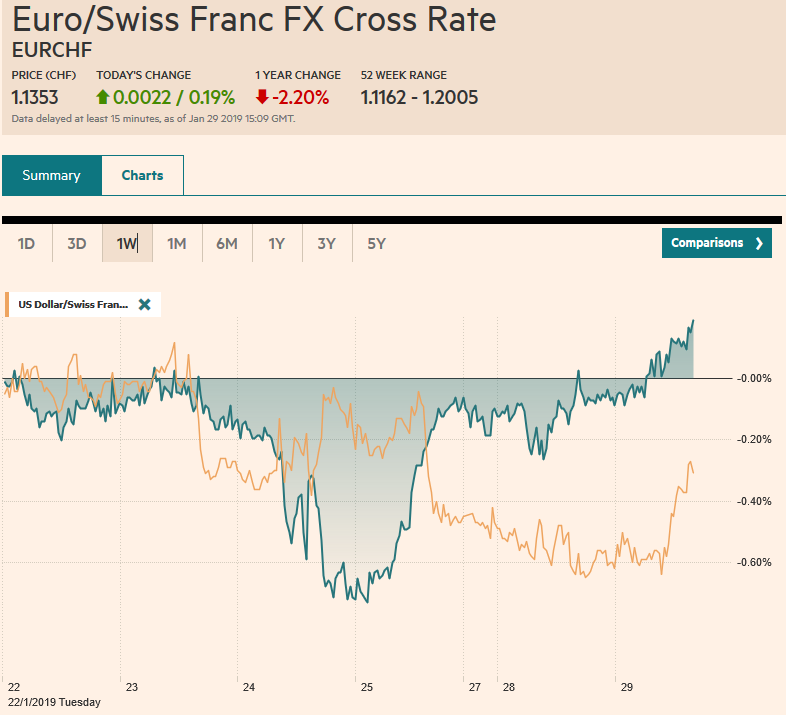

Swiss Franc The Euro has risen by 0.19% at 1.1353 EUR/CHF and USD/CHF, January 29(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The positive impulse in the capital markets seen last week has faded. The gap higher opening ahead of the weekend by the S&P 500 was follow by a gap lower opening yesterday. The US threatened crackdown on Huawei disrupted equities in that sector, with as many as two dozen companies on the Shenzhen exchange that were limit down (10%). Most Asia Pacific equity markets, but Japan and South Korea moved lower. European equities are edging higher late in the morning session. US equities are little changed. Peripheral European bonds

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, CAD, EUR, EUR/CHF and USD/CHF, Featured, GBP, JPY, MXN, newsletter, SPX, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.19% at 1.1353 |

EUR/CHF and USD/CHF, January 29(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The positive impulse in the capital markets seen last week has faded. The gap higher opening ahead of the weekend by the S&P 500 was follow by a gap lower opening yesterday. The US threatened crackdown on Huawei disrupted equities in that sector, with as many as two dozen companies on the Shenzhen exchange that were limit down (10%). Most Asia Pacific equity markets, but Japan and South Korea moved lower. European equities are edging higher late in the morning session. US equities are little changed. Peripheral European bonds continue to outperform, even in Greece which is set sell 2 bln euros in new five-year bonds through syndication. The dollar is little changed but with a lower against the majors, and the emerging market currencies are mixed, with the volatile Turkish lira and South African rand among the weakest. Gold moved above $1300 an ounce yesterday and is extending those gains today to trade at a new seven-month high. |

FX Performance, January 29 - Click to enlarge |

Asia Pacific

The US is set to bring extensive charges against China’s Huawei, including allegedly paying employees for stealing technology secrets. Reports suggest that the exclusion of Huawei could set back the rolling out of 5G in Europe. Chip and equipment makers were sold. This is coinciding with the earnings season as well. Today Apple, AMD, and 3M report in the US. SAP already reported and although it met all the raised outlooks, the forward guidance was poor. Earlier TSMC reported its suppliers agreed to cut prices by 10% after the company reported weak revenue growth.

Separately, the economic slowdown in China, beyond what the official data imply, is taking a toll on corporate earnings from US, European and Japanese companies.

The Chinese yuan has appreciated for five consecutive sessions through today. China does not confirm the weighting of the basket is tracks the yuan against (CFETS). Bloomberg’s attempt to duplicate it finds that the yuan has appreciated against the basket after trading in a range recently. Some are linking the yuan’s appreciation to optimism on the trade front. To the contrary, we see the yuan’s appreciation as an effort by Chinese officials to ensure the trade talks are not distracted by short-term moves in the foreign exchange market.

The press gives little reason to be optimistic on trade. The talks are resuming but the action against Huawei is unlikely to contribute positively to the discussion, and likely underscore the US commitment to ensuring the agreements are verifiable and that deep structural reforms are needed. Meanwhile, it does not sound like negotiating positions have changed. China is willing to buy more US energy and agriculture goods. It continues to resist calls for fundamental changes in China industrial policy.

