Swiss Franc The Euro has risen by 0.27% to 1.0584 EUR/CHF and USD/CHF, March 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Bottom-picking, after officials step up efforts and some optimism creeps in, is helping lift spirits today. As one looks at the equity bounces, it is important to remember that among the biggest rallies take place in bear markets. Nearly all the bourses in Asia-Pacific rallied, led by a 7% advance by Japan’s Nikkei and an 8%+ surge in South Korea’s Kospi. Most other markets were up 2%-5%. Europe’s Dow Jones Stoxx 600 is up nearly 5% after falling 4.3% yesterday. US stocks are firmer, and early indications suggest a 3%-4% early gains. Bond markets are much quieter, and most benchmark

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, cross currency basis swap, Currency Movement, Featured, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.27% to 1.0584 |

EUR/CHF and USD/CHF, March 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

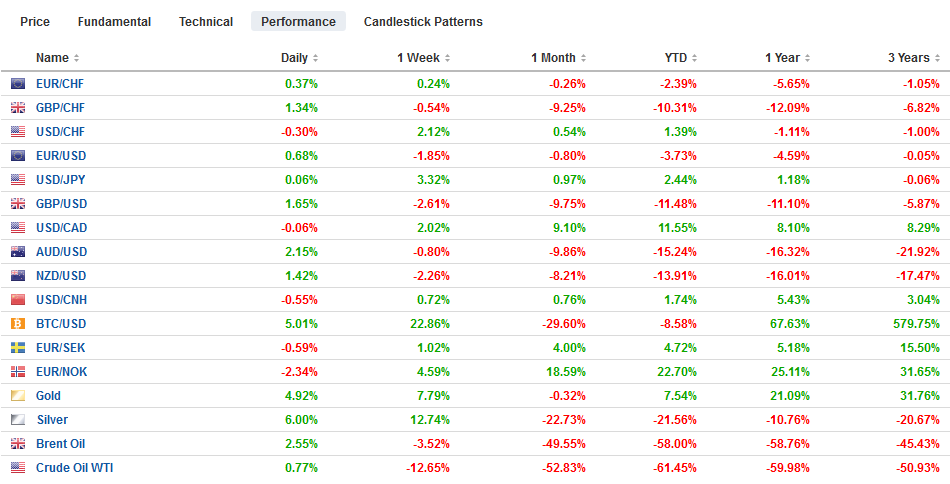

FX RatesOverview: Bottom-picking, after officials step up efforts and some optimism creeps in, is helping lift spirits today. As one looks at the equity bounces, it is important to remember that among the biggest rallies take place in bear markets. Nearly all the bourses in Asia-Pacific rallied, led by a 7% advance by Japan’s Nikkei and an 8%+ surge in South Korea’s Kospi. Most other markets were up 2%-5%. Europe’s Dow Jones Stoxx 600 is up nearly 5% after falling 4.3% yesterday. US stocks are firmer, and early indications suggest a 3%-4% early gains. Bond markets are much quieter, and most benchmark yields are 3-5 bp higher. The dollar is seeing its recent gains pared. The Norwegian krone has been the weakest of the majors, and it is leading the move today with a nearly 6% gain, while the yen and Canadian dollar are the laggards, gaining around 0.7%. Among emerging market currencies, the Mexican peso has been exceptionally pressured, and it nearly 2.5% higher, while the JP Morgan Emerging Market Currency Index is about 0.25% higher. Gold is extending its recovery for a third session, over which time it is up around $110 an ounce. Its roughly 7.5% gain has been matched by the two-day advance in oil prices, May WTI settled last week near $22.65 and is now trading near $24.35. |

FX Performance, March 24 - Click to enlarge |

Asia Pacific

Japan’s preliminary March composite PMI fell to 35.8 from 47.0. This reflected a fall in the manufacturing PMI to 44.8 (from 47.8) and the services PMI to 32.7 from 46.8. Japan’s economy had contracted in Q4 under the weight of the sales tax hike and damage from the tsunami. A recovery in Q2 is hoped for, but many several things have to fall into place first. The equity advance today, the most in four years, was helped by nearly 20% rally in Softbank, which announced plans to raise some $4.5 bln, with roughly half to be used for share buybacks.

