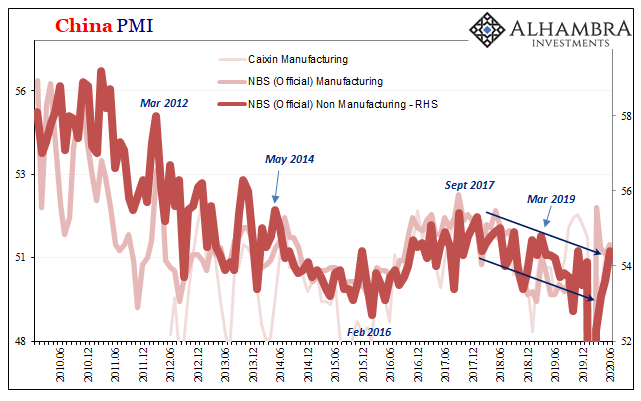

China’s PMI’s continue to impress despite the fact they continue to be wholly unimpressive. As with most economic numbers in today’s stock-focused obsessiveness, everything is judged solely by how much it “surprises.” Surprises who? Doesn’t matter; some faceless group of analysts and Economists whose short-term modeling has somehow become the very standard of performance. According to one such group, China’s official manufacturing index, the one calculated and maintained by the government (via its National Bureau of Statistics), solidly “beat” expectations. The headline was thought to have declined from May’s 50.6 to somewhere around 50.2. Instead, the NBS reports it accelerated during June 2020 to 50.9 for a big upside surprise. While the manufacturing PMI was

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, China, china nbs manufacturing pmi, china nbs non-manufacturing pmi, currencies, economy, Featured, Federal Reserve/Monetary Policy, global recovery, manufacturing, Markets, newsletter, non-manufacturing, PMI

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

China’s PMI’s continue to impress despite the fact they continue to be wholly unimpressive. As with most economic numbers in today’s stock-focused obsessiveness, everything is judged solely by how much it “surprises.” Surprises who? Doesn’t matter; some faceless group of analysts and Economists whose short-term modeling has somehow become the very standard of performance. According to one such group, China’s official manufacturing index, the one calculated and maintained by the government (via its National Bureau of Statistics), solidly “beat” expectations. The headline was thought to have declined from May’s 50.6 to somewhere around 50.2. Instead, the NBS reports it accelerated during June 2020 to 50.9 for a big upside surprise. While the manufacturing PMI was that to the easily impressed (and surprised), the non-manufacturing PMI was a resounding joy. At 53.6 in the prior month, the bar was set down at 52.1 (or thereabouts depending upon which “consensus” the consensus gives consent). Beating the forecast by more than two and a quarter points, the official version for June is 54.4. |

China PMI, 2010-2020(see more posts on China PMI, ) - Click to enlarge |

| Given the situation in which the Chinese economy finds itself, no different from that of the rest of the world, there isn’t any meaningful difference between 52.1 and 54.4. Neither of those actually indicate what everyone wants to see right now.

Acceleration. Meaningful acceleration. Instead, these lower levels even though still above 50 indicate at best the economy bottoming out. Not acceleration. And that’s actually bigger trouble than it sounds since, going by the PMI’s as well as China’s official story, the non-economic shutdown ended months ago. In terms of both China’s PMI’s, there was just the one month of the historic drop off (February) and then everything is supposedly moved back near normal. |

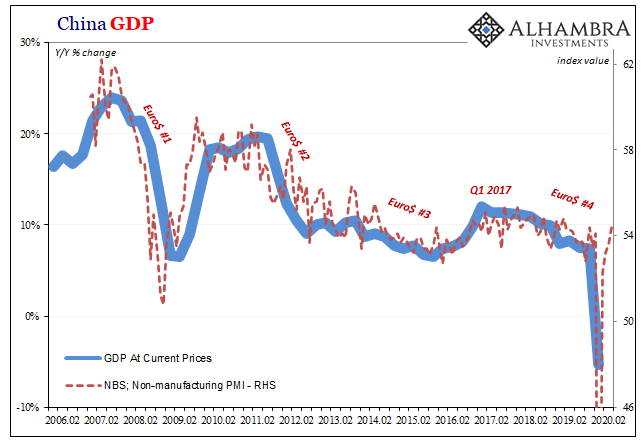

China GDP, 2006-2020 - Click to enlarge |

| To show you what I mean when I claim that’s not what these PMI’s (nor anything else) are suggesting, we have to go beyond rates never forgetting that levels matter, too. In cases where there are sizable contractions, the starting levels matter even more.

