Swiss Economicblogs.org

Swiss Economicblogs.org

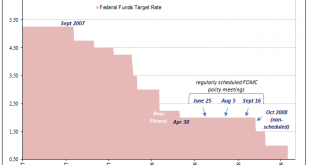

So Ben Bernanke has won a Nobel Prize for kicking a can down the road! Many will have heard the saying ‘those who do not learn from history, are doomed to repeat it’. It is often attributed to Churchill, but he was in fact quoting George Santanya. We prefer the Stephen Hawking quote, ‘“We spend a great deal of time studying history, which, let’s face it, is mostly the history of stupidity.” as this feels more apt in this day and age. Below we outline the Nobel-prize...

Read More »Ben Bernanke Wins Nobel Prize for Kicking Can Down the Road!