Japanese banks have been large users of the dollar swaps the Fed makes available to the Bank of Japan. After taking $35 bln at yesterday’s seven-day swap auction, they took almost $90 bln today. In the three auctions under the modified rules (OIS+25 bp), Japanese banks have taken around $150 bln. Around minus 92 bp below LIBOR, the three-month cross-currency swap is still extreme. It was above -20 bp before the crisis broke.

In other regional developments: South Korea announced a KRW48.5 trillion (~$38.5 bln) package to stabilize the financial markets, including funds to support the bond and stocks market and provide liquidity. Malaysia imposed a temporary ban on short-sales, and the Philippines cut reserves requirements by 200 bp, which frees up about PHP300 bln. China said the lockdown for Wuhan could be lifted on April 8.

The use of the Fed’s swap lines have not eased the demand for dollars against the yen in the spot market. The dollar held above JPY110 in Toyko and is flirting with JPY111 in Europe. It reached almost JPY111.60 yesterday and has been up to JPY111.35 today. There are around $2.5 bln in expiring options between JPY111.30 and JPY111.60. The Australian dollar is trying to extend its recovery into a third session. It bottomed last week near $0.5500 and reached $0.5975 in late Asia today before consolidating in the European morning. If the $0.6000 area can be overcome, the next target is near $0.6100. The US dollar traded softer against the Chinese yuan and finished the mainland session, lower for the third consecutive session. The dollar settled last week near CNY7.0960 and ended the Shanghai session around CNY7.0760.

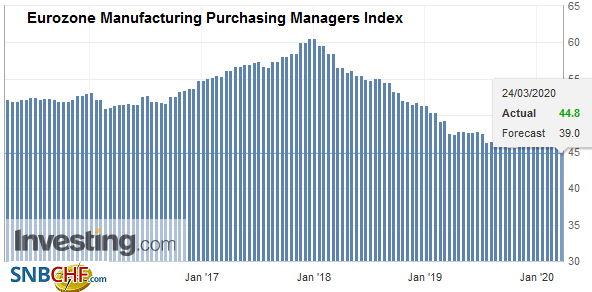

EuropeThe preliminary European PMIs are weaker than expected. The manufacturing PMIs, though, held up better than anticipated, due it appears to a statistical quirk of how longer delivery times are calculated of the diffusion index. There should be no mistake, though that a steep economic contraction is underway. On the aggregate level, the EMU manufacturing PMI fell to 44.8 from 49.2. |

Eurozone Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on Eurozone Manufacturing Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

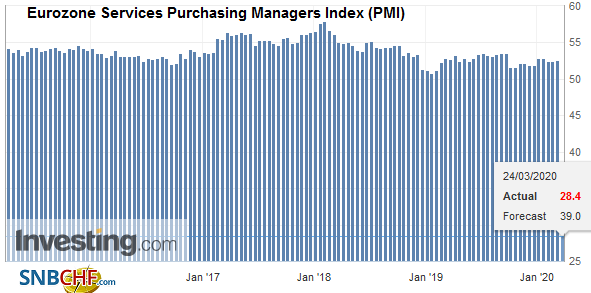

| The service PMI fell to 28.4 from 52.6. This saw the composite tumble to 31.4 from 51.6. |

Eurozone Services Purchasing Managers Index (PMI), March 2020(see more posts on Eurozone Services Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

| This general pattern was repeated in Germany and France, and also seen in the UK. The German manufacturing PMI eased to 45.7 from 48.0, while the service PMI dropped to 34.5 from 52.5. The composite stands at 37.2, down from 50.7. |

