Swiss Franc The Euro has risen by 0.05% at 1.1135 EUR/CHF and USD/CHF, July 08(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The capital markets have begun the week in a mixed note. Asia Pacific equities tumbled, led by 2%+ losses in China and South Korea, but European shares are edging higher, and a positive close would be the seventh in the past eight sessions. The S&P is little changed. Asia Pacific bond yields moved higher, as anticipated after the jump in US yields after the jobs data. European bonds are slightly firmer, except in Italy and Spain, where the benchmarks are paring recent gains. Greek debt has rallied in response to the election results

Topics:

Marc Chandler considers the following as important: $CNY, $TRY, 4) FX Trends, EUR/CHF, Featured, FX Daily, newsletter, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.05% at 1.1135 |

EUR/CHF and USD/CHF, July 08(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The capital markets have begun the week in a mixed note. Asia Pacific equities tumbled, led by 2%+ losses in China and South Korea, but European shares are edging higher, and a positive close would be the seventh in the past eight sessions. The S&P is little changed. Asia Pacific bond yields moved higher, as anticipated after the jump in US yields after the jobs data. European bonds are slightly firmer, except in Italy and Spain, where the benchmarks are paring recent gains. Greek debt has rallied in response to the election results that saw Syriza defeated by New Democracy, along the lines the polls had signaled. US 10-year Treasury yield is consolidating the pre-weekend move that lifted it back above 2%. The dollar is sporting a slightly heavier profile, with the Scandis and Antipodeans leading way with 0.2%-0.3% gains. The Turkish lira is off nearly 2% following Erdogan dismissal of the central bank governor. Gold and oil are firmer. |

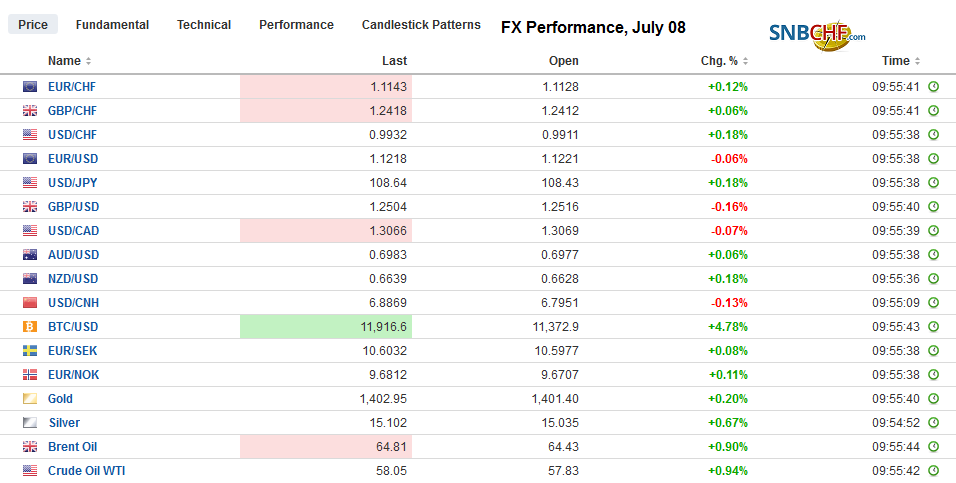

FX Performance, July 08 - Click to enlarge |

Asia Pacific

Japan reported a smaller current account surplus and a drop in core machine orders. The more modest external surplus reflects the deterioration in Japan’s trade balance. The deficit on the balance of payments basis rose to about JPY650 bln from less than JPY100 bln in April. Japan has recorded an average trade deficit of JPY107 bln this year compared with JPY192 bln average in the first five months of last year. Separately, Japan’s three-month rising machinery orders came to a screeching halt in May with a nearly 8% drop, twice the decline expected by economists. Last week, Japan reported stronger household consumption, but that could be some front running ahead of the October 1 sales tax hike to 10% from 8%.

China’s reserves rose by $18 bln to $3.119 trillion. It is the highest since last April and likely reflects valuation adjustments and capital inflows, rather than intervention to weaken the yuan. The way the PBOC set the reference rate last month suggests that it had been leaning against modest downside pressure on the yuan. China also reported its first monthly increase in auto sales this year. New discounts may have helped, but also some cities granted more licenses too.

The dollar is consolidating in the upper end of the pre-weekend range. It met offers in Tokyo near JPU108.60 but found support in Europe ahead of JPY108.25, where a roughly $770 mln option is struck and will expire in the US today. Around $1.25 bln in options in the JPY108.00-JPY108.15 area may offer support for the greenback. The Australian dollar is also consolidating its pre-weekend decline and has been confined to a quarter of a cent below $0.7000. Nearby support is seen in the $0.6950-$0.6965 area. The US dollar initially edged up against the Chinese yuan, edging through last week’s highs but slipped as the session progressed to finish the local session near CNY6.88.

