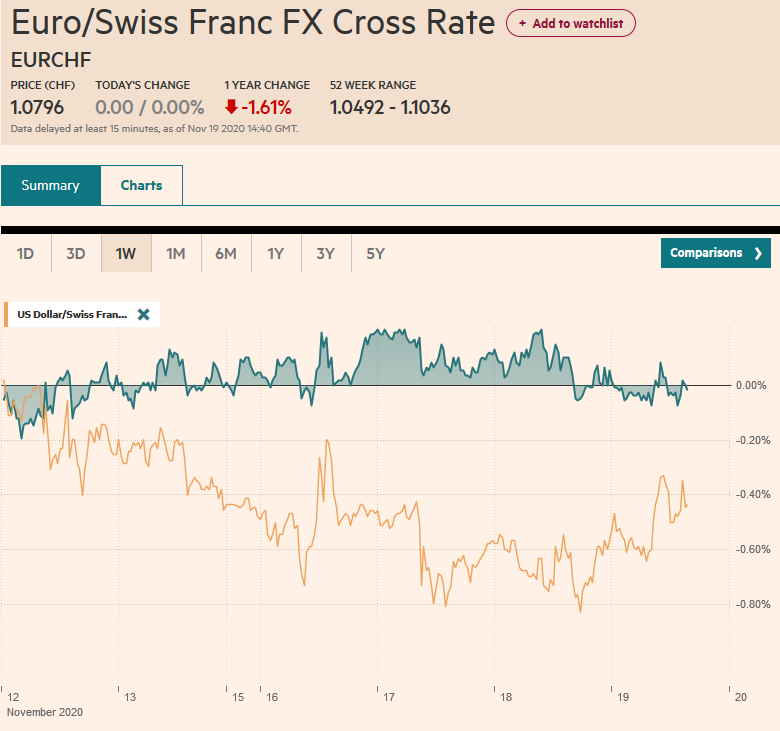

Swiss Franc The Euro is stable by 0.00% to 1.0796 EUR/CHF and USD/CHF, November 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: News that the New York City was closing the schools to contain the virus sent stocks reeling in late North American dealings yesterday and spurred some profit-taking in the Asia Pacific and Europe. Equities in the Asia Pacific region were mostly lower, though China, South Korea, and Australia’s advanced and Tokyo markets were mixed. The Dow Jones Stoxx 600 is off by almost 1%, which would be the month’s biggest loss. The European benchmark rose by about 12% over the past two weeks. Follow-through selling is weighing on US shares, and the NASDAQ is lower for the third consecutive

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, China, commodities, Currency Movement, EU, Featured, newsletter, Turkey, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro is stable by 0.00% to 1.0796 |

EUR/CHF and USD/CHF, November 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: News that the New York City was closing the schools to contain the virus sent stocks reeling in late North American dealings yesterday and spurred some profit-taking in the Asia Pacific and Europe. Equities in the Asia Pacific region were mostly lower, though China, South Korea, and Australia’s advanced and Tokyo markets were mixed. The Dow Jones Stoxx 600 is off by almost 1%, which would be the month’s biggest loss. The European benchmark rose by about 12% over the past two weeks. Follow-through selling is weighing on US shares, and the NASDAQ is lower for the third consecutive session. The US 10-year yield is hovering around 0.85%, while core European benchmark yields are a little softer, but the peripheral yields are lagging. The dollar is having one of its best days in recent weeks, rising against nearly all the currencies in the world. Among the majors, the Scandis, Antipodeans, and sterling are leading the downside with 0.4%-0.6% losses. The euro, yen, and Swiss franc are 0.15%-0.25% lower. Emerging market currencies are heavy, and the JP Morgan Emerging Market Currency Index is snapping a four-day rally. Gold is trading like a risk asset and is down for the fourth consecutive session and has approached last week’s low near $1850. The September low was just below there (~$1848), and a break could signal a return to $1800. December WTI has pushed above $42 a barrel several times in recent days but has failed to settle above it. It found a bid in the European morning near $41.20. |

FX Performance, November 19 - Click to enlarge |

Asia Pacific

Australia provided a pleasant surprise today in a day in which the surging virus has otherwise dealt a blow to sentiment. The lifting of the lockdown in Victoria saw a surge in employment. The nearly 179k increase blew away forecasts, where the median projection in the Bloomberg survey was for a loss of 27.5k jobs. The downward revision in September to show a loss of 42.5k positions (-29.5k initially) made the recovery all the more impressive. Full-time positions account for a little half (97k) of the employment gains. The fact that the participation rate jump to 65.8% from a revised 64.9% prevented the unemployment rate from improving (7.0% vs. 6.9%). The unexpected jump in employment was insufficient to prevent the Australian dollar from slipping lower in the risk-averse mood.

