Jeffrey P. Snider

July 1, 2020

SNB & CHF

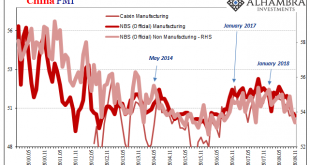

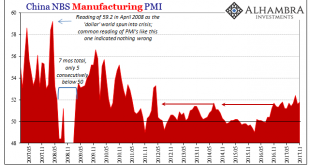

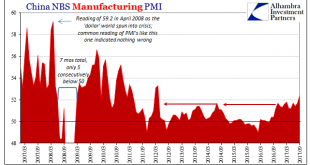

China’s PMI’s continue to impress despite the fact they continue to be wholly unimpressive. As with most economic numbers in today’s stock-focused obsessiveness, everything is judged solely by how much it “surprises.” Surprises who? Doesn’t matter; some faceless group of analysts and Economists whose short-term modeling has somehow become the very standard of performance.

According to one such group, China’s official manufacturing index, the one calculated and...

Read More »

Jeffrey P. Snider

September 4, 2019

SNB & CHF

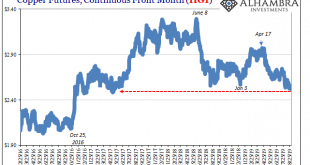

Copper prices behave more deliberately than perhaps prices in other commodity markets. Like gold, it is still set by a mix of economic (meaning physical) and financial (meaning collateral and financing). Unlike gold, there doesn’t seem to be any rush to get to wherever the commodity market is going. Over the last several years, it has been more long periods of sideways.

That’s what makes any potential breakout noteworthy. Dr. Copper’s place in the hierarchy is...

Read More »

Jeffrey P. Snider

December 4, 2018

SNB & CHF

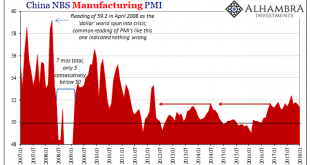

By the time things got really bad, China’s economy had already been slowing for a long time. The currency spun out of control in August 2015, and then by November the Chinese central bank was in desperation mode. The PBOC had begun to peg SHIBOR because despite so much monetary “stimulus” in rate cuts and a lower RRR banks were hoarding RMB liquidity.

Late 2015 was not a fun time in China. The idea of economic...

Read More »

Jeffrey P. Snider

February 4, 2018

SNB & CHF

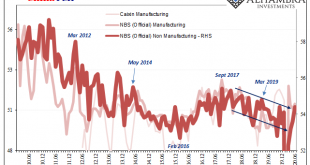

According to China’s official PMI’s, those looking for a boom to begin worldwide in 2018 after it failed to materialize in 2017 are still to be disappointed. If there is going to be globally synchronized growth, it will have to happen without China’s participation in it. Of course, things could change next month or the month after, but this idea has been around for a year and a half already.

Without China, growth won’t...

Read More »

Jeffrey P. Snider

December 13, 2017

SNB & CHF

China’s National Bureau of Statistics reported last week that the official manufacturing PMI for that country rose from 51.6 in October to 51.8 in November. Since “analysts” were expecting 51.4 (Reuters poll of Economists) it was taken as a positive sign. The same was largely true for the official non-manufacturing PMI, rising like its counterpart here from 54.3 the month prior to 54.8 last month.

China Manufacturing...

Read More »

Jeffrey P. Snider

November 4, 2017

SNB & CHF

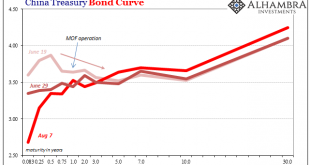

Back in June, China’s federal bond yield curve inverted. Ahead of mid-year bank checks, short-term govvies sold off as longer bonds continued to be bought. It was for some a rotation, for others a reflection of money rates threatening to spiral out of control. On June 19, for example, the 6-month federal security yielded 3.87% compared to a yield of 3.525% for the 10-year.

China Treasury Bonds(see more posts on china...

Read More »

Jeffrey P. Snider

October 14, 2017

SNB & CHF

In the US our economic data for a few months at least will be on shaky ground due to the lingering economic impacts of severe hurricanes. In China, the potential for irregularity is perhaps as great, though it has nothing to do with the weather. In a little over a week, Communist Party officials will gather for their 19th Party Congress.

The temptation may exist to deliver a somewhat better economic picture than has...

Read More »

Jeffrey P. Snider

June 9, 2017

SNB & CHF

Both US manufacturing PMI’s underwhelmed just as those from China did. The IHS Markit Index was lower than the flash reading and the lowest level since last September. For May 2017, it registered 52.7, down from 52.8 in April and a high of 55.0 in January. Just by description alone you can appreciate exactly what pattern that fits.

The ISM Manufacturing PMI was slightly higher in May than April, 54.9 versus 54.8, but...

Read More »

Jeffrey P. Snider

June 8, 2017

SNB & CHF

China’s PMI’s were uniformly disappointing with respect to what Moody’s was on about last week. Chinese authorities expended great effort and resources to get the economy moving forward again after several years of “dollar”-driven deceleration. There was a massive “stimulus” spending program where State-owned FAI expenditures of about 2% of GDP were elicited to make up for Private FAI that at one point last year was...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org