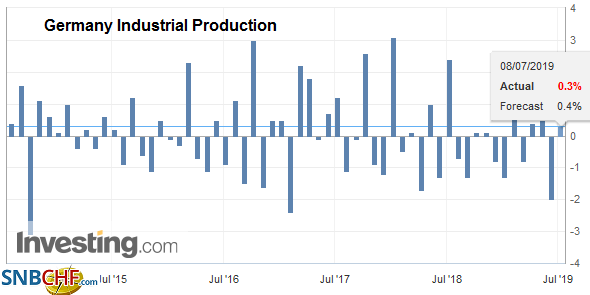

EuropeAfter German factory orders tumbled 2.2% in May, the market was prepared for a poor industrial production report. It did not turn out as bad as feared. Industrial output edged up 0.3% after the April decline was revised to -2.0% from -1.9%. Germany also reported a stronger than expected rise in exports (1.1%) after a substantial decline (-3.4% in April, revised from -3.7%). Imports unexpectedly fell (-0.3%) rather than increase by 0.5% as the median Bloomberg survey forecast anticipated. |

Germany Industrial Production, May 2019(see more posts on Germany Industrial Production, ) Source: investing.com - Click to enlarge |

Johnson appears to have solidified his lead to become the next Tory leader, securing Javid’s support. This has spurred speculation that Javid will replace Hammond as the Chancellor of the Exchequer. The results of the rank-and-file vote are still two weeks away. Although the agreement with the DUP is to run the course of the parliament session, it does not seem ironclad. A new government committed to getting rid of the backstop, which ostensibly risks the Good Friday Agreement would seem to violate a key part of the agreement. Johnson refuses to rule of propagation, which would end the parliament session. The risk of a no-deal exit continues to weigh on sterling sentiment.

The firing of Turkey’s central bank governor may bring forward the rate cut that Erdogan is demanding, but the market does not like the interference and sold the lira. The dollar had trended lower against the lira in May and June and lost nearly 3% over those two months. The greenback slipped to its lowest level since early April last week (~TRY5.5850), but in the illiquid Asian timezone, when investors got their first chance to respond, the dollar was marked up to nearly TRY5.8250. The lira recovered, but the dollar found support a little below TRY5.71. In Europe the five-year credit default swap also rose 395 bp from 375 bp before the weekend.

The euro fell a little below $1.1210 after the US employment data and has barely been able to recover. It reached almost $1.1235 in Europe, but there is not much of an appetite. The 2.1 bln euros in expiring options struck between $1.1250 and $1.12665 will likely be a sufficient cap today. Sterling was driven below $1.25 before the weekend and has resurfaced above there today to reach almost $1.2540. The intra-day technicals show little enthusiasm for stronger gains. Initial resistance is seen near $1.2560.

America

Fed chair Powell’s testimony before Congress Wednesday and Thursday has taken on greater significance after the constructive employment report. Some fear that if the Fed delivers a rate cut in July, it would be seen as capitulating to the presidential bullying. On the other hand, if the Fed does not deliver a rate cut it, others fears that the disruption to the market would make a September cut inevitable. We have argued the institutional strength differentiates the US from many developing countries, such as Turkey. The unusual explicit pressure from Trump has been resisted reduces the likelihood that a rate cut now would be seen as the loss of the central bank’s independence.

The tension between Japan and South Korea is not America’s doing, but one could imagine a different kind of American president exerting leadership to quell the tension between two allies. Our sense is that both Japan and South Korea will be harmed by the dispute, but like the US and China dispute, it will spur South Korea to strengthen its own semiconductor materials market. Japan’s use of trade to punish South Korea over a non-trade issue seems to be a page from the US playbook. Indeed, there are some reports today that suggest China may take another page from Trump’s playbook and challenge trade with some US companies on national security grounds.

It is a light calendar day for North America. The Canadian dollar is in stuck in a narrow range, and a chunky option for $1.3 bln at CAD1.31 is likely sufficient to deter a stronger US dollar recovery. The Bank of Canada meets in the middle of the week, and while there won’t be a change in policy, the confidence that the soft-patch is in the rearview mirror may have been bolstered by the recent data. For a third session, the dollar is straddling the MXN19.00 level. The consolidation, even if there is some range extension, looks poised to continue. The peso and the yuan are competing today for the strongest emerging market currency.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CNY,$TRY,EUR/CHF,Featured,FX Daily,newsletter,USD/CHF