There is a lot of evidence which shows some basis for expectations-based monetary policy. Much of what becomes a recession or worse is due to the psychological impacts upon businesses (who invest and hire) as well as workers being consumers (who earn and then spend). Once the snowball of macro contraction begins rolling downhill, rational prudence dictates some degree of caution on all parts (pro-cyclicality). Bathed in the unearned glow of the Great “Moderation”, central banking’s greatest thinkers untroubled by no longer thinking about finance or money began to presume they had figured out a way to manipulate “confidence” to such a degree that it would allow them some substantial degree of control over the entire business cycle. Down as well as up. Ben

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, Alan Greenspan, Business cycle, consumer spending, currencies, economy, EuroDollar, eurodollar system, expectations policy, Featured, Federal Reserve, Federal Reserve/Monetary Policy, jay powell, Markets, newsletter, QE, Recession, recovery, Retail sales

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| There is a lot of evidence which shows some basis for expectations-based monetary policy. Much of what becomes a recession or worse is due to the psychological impacts upon businesses (who invest and hire) as well as workers being consumers (who earn and then spend). Once the snowball of macro contraction begins rolling downhill, rational prudence dictates some degree of caution on all parts (pro-cyclicality).

Bathed in the unearned glow of the Great “Moderation”, central banking’s greatest thinkers untroubled by no longer thinking about finance or money began to presume they had figured out a way to manipulate “confidence” to such a degree that it would allow them some substantial degree of control over the entire business cycle. Down as well as up. Ben Bernanke, among others, swallowed this view hook, line, and sinker (along with the adoration and attention it necessarily brought them). After all, he said, look at the nineties and 2000’s (before August 2007, obviously). With the tiny dot-com recession (why don’t stock crashes by themselves create depressions anymore?) the lone economic blemish in that 16-year span between 1991 and 2007, policymakers were riding high as to their emotional exploitation scheme. |

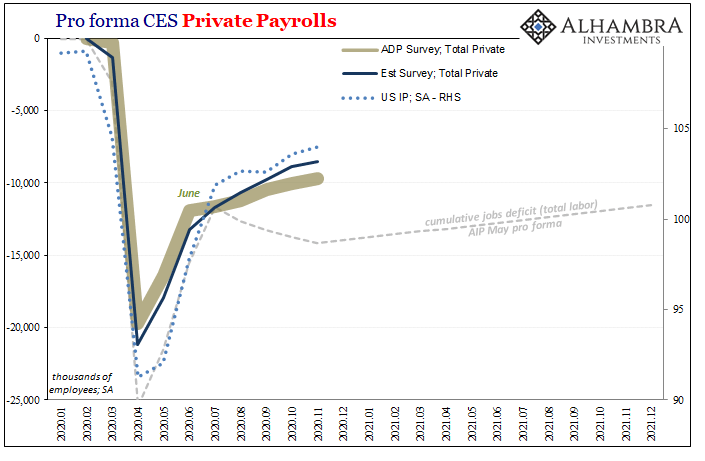

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

August 2007, however, should have awoken deep skepticism; maybe it hadn’t been pop psychology which had produced the near-unbroken “moderation” of the long prior span. Perhaps Federal Reserve officials, in particular, should have paid much closer attention to not just what Salomon Brothers had been up to at the start of it, more importantly why these “brothers” were doing these things and the potentially grave implications of everyone else in the money dealer family doing much the same.

In other words, what if the monetary system had drastically changed (which Greenspan’s crew knew) and its unappreciated, decidedly immoderate ascent had been responsible for those particular 16 years? What good might monetary policy be with no money to offer attempting instead to manipulate happy thoughts throughout an economy recoiling in the wake of widespread, obvious (to any honest person operating outside the close central bank orbit) money shortages? Subprime mortgages nothing, this pretty much sums up the Great “Recession” as well as what didn’t follow it. Now 2020. The year of COVID, no doubt, but no less monetarily dry. Officials are thumping their chests about how well they must’ve performed given the lack of another Lehman, but like the original Lehman (which I still have more to say here) they’ve got it all wrong. But this part Federal Reserve Chairman Powell has right, warning Congress at the end of last month:

Again, the brief sparkle of truth underlying the expectations nonsense. This year, Powell’s Fed has tried Japan-style QE, Japan-style inflation targeting, and even Japan-surpassing lies about “digital money printing.” All of it with the same Japan-like goal in mind: making people “confident that it is safe to re-engage in a broad range of activities.” Uh oh. |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

|

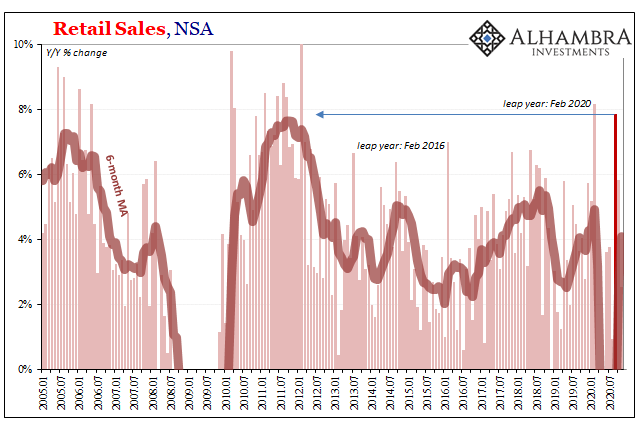

As we’ve catalogued for months now, the re-engaging part never even got halfway and now the rebound’s down to not yet nil but closing in again on nil. The labor market, most importantly, most of all.One of the very few indications otherwise had been US Retail Sales – and only for a brief time. In September, Americans apparently splurged and did so in a way that was, for once, at least plausibly consistent with the level of activity a “V”-shaped trajectory would feature. Overall sales growth had risen by the most in unadjusted terms (outside of leap year Februarys with their 29th day advantages) since before the 2012 (Euro$ #2) slowdown (the end of all recovery hopes). |

Retail Sales, NSA 2005-2020 - Click to enlarge |

| Was that a sign of things to come, an actual acceleration as consumers looked upon a resurgent labor market and, as Powell said, re-engaged in immoderate spending? Or, had it been merely the same outlier jump brought about artificially by some large government handouts and subsidizing stipends?As noted yesterday, the production side of the economy (which includes a healthy proportion of the unhealthy services side) has been unequivocal on which one; producers haven’t just been betting on the latter, they are actively suppressing their own activities having already been convinced of it. |

US Retail Sales, 2016-2020 - Click to enlarge |

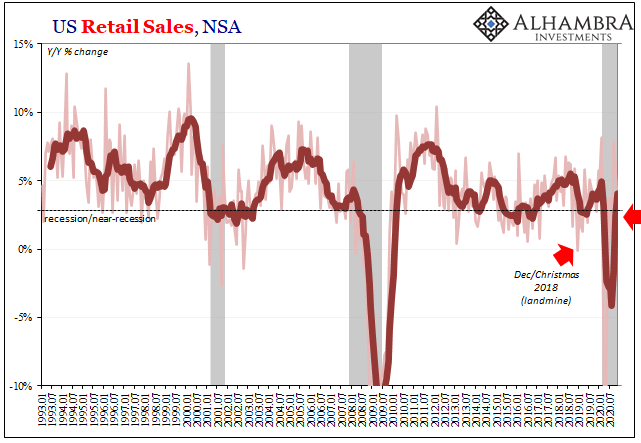

| Now the updated spending figures for October and thus November (released today). Retail sales have declined, seasonally-adjusted, in both (October’s estimate was revised downward), with November’s, a key month for the all-important Christmas period circled on every single retailer’s calendar, coming in with a significant monthly negative at the worst time. |

US Retail Sales, NSA 1993-2020 - Click to enlarge |

|

In the unadjusted series, year-over-year total retail sales were up just 2.52%! That’s right back down into recession territory after having been in somewhat “V” shape for only the one month. Following a huge contraction earlier this year after which symmetry already proposes an equally huge rebound, massive stipends abound, QE all over the place, and yet there remains serious reluctance “to re-engage in a broad range of activities.”Powell, like most, will point to COVID and a second wave of non-economic factors beginning with unnecessary interruptions to the economy. Of course he will; he already has. Workers always suffer the most under the deflationary strain central banks never time; Keynes was exactly right about this, and the Federal Reserve’s entire history – including how wrong it was about the Great “Moderation” – a litany of tragic errors more than establishing what used to be common knowledge. |

US Retail Sales, 1992-2020 - Click to enlarge |

| The Great Inflation, like the Great Depression, only its most glaring.