All PMI’s tell us is whether there are more (>50), less (<50), or the same number (50) of respondents reporting growth. That’s it. So, if very few purchasing managers are telling the government they are seeing growth, then that’s consistent with a sizable economic decline. Once that decline has finished, for whatever reasons, we should expect meaningful acceleration – what we (used to) call recovery. First, though, the economy has to bottom out, which in the PMI’s means a transition from sub-50 to more than 50. That by itself, however, does not mean anything more. What needs to follow is that acceleration; if bottoming out is, after widespread contraction, the slight majority of respondents reporting growth then acceleration would be indicated when that small majority becomes an overwhelming one. Nearer everyone gets in on the upside. In PMI’s, that means slightly above 50 isn’t nearly enough. |

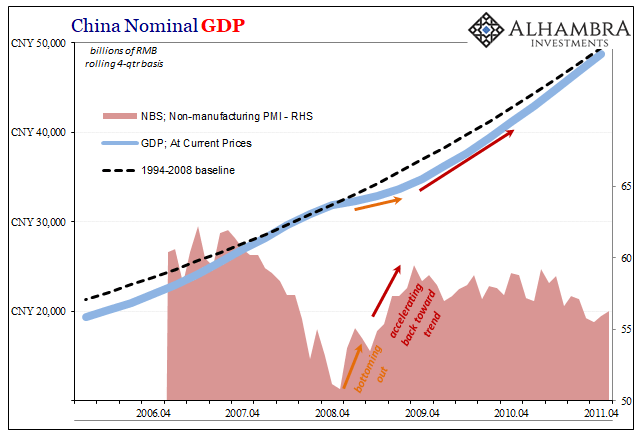

China Nominal GDP, 2006-2011 - Click to enlarge |

| If we go back and review China’s experience during the Great “Recession” and immediately after, that’s just what we find. Using the NBS Non-Manufacturing index as our sentiment proxy, it had indicated a bottoming out in the first few months of 2009 as the trough hit worldwide.

That wasn’t the end, however, as in the last half of 2009 the PMI leapt toward 60 consistent with the kind of acceleration (a significant enough majority reporting growth) that in this instance had pushed nominal Chinese GDP back up toward its prior trend. Recovery, for short. An actual “V” as opposed to those missing at the same time throughout the developed world; the key difference between mere positive numbers and real growth. |

China Nominal GDP, 2006-2011 - Click to enlarge |

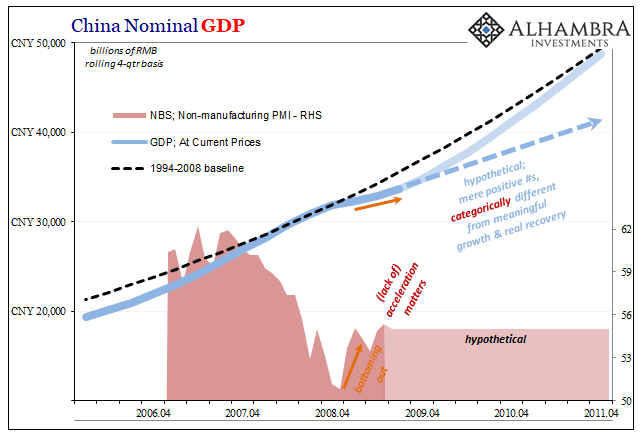

| If that PMI hadn’t gone any further, still only a small majority of respondents reporting growth, that would’ve instead suggested a very different outcome in GDP like the real economy. No more contraction, sure, but falling short of acceleration and therefore recovery.

“L”, in other words. The recession ended, but the pain only beginning (which we know all-too-well). In fact, that’s just we see in both rates as well as levels in China’s post-2011 experience. Following Euro$ #2 (despite the “flood” of liquidity which every media outlet excitedly reported), PMI’s fell back to where the number of survey reports indicating growth was only slightly more than those not indicating it; growth, but not really as it didn’t appear to be spread near wide enough. Thus, mere positive numbers. Once that happened, in the lower 50’s for these PMI’s, the Chinese economy caught up to the rest of the world’s ongoing, QE-immune malaise. |

China Nominal GDP, 2006-2020 - Click to enlarge |

There just isn’t near enough growth indicated by anything less than 56 and probably 58 and 59 at this point in 2020. The level matters as much as the rate! You can’t just ignore the size and scale of the decline, and therefore how much we depend upon meaningful, widespread acceleration just to be able to pull back out of it.

