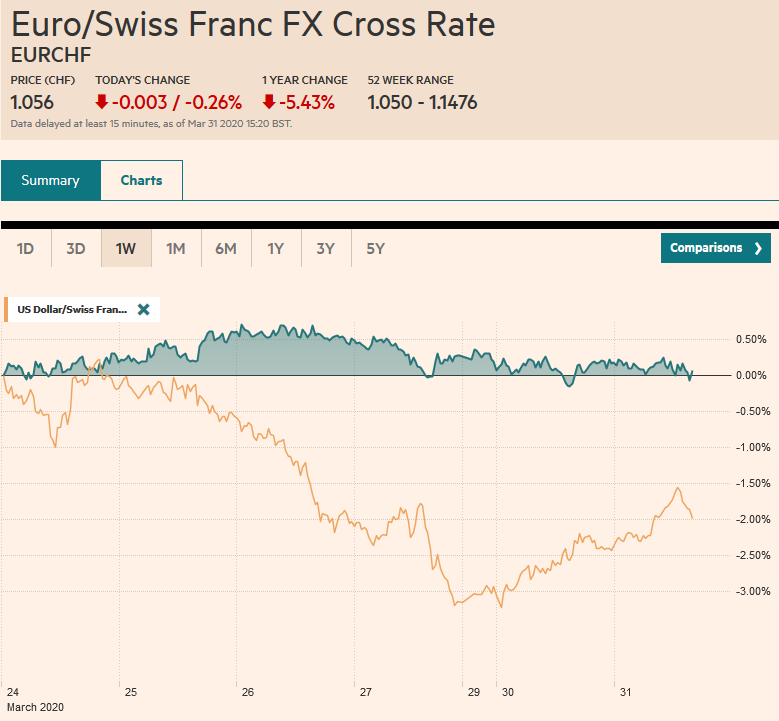

Swiss Franc The Euro has fallen by 0.26% to 1.056 EUR/CHF and USD/CHF, March 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The coronavirus plague upended the world in March. Equities are finishing the month on a firm note. Strong gains in the US yesterday and an unexpectedly strong Chinese PMI (yes, to be taken with the proverbial grain of salt) helped lift most Asia Pacific and European markets today. Japan and Australia are exceptions to the generalization. The Dow Jones Stoxx 600 is slightly higher but appears to be waiting for US leadership to break higher. Benchmark 10-year yields are narrowly mixed. Peripheral European yields are a little softer, while the US 10-year hovers around 70 bp. The dollar

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brazil, China, Featured, Hungary, Mexico, newsletter, Oil, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.26% to 1.056 |

EUR/CHF and USD/CHF, March 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The coronavirus plague upended the world in March. Equities are finishing the month on a firm note. Strong gains in the US yesterday and an unexpectedly strong Chinese PMI (yes, to be taken with the proverbial grain of salt) helped lift most Asia Pacific and European markets today. Japan and Australia are exceptions to the generalization. The Dow Jones Stoxx 600 is slightly higher but appears to be waiting for US leadership to break higher. Benchmark 10-year yields are narrowly mixed. Peripheral European yields are a little softer, while the US 10-year hovers around 70 bp. The dollar saw strong demand at the Tokyo fix, and only the Norwegian krone among the majors is gaining on the greenback. Perhaps it is helped by the bounce in oil, encouraged by expected Chinese refinery demand and so much pressure on some US shale producers, that cooperation with OPEC is being considered. The JP Morgan Emerging Market Currency Index is flat after falling more than 2% over the past two sessions. Gold is softer in the middle of the $1600-$1650 near-term range. |