Germany Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on Germany Manufacturing Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

| The French composite stands at 30.2 after a 52.0 reading in February. This was the result of the slip in the manufacturing PMI to 42.9 from 49.8 and a drop in the services PMI to 29.0 from 52.5. Economists appear to be looking at a 5%-8% quarterly contractions. |

French Markit Composite Purchasing Managers Index (PMI), March 2020(see more posts on French Markit Composite Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

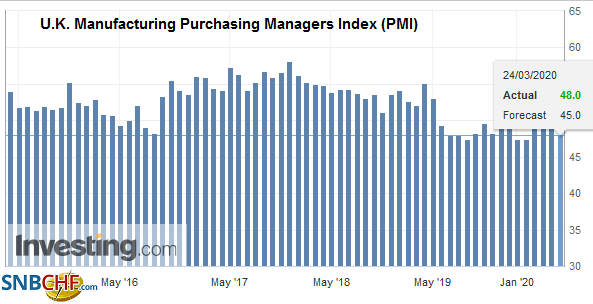

| In the UK, the preliminary estimate for the composite PMI fell to 37.1 from 53.0. Manufacturing dipped to 48.0 from 51.7, while the service PMI fell to 35.7 from 53.2. Separately, after first embracing the “herd containment” strategy until realizing it would overwhelm the UK’s medical capacity, the Johnson government has rapidly reversed itself and, on top of significant fiscal efforts, has announced three-week lockdown. |

U.K. Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on U.K. Manufacturing Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

Although Merkel says Germany is open to discuss a joint bond issuance, it is not ready to embrace it yet. Italy, where the fatality rate is near 8.5%, is in need of help. However, Germany is advocating that Italy is granted an enhanced credit line with the European Stabilization Mechanism, which would then allow it to trigger the Outright Market Transactions (OMT). OMT allows for ECB bond purchases. Merkel seemed sympathetic to light conditionality. The challenge here is that Italy has structural problems that need to be addressed. Separately, fatalities in Italy appear to have fallen for a second day, while hospitalization in the hard-hit Lombardy region slowed.

The euro has based in the last two sessions near $1.0635. It is around $1.0860 in the European morning, where a 1.1 bln euro option is expiring today. The next chart points are seen in the $1.09 area and then $1.0940. Seven EMU banks took $4.12 bln at the daily seven-day swap auction. This is up from a lowly $20 mln yesterday, and the three-month cross-currency basis swap has normalized. Sterling is firm, but within yesterday’s range (~$1.1450-$1.1740). A move above $1.18 would bring the $1.1935 area, seen on March 20 into view.

AmericaThe Federal Reserve continues to offer new measures of financial and economic support, and despite claims that it is “all in,” there is more that will do. Yesterday, it announced open-ended purchases and an aggressive action plan this week to buy $375 bln of Treasuries and $250 of mortgage-backed securities. The Fed is setting up a special purpose vehicle, like it did for commercial paper, for asset-backed securities, and for the first time, corporate bonds. Each SPV is funded by $10 bln from the Treasury’s exchange stabilization fund. A new SPV is expected to be announced shortly that would support small and medium-sized businesses. Meanwhile, the debate over fiscal efforts continues, and, optimistically, a resolution may be seen before the end of the week. The House Democrats have drafted a $2.5 trillion alternative to the White House/Senate version. The House’s plan calls on a temporary reprieve from personal debt (credit cards, mortgages, and car payments, and a $10k maximum write-off of student debt. |

U.S. Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on U.S. Manufacturing Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

The Bank of Canada is expanding the range of assets it can buy and sell to include corporate and local government bonds. Mexico’s President AMLO is opposed to granting company bailouts or tax amnesty. Brazil’s President Bolsonaro indicated that yesterday’s decree that allows companies to halt work contracts for four months without salary payments (that helped send BRL to new record lows yesterday) will be revoked.