A combination of strong demand from China and concerns that poor weather will make for a light crop has driven up soy prices to a six-year high. Prices are up 8% this month and almost 24% since the end of August. Wheat prices are up 10% over the same period. US soy stocks are low, and China has promised to step up its purchases of US agriculture. Chinese demand is also thought to be driving the price of iron ore to new highs for the year. The front-month futures contract is up for the fourth consecutive session and nine of the past ten for around an 11% surge. Copper prices are consolidating since making a two-year high to start the week. Oil prices are at the upper end of where they traded over the past two months.

The dollar is pushing back above JPY104 in the European morning after holding above yesterday’s low (~JPY103.65) in local markets. There are options for around $950 mln struck between JPY104.25-JPY104.35 that expire today. This area may be sufficient to check stronger dollar gains today, but if not, another set of expiring options in the JPY104.50-JPY105.60 area for $1.6 bln should. The Australian dollar was unable to surpass last week’s high ($0.7340) despite trying in the past two sessions, leaving it vulnerable to today’s setback. Initial support now is seen near $0.7250. Recall that it settled last week near $0.7270. The greenback is rising against the Chinese yuan for the second consecutive session, for the first time this month. Its nearly 0.5% gain is the most for nearly a month. Since dropping the “counter-cyclical” factor, the PBOC’s reference rate for the dollar has become more transparent. Today’s fix was at CNY6.5488, which was largely anticipated. The CNY6.60 and then CNY6.63 may cap corrective upticks in the US dollar.

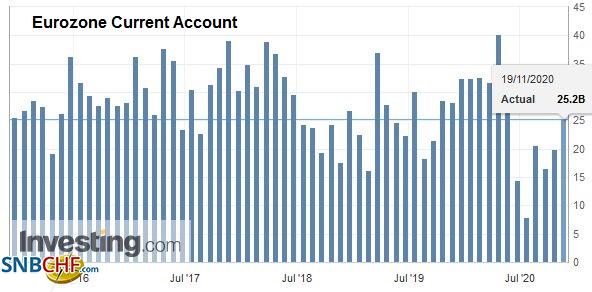

EuropeThe EU is fighting a two-front battle. On one side are the trade talks with the UK. Several deadlines have already been missed, and sometime early next week is the next one. Even though the standstill agreement does not end until December 31, the agreement has to be ratified by all the members to take effect. Some UK reports played up the likelihood of a last-minute agreement, but EU officials still report little progress. That said, many in the market suspect that sterling could move around 5% in either direction, depending on the results. The EU is under pressure to publish its plans if there is not an agreement to help businesses prepare. |

Eurozone Current Account, September 2020(see more posts on Eurozone Current Account, ) Source: investing.com - Click to enlarge |

| On the other side is the EU’s seven-year budget. It requires unanimity to be approved. Yet strings were attached to it regarding the rule of law that targets Poland and Hungary. They have rejected it. While many are sympathetic with the goal and the importance of the rule of law, the budget is arguably the wrong instrument to use precisely because of the consensus needed. There are other points of leverage, and the EU has both countries under formal investigation for not respecting the rule of law (independent judiciary and free press). A compromise has to be forged, and excluding Poland and Hungary is not really an option. |

Eurozone Current Account n.s.a., September 2020(see more posts on Eurozone Current Account, ) Source: investing.com - Click to enlarge |

As widely anticipated, Turkey’s new central banker hiked the one-week repo rate to 15.00% from 10.25%. This is partly a catch-up move, given that effective funding costs were already above 14%. However, the move signals a return toward a more orthodox policy, and that means that the one-week repo rate has been reactivated rather than other secondary rates used over the last few months. The lira initially rallied but has seen the gains halved. The dollar fell from about TRY7.70 to TRY7.5150 before bouncing back above TRY7.62.

Like the $0.7340 area in the Australian dollar, which proved a cap, the euro approached but was unable to move above $1.19 in the last couple of sessions. As the momentum stalled, the euro was vulnerable to the pullback. The week’s low was set Monday near $1.1815. A break of $1.1800 could signal a deeper correction toward $1.1750. The $1.1840-$1.1850 area may cap the upside. Sterling was unable to push above last week’s high (~$1.3315) yesterday and has been sold to $1.3200 today. Initial support is seen near $1.3185 and then around $1.3155. Resistance is now seen around $1.3240-$1.3250. The euro has edged higher against sterling. It had approached GBP0.8915 yesterday, and nearly 1.4 bln euros of options will expire today struck between GBP0.8900 and GBP0.8925. The euro is traded firmer in Asia but met new sellers in Europe near GBP0.8960. The cross settled last week near GBP0.8975 and has not traded above GBP0.9000 this week.