The dollar found support for the second day a little above JPY109.00. It appears stuck in a range that is marked by expiring options. At JPY109, a roughly $400 mln option expires today and at JPY109.50, another $550 mln is struck. The Australian dollar reversed after briefly poking through $0.7200 yesterday, closing near $0.7165. The losses were extend to almost $0.7135 before bids were found, allowing the Aussie to recoup the earlier decline. Initial resistance is seen near $0.7180. New Zealand reported a larger than expected trade surplus, but it was largely offset by a revision to the November series showing a larger shortfall. Exports rose while imports fell. The Kiwi’s gains appeared to lose momentum in the European morning as yesterday’s high were approached.

Europe

The UK debate over its plan to leave the EU takes what seems like a dangerous step and one that make sterling appear vulnerable after a six-week rally. We have argued that the Brexit issue is a like a scissors. The close the government is to striking a deal with the EC, the further is is away from Parliament. That was May’s Plan A–the negotiated deal with the EC. This was rejected. Plan B is for May to move back toward Parliament. Specifically that means questioning the backstop and its duration with the Irish border. The Prime Minister is encouraging MPs to vote for the Brady Amendment that allows alternative arrangements. However, and this is important, the EC and Ireland have rejected both re-opening negotiations and limiting the backstop. There seems to be a discussion of Plan C, which would entail extending the transition period to increase the likelihood of a solution for the Irish border. Yet the alternatives seem quite limited, if there is to be no hard border between Northern Ireland and the Irish Republic and no separation of Northern Ireland and the rest of Britain.

The euro is extending its recovery after easing below $1.13 on the back of the unexpectedly dovish ECB, which for the first time, changed its risk assessment without the benefit of updated staff forecasts. The economic data has apparently been so weak as to make new forecasts superfluous. The euro is trading new two-week highs and is approaching a retracement objective of the decline since pushing to $1.1575 in the middle of the month. That objective, near $1.1465 holds a nearly 530 mln euro option that is expiring today. There are also about 1.2 bln euros in options struck between $1.1410 and $1.1415 that also expire today. Over the last couple of weeks, short-term traders have been frustrated by the lack of follow-through after breaking out of the $1.13-$1.15 range. They do not want to be bit by the same dog again and look for them to take profits as the upper end of the range is neared. Sterling is consolidating its strong gains at the end of last week, when it traded between roughly $1.3060 and $1.3220. It found new interest near $1.3130 today, a few ticks below yesterday’s lows. There are a couple of options, each for about GBP230 mln at $1.3175 and $1.3200 that expire today. A break of $1.3025 may be the first sign that a top of some import may be in place. After dropping from GBP0.9100 at the start of month to nearly GBP0.8600 at the end of last week, the euro, from a technical perspective, looks set to begin recovering.

Americas

US sanctions against PDVSA will add pressure on Maduro. Not only won’t the US buy Venezuela oil, but it will prevent the sale of naphtha, which is needed to breakdown Venezuela’s heavy crude. The US opposition to Maduro seems to almost automatically trigger supportive action by China and Russia, who may buy Venezuela’s oil. Most US refiners are used to Venezuela’s heavy crude, but the US can replace it via Mexico, and perhaps some Middle East producers, though Saudi Arabia is reportedly cutting shipments to the US.

Separately, API reports US oil inventories ahead of the EIA’s estimate tomorrow. Participants are looking for around a 3 mln barrel build. Last week the EIA reported a nearly 8 mln barrel build, the largest in a couple of months. March WTI fell more than 3% yesterday, its largest decline since around Christmas. It is about 1% higher today, but remains in a $50-$55 trading range that has confined the price action for the better part of three weeks.

The collapse of a dam in Brazil took a toll on Vale, with estimates of damages extending to $7 bln. Vale dragged down the materials sector in the Bovespa yesterday, which pressured the entire index, even though most of the other sectors, but health care advanced. Still, the enthusiasm among investors for Brazil under Bolsonaro appears to remain intact and the Bovespa’s 8.6% gain this month is among the best in the world.

With the US government re-opening, the back data will begin being reported, though a schedule has not yet been announced. In some ways, after tomorrow’s first look at Q4 GDP, the data from last year is less important. Data for January is still limited and weakness spurred by the disruption of the partial government shutdown is expected to be reversed.

The US dollar is consolidating its losses against the Canadian dollar seen at the end of last week, when it approached CAD1.32, which held yesterday. The greenback needs to get back above CAD1.33 to stabilize the tone. The dollar continues to hover around MXN19.00. Watch the MXN19.16 area. The 20-day moving average is found near there and the dollar has not closed above the moving average since early November. The Dollar Index rose to around 96.65 on the back of the ECB last week. It has approached 95.60 today. Unless 96.00 is re-taken, the risk is for the Dollar Index to retest on this month’s low near 95.00. The S&P 500 gapped on January 18 and was quickly filled in next session. On January 25 the S&P 500 again gapped higher, However, yesterday the gap was not filled. To the contrary, the S&P 500 gapped lower, leaving a one-day island in its wake. This is seen by technicians as a bearish development. However closing yesterday’s gap and neutralizing the negative require the S&P 500 trade above last Friday’s low near 2657.3.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,EUR/CHF and USD/CHF,Featured,MXN,newsletter,SPX