And in this case, the fact that the economic dislocation was (allegedly) short and non-economic in nature only adds to the disappointment and intrigue. A true “V” in PMI numbers following that particular set of circumstances would’ve been up near 60 if not higher by April, May at the latest.

Instead, what China’s PMI’s (both sets) are indicating is nothing more than what the last US payroll report had showed – the global economy has bottomed out, and that’s it.

Vastly more important, we shouldn’t be left scratching our heads wondering where’s the acceleration. The fact that it remains missing is more “L-ish” than people are thinking, and are being led to believe particularly when, in mainstream convention, analysis consists solely of whether or not whichever number beat its consensus. Upside surprise and all that.

The only surprise here, to many if not most, is the decided lack of upside in these numbers.

You Might Also Like

China’s Back!

China’s Back!

The Washington Post began this week by noting how the US economy seems to have lost its purported zip just when it needed that vitality the most. Never missing a chance to take a partisan swipe, of course, still there’s quite a lot of truth behind the charge. An actual economic boom produces cushion, enough of one that President Trump and his administration may have been counting on it when opting for full-blown shutdown.

Not COVID-19, Watch For The Second Wave of GFC2

Not COVID-19, Watch For The Second Wave of GFC2

I guess in some ways it’s a race against the clock. What the optimists are really saying is the equivalent of the old eighties neo-Keynesian notion of filling in the troughs. That’s what government spending and monetary “stimulus” intend to accomplish, to limit the downside in a bid to buy time. Time for what? The economy to heal on its own.

Manufacturing Clears Up Bond Yields

Manufacturing Clears Up Bond Yields

Yesterday, IHS Markit reported that the manufacturing turnaround its data has been suggesting stalled. After its flash manufacturing PMI had fallen below 50 several times during last summer (only to be revised to slightly above 50 every time the complete survey results were tabulated), beginning in September 2019 the index staged a rebound jumping first to 51.1 in that month.

More Trends That Ended 2019 The Wrong Way

More Trends That Ended 2019 The Wrong Way

Auto sales in 2019 ended on a skid. Still, the year as a whole wasn’t nearly as bad as many had feared. Last year got off on the wrong foot in the aftermath of 2018’s landmine, with auto sales like consumer spending down pretty sharply to begin it. Spending did rebound in mid-year if only somewhat, enough, though, to add a little more to the worst-is-behind-us narrative which finished off 2019.

Not Abating, Not By A Longshot

Not Abating, Not By A Longshot

Since I advertised the release last week, here’s Mexico’s update to Industrial Production in November 2019. The level of production was estimated to have fallen by 1.8% from November 2018. It was up marginally on a seasonally-adjusted basis from its low in October.

China Enters 2020 Still (Intent On) Managing Its Decline

China Enters 2020 Still (Intent On) Managing Its Decline

Chinese Industrial Production accelerated further in December 2019, rising 6.9% year-over-year according to today’s estimates from China’s National Bureau of Statistics (NBS). That was a full percentage point above consensus. IP had bottomed out right in August at a record low 4.4%, and then, just as this wave of renewed optimism swept the world, it has rebounded alongside it.

Time Again For Triple Digit Dollar

Time Again For Triple Digit Dollar

Being a member of the institutional “elite” means never having to say you’re sorry; or even admit that you have no idea what you are doing. For Christine Lagarde, Mario Draghi’s retirement from the European Central Bank could not have come at a more opportune moment. Fresh off the Argentina debacle, she failed herself upward to an even better gig.

An International Puppet Show

An International Puppet Show

It’s actually pretty easy to see why the IMF is in a hurry to secure more resources. I’m not talking about potential bailout candidates banging down the doors; that’s already happened. The fund itself is doing two contradictory things simultaneously: telling the world, repeatedly, that it has a highly encouraging $1 trillion in bailout capacity at the same time it goes begging to vastly increase that amount.

Tags: China,china nbs manufacturing pmi,china nbs non-manufacturing pmi,currencies,economy,Featured,Federal Reserve/Monetary Policy,global recovery,manufacturing,Markets,newsletter,non-manufacturing,PMI