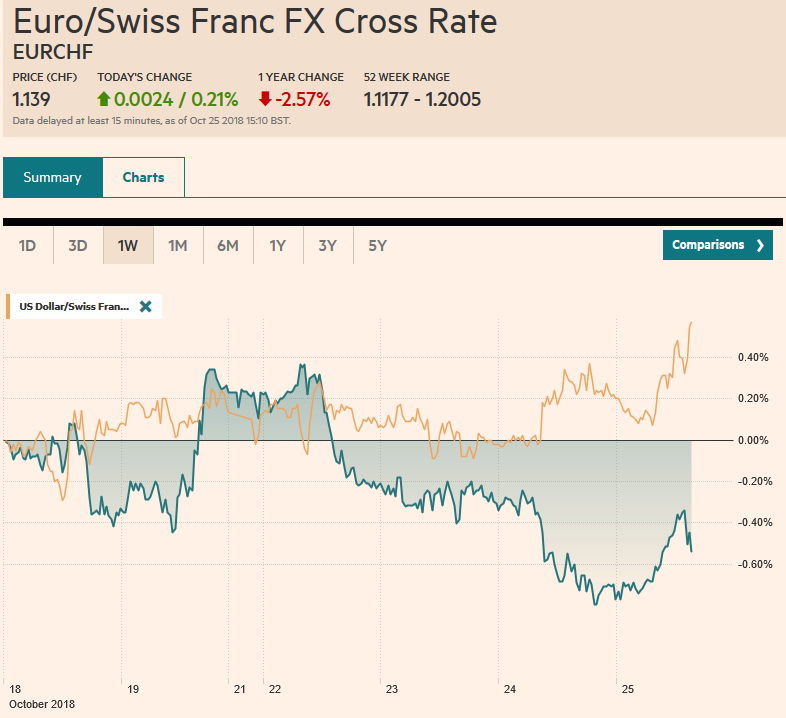

Swiss Franc The Euro has risen by 0.21% at 1.139 EUR/CHF and USD/CHF, October 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates FX: The Dollar Index broke above 96.00 yesterday and is consolidating today. Provided the 96.00 area holds, the next target is the year’s high near 97.00. The euro has been confined to a little more than a quarter of a cent. Players seem reluctant to sell it below .14 and note there is a 570 mln euro option at .1420 that expires today. Sterling is straddling the .29 level, and intraday technicals warn of the risk of a retest of yesterday’s low near .2865. The dollar initially fell in Asia to test JPY111.80 but recovered in late-Asia

Topics:

Marc Chandler considers the following as important: 4) FX Trends, CAD, ECB, EUR, Featured, GBP, JPY, MXN, newsletter, SPX, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.21% at 1.139 |

EUR/CHF and USD/CHF, October 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesFX: The Dollar Index broke above 96.00 yesterday and is consolidating today. Provided the 96.00 area holds, the next target is the year’s high near 97.00. The euro has been confined to a little more than a quarter of a cent. Players seem reluctant to sell it below $1.14 and note there is a 570 mln euro option at $1.1420 that expires today. Sterling is straddling the $1.29 level, and intraday technicals warn of the risk of a retest of yesterday’s low near $1.2865. The dollar initially fell in Asia to test JPY111.80 but recovered in late-Asia and early Europe to test the JPY112.40 area. There are $1.3 bln in options struck between JPY112.50 and JPY112.55 that are expiring today. There is another roughly $1.3 bln in options struck between JPY112.00-and JPY112.10 that will also be cut today. The Australian and Canadian dollars are trading within the ranges seen yesterday. The Aussie may not make it back to $0.7100 where an A$605 mln expiring option is struck. The US dollar pushed above MXN19.50 yesterday. It is paring those gains in thin activity now, but a soft August retail sales report later today could renew the pressure. |

FX Performance, October 25 - Click to enlarge |

Overview: The dramatic sell-off in equities center stage after the S&P 500 lost 3% and the NASDAQ shed 4% yesterday. Stocks in Asia-Pacific followed suit, with the Nikkei’s 3.75% drop setting the pace. Of note, the Shanghai Composite was essentially flat. European bourses are struggling to hold on to some early gains, especially in Germany where the IFO survey showed a deterioration of investor confidence. Bond markets are firm with yields in Asian playing catch-up to the drop in the US yesterday. European peripheral yields are mostly slightly lower, but Italy’s 10-year benchmark is off six basis points (to 3.55%), while Italian bank shares are snapping a six-day slide. The dollar is softer against most of the major currencies, though the Japanese yen and Swiss franc are laggards, alongside the New Zealand dollar, which has been pressured a bit by the larger than expected trade shortfall (though both exports and imports rose). The dollar is mixed among the emerging market currencies. European currencies, including the Turkish lira, are faring better than East Asia. The South Korean won is the weakest following a disappointing Q3 GDP report that saw investment drop for the second consecutive quarter. Foreign investors continue to liquidate Korean shares. There has only been one session this month (October 12) that foreign investors bought Korean shares. At pixel time, the S&P 500 is called around 1.0% higher as it tries to snap a six-day drop. It has only advanced four sessions this month, coming into today.