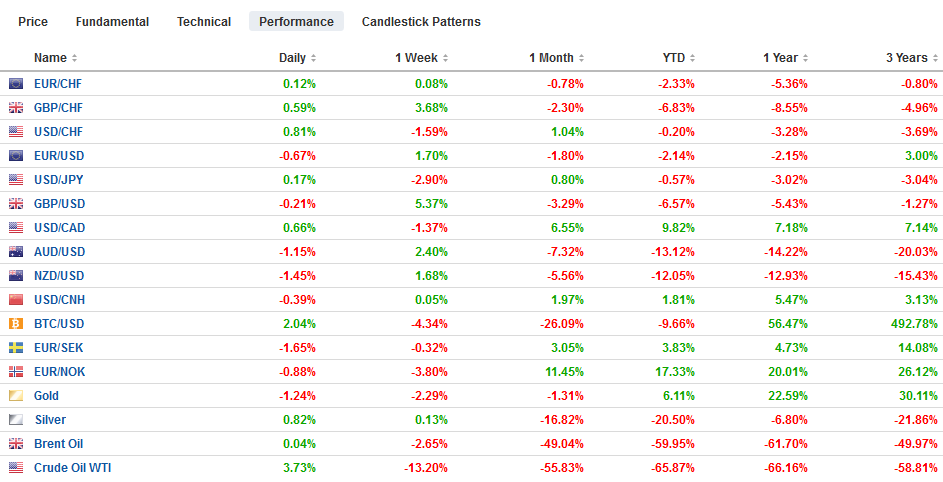

FX Performance, March 31 - Click to enlarge |

Asia Pacific

China’s March PMI surged, and even officials there cautioned against reading too much into it. The questions are phrased relative to the previous month, not pre-crisis. The manufacturing PMI rose to 52.0 from 35.7. A sub-index of export orders rose to 46.4 from 28.7. The non-manufacturing PMI rose to 52.3 form 29.6. Combined, these lifted the composite to 53.0 from 28.9. The take-away is that the Chinese economy is on the mend, and we know from a variety of data, like road traffic, power plant usage of coal, and air quality, that industry is recovering. The broad direction may be more important than the precise location of the recovery.

Japan’s industrial output and retail sales data for February was also better than expected. Industrial production rose by 0.4%, while the median forecast in the Bloomberg survey was for a flat report. Similarly, retail sales had been expected to fall by 1.7% but instead rose by 0.6%. The January rise of 0.6% was revised to 1.5%, suggesting the consumer was recovering from the sales tax increase slump more than had been appreciated. The jobless rate was steady in February at 2.4%, but the job-to-applicant ratio slipped to 1.45 from 1.49, a small hint of what is to come. Separately, we note that South Korea’s February industrial output better than anticipated as well. It fell by 3.8%, whereas the Bloomberg survey expected a 4.5% drop. Tomorrow, South Korea will report March trade figures.

Strong demand for dollars was seen at the Tokyo fix, and the greenback surged to JPY108.70 after having tested the JPY107.70 area yesterday. There are two options expiring today of note. The first is for about $365 mln at JPY108.50, and the second is for nearly $2 bln at JPY109.00. An hourly trendline is found around JPY108.00-JPY108.20 in the North American morning that may offer support. The Australian dollar poked above $0.6200 for the first time since March 16, but this seems to have exhausted the interest. It has traded on both sides of yesterday’s narrow range (~$0.6110-$0.06195), and a close beyond it may be a signal of the near-term direction. The yuan’s reference rate was set slightly weaker than the models’ forecast. Extremely narrow ranges prevailed yesterday and today.

Europe

In a week’s time, the Eurogroup of EMU finance ministers is to have proposals ready for the heads of state to deal with the funding of the emergency. While corona bonds are one option, it does not seem like the most likely. There appears to be some movement to a credit line with the European Stabilization Mechanism for around 2% of GDP. Germany is reported skeptical of unconditional borrowing but seems like it is a starting point. Still, given the magnitude of the spending that is required, and the stock of existing debt, it is not clear that a 2% credit line is sufficient to move most government’s debt and debt servicing needles.