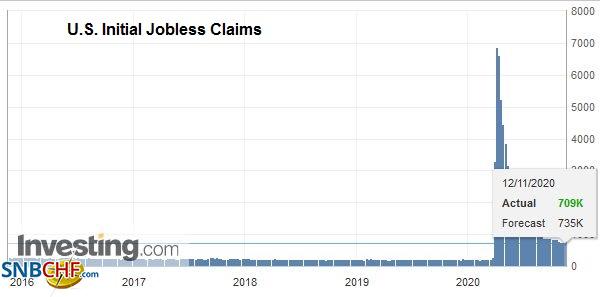

AmericaThe US reports weekly jobless claims, which are expected to have edged lower toward 700k. Many who have exhausted the benefits have qualified for the emergency federal extension, but these programs are set to expire at the end of the year. There is some hope that the appropriations bill, which must be passed by December 11 to avoid a government shutdown, may include an extension, but it is far from certain. The Philadelphia and Kansas Fed’s November manufacturing surveys are also out today, and both are expected to have slowed. October existing-home sales may have pared some of the impressive 9.4% gains in September. The Leading Economic Indicator does not typically draw much attention, and this time it is doubly true as the surging virus and social restrictions make it seemingly less relevant. |

U.S. Initial Jobless Claims, November 19(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

Minority governments last about two years on average in Canada, and Prime Minister Trudeau’s second year is off to a rocky start. The risk of an election early next year went up yesterday after the government lost a 176-146 vote that saw the opposition parties unite to call for a more direct confrontation with China. The non-binding called for the government to officially ban Huawei from its 5G build-out and offer a plan to counter efforts to intimidate Chinese nationals living in Canada. Trudeau says he is waiting for a report from Canada’s intelligence services. However, given that the Five-Eyes intelligence alliance (Australia, New Zealand, the UK, the US, and Canada) have all moved to ban Huawei but Canada.

The US dollar is at a three-day high against the Canadian dollar, a little above CAD1.3100. It looks poised to test the week’s high near CAD1.3140. That also corresponds to the 20-day moving average, which the greenback has not closed above since November 2. Above there, the next target is CAD1.3170-CAD1.3200. The US dollar is also near the highs for the week against the Mexican peso (~MXN20.4340). A push above MXN20.45 could spur a squeeze toward MXN20.65. Support now is seen near MXN20.30.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

The optimism among investors appears to have evaporated in the face of new US-Chinese tensions, possible delays in the next US fiscal stimulus, and new record virus infections in Australia and Hong Kong. US stocks had pared early gains yesterday, and the high-flying NASDAQ finished lower after setting new record highs.

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

A flurry of deals, including the still-evolving Oracle-TikTok tie-up, helped lift equity markets in the Asia Pacific region. South Korea’s Kospi, and Indonesia, which had been battered last week, led the advance. The MSCI Asia Pacific Index rose for the third consecutive sessions. European bourses are little changed while US stocks are firmer.

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

The new week has begun with robust risk appetites, driving stocks and stocks higher and sending the dollar broadly lower. Nearly all the equity markets in the Asia Pacific region gained more than 1%, except Malaysia and Indonesia.

FX Daily, September 09: Investor Anxiety Continues to Run High Despite Some Stability in the Capital Markets

FX Daily, September 09: Investor Anxiety Continues to Run High Despite Some Stability in the Capital Markets

News that the AstraZeneca Phase 3 test had to be stopped to study the adverse reaction of one subject added to the uncertainty of investors amid one of the more significant reversals of risk appetites since March. Equities continued to slump in the Asia Pacific region, with many large markets off more than 1%, led by Australia’s more than 2% decline.

FX Daily, September 16: Dollar Eases Ahead of the FOMC

FX Daily, September 16: Dollar Eases Ahead of the FOMC

Overview: The dollar has been sold against nearly all the world’s currencies ahead of what is expected to be a dovish Federal Reserve, even if no fresh action is taken. The Scandis and Antipodean currencies are leading the majors.

FX Daily, September 29: Consolidation Still Featured

FX Daily, September 29: Consolidation Still Featured

A consolidative tone continues across the capital markets. Equities have lost their momentum. The MSCI Asia Pacific Index was mixed, while Europe’s Dow Jones Stoxx 600 is paring yesterday’s sharp 2.2% gain. US shares are little changed but mostly softer.

FX Daily, October 14: UK Blinks on Threat to Walk Away on Eve of EU Summit

FX Daily, October 14: UK Blinks on Threat to Walk Away on Eve of EU Summit

Overview: Turn around Tuesday saw the dollar bounce, particularly against the Australian dollar and European currencies, among the majors. Sterling pared earlier losses on reports that the UK would not walk away from the talks just yet, while the euro remains on its back foot.

FX Daily, October 19: Sterling Sparkles in Dollar Setback

FX Daily, October 19: Sterling Sparkles in Dollar Setback

Investors have not let the surge of the virus or uncertainty over the UK-EU talks or US fiscal stimulus to stand in their way. Sterling is leading the major currencies higher, returning to the $1.30 area, while global equities are trading higher.

Tags: #USD,Brexit,China,commodities,Currency Movement,EU,Featured,newsletter,Turkey