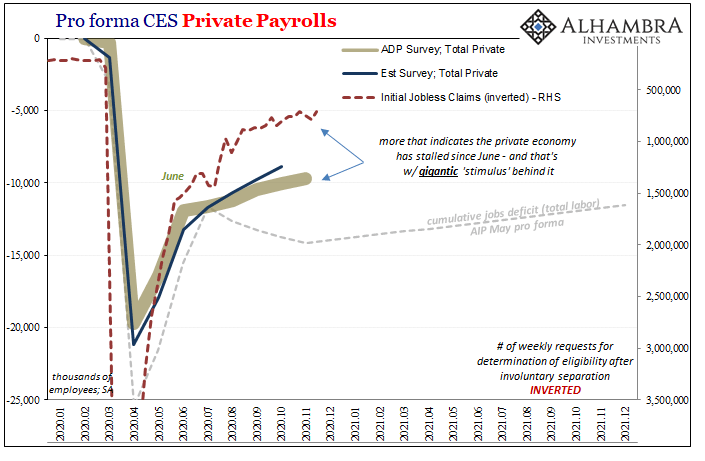

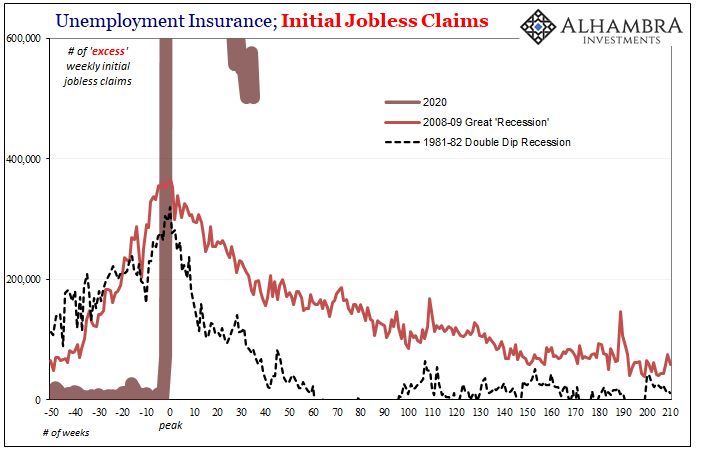

Initial jobless claims (Thursday ritual) dropped last week after two weeks having surged more than (revised) 10%. From 787,000 two weeks ago, the latest estimate (712k) indicates still more than 700,000 former American workers filing for insurance payment eligibility; another week which, before this year, would’ve been a record number. |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

| That’s all the way through November.

Like the ISM PMI, it appears the overall economic situation continues to improve in absolute terms. It is the trends, the dramatic and persisting slowing of the rate of improvement, which portend a boatload of future problems. |

Unemployment Insurance, Initial Jobless Claims, 1980-2020 - Click to enlarge |

| Somehow, incoming government subsidies (not “stimulus”) plus the suddenly uncertain rollout of COVID vaccines (google: Pfizer “supply chain” snags) are, in some commentary, enough to render this slowdown moot anyway.

Forget today’s struggles, tomorrow’s government cash payments and vaccinations are all that matter. Other than the US$’s exchange value with the euro, even stocks aren’t jumping fully onboard this interpretation. And, as noted yesterday, oil’s got OPEC and record domestic inventories (indicative of the same summer slowdown) to carry forward until those future developments hopefully pan out. |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

|

| They’re saying it’ll be easy to get the economy back up and running again once COVID is removed from the equation; which, you’ll recall, was exactly what was said when the reopening process began. Dead “V”, it wasn’t so easy after all so bring in the next set of dei ex machina.

Here we are six months later, COVID isn’t really as much of a problem but the economic factors holding back especially employment certainly are. Payroll numbers come tomorrow, and if they are anything like ADP’s initial estimates, we’ll be adding another nail to the “V’s” coffin which has already been hammered full of them. Thus, we’re left to wonder if the next “V”, which some claim is really a “K”, and that’s OK, isn’t that big of a difference. Shifting letters, moving the goalposts already, that, too, is very 2010-11 like. |

Friedman's Plucking Model of Trend-Cycle Analysis - Click to enlarge |

You Might Also Like

Reality Beckons: Even Bigger Payroll Gains, Much Less Fuss Over Them

Reality Beckons: Even Bigger Payroll Gains, Much Less Fuss Over Them

2020-07-05

What a difference a month makes. The euphoria clearly fading even as the positive numbers grow bigger still. The era of gigantic pluses is only reaching its prime, which might seem a touch pessimistic given the context. In terms of employment and the labor market, reaction to the Current Employment Situation (CES) report seems to indicate widespread recognition of this situation. And that means how there are actually two labor markets at the moment.