German unemployment rose by 1k in March, and the unemployment rate was unchanged at 5.0%. While Europe may still be trying to figure out a collective approach to the debt, it will likely have a more stable labor market. Several countries have adopted the German practice of the state, absorbing some part of wage costs if employers reduce workers’ hours without dismissing them. Outside of the EMU, the UK and Canada have also unveiled similar programs. The US approach saw over 3 mln people claim unemployment benefits in the week ending March 21 and another surge, perhaps even larger, is expected last week, when data is reported on April 2. Separately, EMU March CPI rose 0.5% on the month, but the year-over-year rate slumped to 0.7% from 1.2%, and the core rate eased to 1.0% from 1.2%. Deflation forces will likely gather steam in the period ahead.

Emergency times call for emergency measures to be sure, but the move in Hungary is breathtaking, and once again, underlines the importance of initial conditions in terms of institutional relations. Prime Minister Orban has been at the forefront of pushing the envelope of illiberal market economies, often bringing it into conflict with the EC. Parliament, yesterday, suspended itself, after declaring a state of emergency and granting Orban unlimited powers. His power to rule by decree is open-ended. Along with all but a handful of emerging market currencies, the forint was sold to start the week. It settled at record low against the euro and is consolidating today. The pattern that the cross has carved looks to be a continuation formation and suggests potential toward HUF268-HUF278. Separately, Poland’s Deputy Prime Minister appears to have been among the first to suggest that the May 10 presidential election should be postponed. The main challenger to the incumbent Duda is called on supporters to boycott the election and suspended her campaign over the weekend.

The euro is pulling back for the second consecutive session after rallying every day last week. It is met the initial retracement (38.2%) objective near $1.0965 today, and the pre-weekend low was almost $1.0950. If this area does not hold, the next retracement (50%) is found closer to $1.09. Expiring options may discourage the upside. There is an option for roughly 760 mln euro at $1.10, and another 520 mln at $1.1015, and nearly 600 mln at $1.1036. That said, North American dealers will return to their desks with the euro over-extended on an intraday basis. Note that there is a 1.5 bln euro option expiring tomorrow at $1.10. Sterling had approached $1.25 in last week’s surge and being sold yesterday, and in Asia today, it reached about $1.2245. It is trying to recover in the European morning but is likely blocked by resistance near $1.24.

America

A fourth US fiscal package is taking shape. It looks to be around $600 bln, and will include more aid to states, the mortgage market, the travel industry, and bolster worker safety. With the Federal Reserve committed to an open-ended Treasury and MBS purchases program, the US debt market shows no concern for the coming supply. The US fiscal efforts are already estimated at around 10% of GDP, which is the most among the major industrialized countries.

While oil output exceeds demand, the problem of storage is growing. Saudi Arabia has signaled a further discount in next month sales from the benchmark rate, nearly doubling it to $6.5. A couple of producers in Texas are lobbying to strike a deal with OPEC, which still seems highly unlikely. There is talk that Cushing is experiencing a huge surge in storage. With falling prices and rising storage costs, producers are at a disadvantage. News that China’s refineries are going to dramatically boost their processing rate helps blunt drop in runs by refineries in India, Canada, and South Africa. Some Indian refiners are citing force majeure to turn down shipments.

Mexico and Brazil have been slow to respond to the COVID-19 threat. It declared a health emergency late yesterday. Separately, the central bank will auction dollars from the Fed swap line tomorrow. Twitter and Facebook removed re-posts by Brazil’s President Bolsonaro on the grounds of harmful misinformation regarding the virus. Both currencies are among the hardest hit in the past month. Both saw record lows. The peso is off about 18.6% this month, and the Brazilian real has depreciated by nearly 14%.