The Great “Recession” and its aftermath, what my co-host Emil Kalinowski wisely calls this Silent Depression, still ongoing, would be right at the top of this list if it hadn’t been for all that manipulation and squandered good faith wasted by the Greenspan “put” which doesn’t in reality exist. “To re-engage in a broad range of activities” will need more than vaccines and additional stipends, however enormous-sounding; it sure requires something other than QE. |

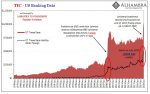

US TIC, 1996-2020 - Click to enlarge |

Friedman's Plucking Model of Trend-Cycle Analysis - Click to enlarge |

You Might Also Like

This Has To Be A Joke, Because If It’s Not…

This Has To Be A Joke, Because If It’s Not…

2020-08-28

After thinking about it all day, I’m still not quite sure this isn’t a joke; a high-brow commitment of utterly brilliant performance art, the kind of Four-D masterpiece of hilarious deception that Andy Kaufman would’ve gone nuts over. I mean, it has to be, right?I’m talking, of course, about Jackson Hole and Jay Powell’s reportedly genius masterstroke.

Fama 2: No Inflation For Old Central Banks

Fama 2: No Inflation For Old Central Banks

2020-08-14

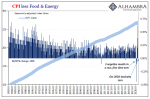

The Bureau of Labor Statistics reported that the core CPI in July 2020 jumped by the most (+0.62%) in almost thirty years. After having dropped month-over-month for three months in a row for the first time in its history, it has posted back to back gains the latest of which pushing the index back above its February level.

Part 2 of June TIC: The Dollar Why

Part 2 of June TIC: The Dollar Why

2020-08-21

Before getting into the why of the dollar’s stubbornly high exchange value in the face of so much “money printing”, we need to first go back and undertake a decent enough review of the guts maybe even the central focus of the global (euro)dollar system.

Not This Again: Too Many Treasuries?

Not This Again: Too Many Treasuries?

2020-08-27

Tomorrow, the Treasury Department is going to announce the results of its latest bond auction. A truly massive one, $47 billion are being offered of CAH4’s notes dated August 31, 2020, maturing out in August 31, 2027. In other words, the belly of the belly, the 7s.We’ve already seen them drop for two note auctions this week, both equally sizable.

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

2020-10-02

It’s always something. There’s forever some mystery factor standing in the way. On the topic of inflation, for years it was one “transitory” issue after another. The media, on behalf of the central bankers it holds up as a technocratic ideal, would report these at face value. The more obvious explanation, the argument with all the evidence, just couldn’t be true otherwise it’d collapse the technocracy right down to the ground.And so it was also in the bond market. Inflation and their yields very much related, the lack of the former wasn’t ever used to explain the curious absence of the BOND ROUT!!! No, the US Treasury market has been beset by its own set of “transitory” factors, too. As ridiculous as some of the inflation excuses had been, Verizon’s unlimited wireless data plans the

Where Is It, Chairman Powell?

Where Is It, Chairman Powell?

2020-11-15

Where is it, Chairman Powell? After spending months deliberately hyping a “flood” of digital money printing, and then unleashing average inflation targeting making Americans believe the central bank will be wickedly irresponsible when it comes to consumer prices, the evidence portrays a very different set of circumstance.

Six Point Nine Times Two Equals What It Had In Twenty Fourteen

Six Point Nine Times Two Equals What It Had In Twenty Fourteen

2020-11-17

It was a shock, total disbelief given how everyone, and I mean everyone, had penciled China in as the world’s go-to growth engine. If the global economy was ever going to get off the ground again following GFC1 more than a half a decade before, the Chinese had to get back to their precrisis “normal.”

Eugene Fama’s Efficient View of Stimulus Porn

Eugene Fama’s Efficient View of Stimulus Porn

2020-08-13

The key word in the whole thing is “bias.” For a very long time, people working in and around the finance industry have sought to gain tremendous advantages. No explanation for the motive is required. Charts, waves, technical (sounding) analysis and so on.

Tags: Alan Greenspan,Business Cycle,consumer spending,currencies,economy,EuroDollar,eurodollar system,expectations policy,Featured,Federal Reserve/Monetary Policy,federal-reserve,jay powell,Markets,newsletter,QE,recession,recovery,Retail sales