Purchasing Managers Indigestion

Purchasing Managers Indigestion

2020-08-06

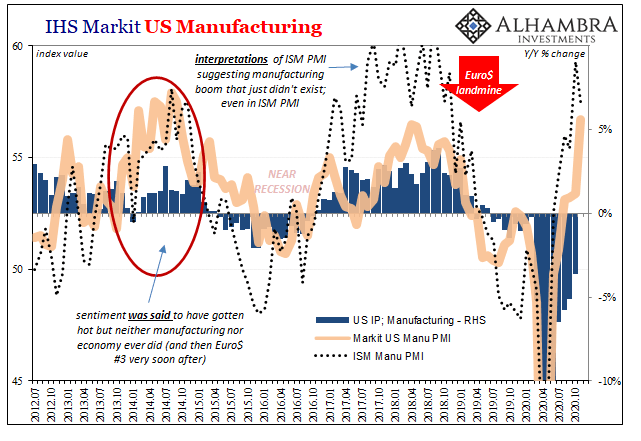

There’s already doubt given how the two major series supposedly measuring the same thing seemingly can’t agree. If the rebound was truly robust, it would show up unambiguously everywhere. But IHS Markit’s purchasing managers indices struggled to get back above 50 in July, barely getting there, suggesting the economy might be slowing or even stalling way too close to the bottom.

*These* Are The Real Huge Jobs Numbers, And They Will Make Your Blood Run Cold

*These* Are The Real Huge Jobs Numbers, And They Will Make Your Blood Run Cold

2020-08-24

There is simply no way to spin these figures as anything good. Not just the usual ones were talking about here, but more so some new data that you probably haven’t seen before. Beginning with the regular, it doesn’t matter that the level of initial jobless claims has declined substantially over the past few weeks

It Just Isn’t Enough

It Just Isn’t Enough

2020-10-10

The Department of Labor attached a technical note to its weekly report on unemployment claims. The state of California has announced that it is suspending the processing of initial claims filed by (former) workers in that state.

There Have Actually Been Some Jobs Saved, Only In Place of Recovery

There Have Actually Been Some Jobs Saved, Only In Place of Recovery

2020-12-04

The ISM reported a small decline in its manufacturing PMI today. The index had moved up to 59.3 for the month of October 2020 in what had been its highest since September 2018. For November, the setback was nearly two points, bringing the headline down to an estimate of 57.5.

Wait A Minute, What’s This Inversion?

Wait A Minute, What’s This Inversion?

2020-06-28

Back in the middle of 2018, this kind of thing was at least straight forward and intuitive. If there was any confusion, it wasn’t related to the mechanics, rather most people just couldn’t handle the possibility this was real. Jay Powell said inflation, rate hikes, and accelerating growth. Absolutely hawkish across-the-board.And yet, all the way back in the middle of June 2018 the eurodollar curve started to say, hold on a minute.

The (Other) Shoe Of Unemployment

The (Other) Shoe Of Unemployment

2020-07-25

After raising the specter of a rebound stall, the idea before limited to Japan and Germany was abruptly given further weight today by US jobless claims numbers. For the first time since the peak at the end of March, the weekly tally of initial filings increased from the prior week.

Good Payrolls Still Say Slowdown

Good Payrolls Still Say Slowdown

2020-11-09

The payroll report for the month of October 2020 was a very good one. This shouldn’t be surprising, perfect BLS publications appear with regularity even during the most challenging of circumstances. Headlines and underneath, everything looked fine last month.

Tags: currencies,economy,employment,Featured,Federal Reserve/Monetary Policy,Initial Jobless Claims,ism non manufacturing index,jobless claims,Labor Market,Markets,newsletter,unemployment insurance