I have been writing for many years that they really don’t know what they are doing. I only wish it was that simple. There has been developing another layer or dimension to that condition, a second derivative of stupid, whereby when faced with this now well-established fact the same people, experts and authorities all, they have no frame of reference to figure out what next to do. In other words, they really don’t know what to do when they realize they really don’t know what they are doing. Just over a week ago, former Fed Chairman Ben Bernanke wrote another blog post for economicsblog.com as a “leader” opining on his own previous thoughts about Japan’s pre-crisis QE experiments. He really should stop posting

Topics:

Jeffrey P. Snider considers the following as important: Ben Bernanke, currencies, depression, economy, Featured, Federal Reserve/Monetary Policy, inflation, Markets, newsletter, The United States, they really don't know what they are doing, unemployment rate, wages

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| I have been writing for many years that they really don’t know what they are doing. I only wish it was that simple. There has been developing another layer or dimension to that condition, a second derivative of stupid, whereby when faced with this now well-established fact the same people, experts and authorities all, they have no frame of reference to figure out what next to do. In other words, they really don’t know what to do when they realize they really don’t know what they are doing.

Just over a week ago, former Fed Chairman Ben Bernanke wrote another blog post for economicsblog.com as a “leader” opining on his own previous thoughts about Japan’s pre-crisis QE experiments. He really should stop posting altogether, but like Greenspan it seems pretty obvious that Mr. Bernanke can sense his legacy in jeopardy. And why shouldn’t he be keenly aware? He said one thing, starting with something about subprime and continuing all the way through the fourth QE, the world turned out instead wholly different. In picking on Japan, he must also be aware that his and the rest of the FOMC’s assessment of the Japanese situation has not aged well. There is an enormous volume of literature from the 2000’s that “diagnosed” what went wrong with the Bank of Japan that instead provided a template for what the FOMC or ECB would do anyway. Thus, at the end of last month he wrote:

|

Average Weekly Earnings Production And Nonsupervisory, January 1990 - May 2017 - Click to enlarge |

| As he so often does, Bernanke tries to obscure his glaring mistake by trying to claim “the results have generally been positive.” That point is hugely debatable to begin with, but also wholly beside the point. The Bank of Japan never once set out, nor did the FOMC, to generate generally positive results. They meant specific business about inflation and had, they thought, developed the specific formulas by which to achieve it. What was quantitative easing if not that?A more reasonable and objective assessment in 2017 would be that the Bank of Japan had no idea how to “vanquish” deflation and neither does Bernanke. QQE definitively showed, as the former Chairman backs his way into, that “resolve”, meaning getting truly crazy with any of the “Q’s”, has no effect. It would be fair to conclude inflation, though it must be a monetary phenomenon, escapes both he and they; further demonstrating that when it comes to money and therefore economy they really don’t know what they are doing.

It may come as a surprise to the public, but it isn’t actually one for economists and policymakers. The whole idea behind Positive Economics in the form of econometrics was that they didn’t need to know. All that was necessary, by this belief, was to figure out correlations. It is why, and how, economists became nothing more than statisticians, steeped in mathematics without the foggiest idea what goes on in an economy.

|

Accounting For All Labor, December 2016 - Click to enlarge |

| We can observe this time and again especially in the last decade and especially over the past three or four years. The unemployment rate was today estimated for May2017 to have been 4.3%. There isn’t on the surface any possibility that unemployment could be so low and labor market “slack” so stout. Everything at 4.3% points to concurrent, not imminent, not future, wage acceleration. Without a braking action, the US economy should be at the point where all Japan’s QE’s (at least 12 to this point) wish Japan’s economy would be. Yet, in both cases wage growth remains steadfast in its elusiveness. Average weekly earnings for production and non-supervisory employees were just 1% more last month than in May 2016. For all workers, average weekly earnings grew by just 0.9%. Variation is quite common in these data points, so averages are more instructive as to the state of wage inflation. The six-month average for production workers is just 2.4%, the same as it was last month and the month before. Thirteen months ago, the average was 1.8%, so clearly there is some improvement, but in terms that matter not really. |