The US dollar is firmer against the Canadian dollar today despite the rise in oil and firm equities. At CAD1.4200, the greenback has retraced (38.2%) of the recent decline. The next retracement (50%) is found closer to CAD1.4300. The US dollar is over-extended on an intraday basis. Initial support is seen near CAD1.4200 now, and below there, support is seen by CAD1.4160. The greenback is consolidating yesterday’s gains against the peso. It appears to be forging a near-term range between MXN23.50 and MXN24.50.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, October 14: Optimism Took the Weekend Off

FX Daily, October 14: Optimism Took the Weekend Off

Overview: Japanese and Canadian markets are on holiday today. While the US bond market is closed, equities maintain their regular hours today. Asia Pacific equities rallied, led by 1% of more gains in China, Taiwan, South Korea, and Thailand. The buying did not continue in Europe, and after a 2.3% rally before the weekend, the Dow Jones Stoxx 600 is about 0.75% lower in the European morning.

FX Daily, October 31: No Good Deed Goes Unpunished

FX Daily, October 31: No Good Deed Goes Unpunished

Overview: The equity and bond rally in North America yesterday carried over into today’s session. With some notable exceptions, like China, Taiwan, Australia, and Indonesia, most bourses in Asia Pacific and Europe traded higher. US shares are little changed in early Europe after the S&P 500 rose to new record highs.

FX Daily, January 9: Animal Spirits Roar Back

FX Daily, January 9: Animal Spirits Roar Back

Overview: The S&P 500 recovered from a 10-day low to reach a new record high, which set the tone for the Asia Pacific and European markets today. The MSCI Asia Pacific Index jumped by the most in a month with the Nikkei’s 2% advance leading the way. More broadly, the markets in Taiwan, South Korea, Hong Kong, India, and Thailand all rose more than 1%.

FX Daily, February 5: Markets Extend Recovery, but Look for a Pause

FX Daily, February 5: Markets Extend Recovery, but Look for a Pause

Overview: The S&P 500 gapped higher and surged 1.5% yesterday, the most since in six months, helping set the stage for a continued recovery in global equities, and stoked risk appetites more broadly. An experimental antiviral treatment is to begin clinical testing. All of the markets in the Asia Pacific region advanced, with Japan, China, and Singapore gaining more than 1%.

FX Daily, February 13: Surprise? China Undercounts Afflictions and Fatalities, Curbs Risk Taking

FX Daily, February 13: Surprise? China Undercounts Afflictions and Fatalities, Curbs Risk Taking

Overview: There is one overriding driver today, and that is the incorporation of CAT scan diagnoses of the virus in Hubei, ground-zero. This follows the arrival of WHO officials into China a couple days ago. Not only have the cases jumped, but so did the number of deaths. It plays on fears that China’s figures are not reliable. But it is not just China.

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

Overview: The ring of containment of Covid-19 has grown from China. The new frontline is Japan, South Korea, Italy, and Iran. A lockdown of around 50k people near Milan and Austria blocking trains from Italy is scaring investors. Asian markets fell, but South Korea bore the brunt with a nearly 4% decline. The national holiday in Japan spared local equities.

FX Daily, February 25: Capital Markets Remain Fragile after Yesterday’s Bloodletting

FX Daily, February 25: Capital Markets Remain Fragile after Yesterday’s Bloodletting

Overview: Yesterday’s bloodletting in global equities has calmed, but investors remain on edge. Despite all the concerns that the markets were under-appreciating the implications of the new coronavirus, there is a sense that yesterday’s moves were in excess. Japanese markets, which were closed on Monday, played catch-up today, and the Nikkei shed 3.3%.

FX Daily, April 2: Optimism on Oil Deal Steadies Risk Appetites…for the Moment

FX Daily, April 2: Optimism on Oil Deal Steadies Risk Appetites…for the Moment

Overview: After US stocks dropped more than 4% yesterday, investor sentiment has improved, apparently sparked by ideas that the pain will force oil producers to find a way to reduce supply. Oil prices have surged, with the May WTI contract rallying around 7%. Asia Pacific equities were mostly higher, with Japan and Australia the notable exceptions.

Tags: #USD,Brazil,China,Featured,Hungary,Mexico,newsletter,OIL