The US dollar is softer but within the range seen yesterday against the Canadian dollar (~CAD1.4335-CAD1.4660). A break of yesterday’s lows could see CAD1.4150. Initial resistance now is seen near CAD1.4450. The greenback rose to a new record high (~MXN25.4585) before reversing lower. Yesterday’s low was near MXN24.36, though initial support may be encountered around MXN24.50.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, March 17: Even Turn Around Tuesday is Flat

FX Daily, March 17: Even Turn Around Tuesday is Flat

Overview: While the markets are not as disorderly as they have been, the tone is fragile, and the animal spirits have been crushed. Australian stocks fell more than 10% last week and dropped another 9.7% yesterday before rebounding by almost 6% today to be one of the few Asia Pacific equity markets to rise. The Nikkei eked out a small gain, but the broader Topix rose 2.6%.

FX Daily, March 16: Monday Blues: Fed Moves Bigly and Stocks Slump

FX Daily, March 16: Monday Blues: Fed Moves Bigly and Stocks Slump

Overview: The Federal Reserve and central banks in the Asia Pacific region acted forcefully, but were unable to ease the consternation of investors. The Reserve Bank of New Zealand cut key rates by 75 bp. The Bank of Japan appears to have doubled its ETF purchase target to JPY12 trillion, and the Reserve Bank of Australia is preparing for new measures that will be announced Thursday.

FX Daily, March 18: Bonds Join Equities in the Carnage

FX Daily, March 18: Bonds Join Equities in the Carnage

Overview: A new phase of the market turmoil is at hand. Bonds are no longer proving to be the safe haven for investors fleeing stocks. The tremendous fiscal and monetary efforts, with more likely to come, have sparked a dramatic rise in yields. Meanwhile, equities are getting crushed again.

FX Daily, March 19: ECB’s Bazooka Support Bonds but not the Euro

FX Daily, March 19: ECB’s Bazooka Support Bonds but not the Euro

Overview: It is not just that the dollar soared while stocks and bonds continued to plunge. The dollar’s strength is, in effect, a powerful short-covering rally. It was used to fund a great part of the global circuit of capital. The circuit of capital is in reverse now, and the funding currency is being bought back. The dollar’s strength is a function of the sell-off of other assets.

FX Daily, March 20: Markets Ending the Week on Better Note

FX Daily, March 20: Markets Ending the Week on Better Note

Overview: Dramatic price action continues but in the other direction. Stocks and bonds have rallied strongly, and the US dollar is snapping a strong advance with a sharp and broad setback. The immediate trigger is hard to identify. Some accounts linking it to fears that the California shutdown will be repeated throughout the country, deepening the coming downturn.

FX Daily, March 23: Greenback Demand Not Satisfied by Swap Lines

FX Daily, March 23: Greenback Demand Not Satisfied by Swap Lines

Overview: In HG Wells’ "War of the Worlds," the common cold repelled a Martian invasion. Now, a novel coronavirus is disrupting everything and everywhere. Global equities continue to get hammered, though the apparent relative resilience of Japan may have spurred some buying of Japanese equities.

FX Daily, October 21: Dollar Soft, but Stage is being Set for Turn Around Tuesday

FX Daily, October 21: Dollar Soft, but Stage is being Set for Turn Around Tuesday

Overview: The UK’s departure from the EU remains up in the air as a new attempt to pass the necessary legislation through Parliament continues today. Many market participants seem to remain optimistic that Prime Minister Johnson’s plan will ultimately succeed. After slipping to $1.2875 initially, sterling briefly pushed through $1.30, which had held it back last week.

FX Daily, November 5: Animal Spirits Remain Animated

FX Daily, November 5: Animal Spirits Remain Animated

The prospects that the US-China deal could include some rolling back of existing US tariffs helped underpin risk appetites. After new record highs in the US S&P 500 and NASDAQ, Asia Pacific markets marched higher, and the MSCI Asia Pacific reached its highest level since August 2018. A small rate cut by China and catch-up by Tokyo, which was on holiday on Monday, helped extended the regional rally for the 14th session in the past 17.

Tags: #USD,cross currency basis swap,Currency Movement,Featured,newsletter