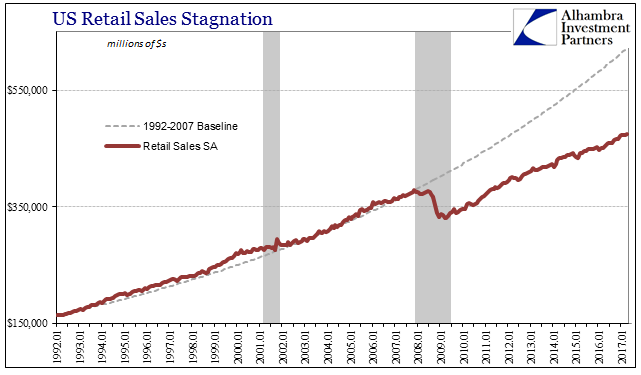

U.S. Retail Sales Stagnation, January 1992 - May 2017 - Click to enlarge |

| To begin 2015, average growth in earnings was 2.4%. At the end of the Polar Vortex in early 2014, average earnings growth was 2.4%. I could go on but you get the point. Policymakers have been seeing “signs” of acceleration all throughout that nearly three and a half year period. They could not be more encouraged by every drop of the unemployment rate; at least until now, as I wrote earlier. As the unemployment rate falls further especially in months like this where it is due to the labor force contracting sharply, their whole operating theory about economy falls apart.

How about now with 4.3% “unemployment” and not even the hint of signs of wage inflation? The lower the rate goes without inflation the more exposed their ignorance, and yet the more they harden and cling to their already untenable philosophy. They really don’t know what to do now that they suspect others have started to realize they really don’t know what they are doing. |

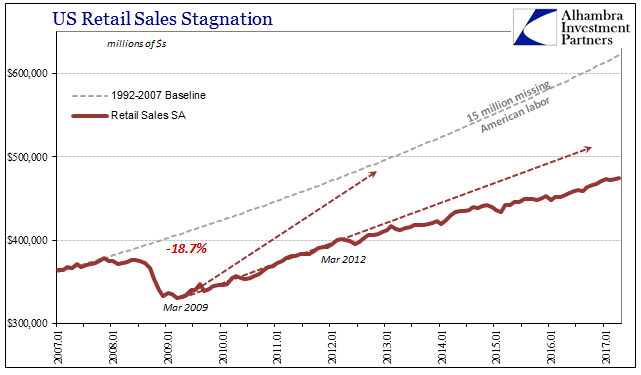

U.S. Retail Sales Stagnation, January 2007 - May 2017 - Click to enlarge |

|

How about now with 4.3% “unemployment” and not even the hint of signs of wage inflation? The lower the rate goes without inflation the more exposed their ignorance, and yet the more they harden and cling to their already untenable philosophy. They really don’t know what to do now that they suspect others have started to realize they really don’t know what they are doing. |

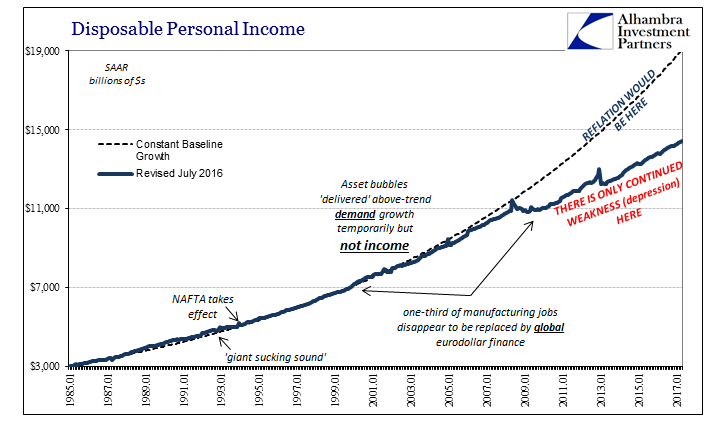

Disposable Personal Income, January 1985 - May 2017 - Click to enlarge |

Tags: Ben Bernanke,currencies,depression,economy,Featured,Federal Reserve/Monetary Policy,inflation,Markets,newsletter,they really don't know what they are doing,unemployment rate,wages