ECB: Imagine the news summary ECB received as the two-day meeting began yesterday. The day before, the Bundesbank warned that the German locomotive may have stalled in Q3. The flash composite PMI for October fell to its lowest level since September 2016 (52.7 vs. 52.6), which is a three-old time series. The erosion of the German PMI was echoed in the deterioration on investor confidence and expectations in today’s IFO report. Europe’s largest bank reported disappointing earnings and the share price fell to record lows. Italy and the EC have begun a macabre slow dance, while the impatient markets are pushing Italian yields higher, spread wider, and bank shares lower.

No wonder the Financial Times calls for the ECB to reconsider ending its easy monetary policy at year’s end. It is not going to happen and for good reason. Don’t be surprised when some journalist asks, Draghi reveals that there wasn’t even such a discussion. First, the extraordinary monetary policy is simply buying assets. There are several other elements, including, for example, negative interest rates, fixed-rate fully allocated repos, liberal collateral rules. These are still going to be in place at the start of next year, with no clear, explicit exit plan except to commit to not raising interest rates until after next summer. Second, the asset purchases were running into technical constraints, which can be overcome, but the price would be steep. Third, it is not clear that the asset purchases are effective, even among many who defended the effectiveness at an earlier stage.

For the last five years, the eurozone economy expanded by an average of 0.5% a quarter. The ECB did not tighten policy when the economy grew 0.7% a quarter in 2017. A quarter or two of growth in the 0.2-0.3% range, which may be seen in H2 after 0.4% growth a quarter in H1. When it comes to it, there will be other policy levers that the ECB can pull. The bar against continuing asset purchases is high. The euro has fallen on the days the ECB has met this year, except last month.

Norway’s central bank met today, and as widely expected, policy was unchanged with the deposit rate left at 75 bp. Still, the central bank has begun a very gradual normalization process, and the next move will likely be in Q1 19. The next monetary report that is due mid-December (December 13) will likely further prepare investors. Sweden’s Riksbank met earlier this week and kept open the possibility of a December or February 2019 move and the ECB not raising rates until next September at the earliest, the Norges Bank need not be in any hurry. The euro has risen from NOK9.40 last week, which is a three-month low to almost NOK9.53 earlier this week and tried it again today before turning down.

Bank of Canada: The Bank of Canada raised rates as widely expected and its statement drove home the point that additional rate hikes will be forthcoming. The market took the bait and ran the Canadian dollar higher initially, but crashing equities and Governor Poloz’s effort to play down the decision to drop the word gradual to characterize the pace of future rate hikes. The central bank gave a clear signal to investors that the overnight rate was going to be hiked to the neutral level. However, unlike the US, the neutrality is defined as a range, and that range is wide enough to drive a truck through, 2.5%-3.5%. It is reasonable to expect the Bank of Canada to lift the overnight rate to the bottom of the range. That implies three quarter-point moves next year. It seems the risk is more likely in the direction of two hikes than four.

US: Judging from the media, people are still trying to get their heads around what seems to be a foiled terrorist attack on Obamas, Clintons, Soros, Holder, Brennan, Waters, and CNN. The response is underwhelming and some in the media are claiming it was a hoax. Imagine such an attack on nearly any other country and the kind of response it would have generated. Today’s US data will be overshadowed by the Draghi’s press conference. Yet, for the record, the highlights include trade and inventory data, which are not completely separate. It appears US companies ordered more goods ahead of the new round of tariffs. That means the risk is for a larger rather than a smaller deficit, but some of those extra imports likely boosted inventories. The US also reports September durable goods orders. After the 4.4% surge in August, some setback is likely. However, while the headline was strong, the details were poor, and now the opposite. Weakness in the headline may be offset by stronger core orders and shipments (excluding defense and aircraft). These reports are the last pieces of data for economists to fine-tune their forecasts for tomorrow’s first look at Q3 GDP. (median forecasts are for around 3 1/4% growth).

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$CAD,$EUR,$JPY,ECB,Featured,MXN,newsletter,SPX