Summary: FOMC, BoE, and BOJ meet next week; only the Fed is expected to change policy. High frequency data may be less important than the central bank meetings and politics in the week ahead. UK political situation is far from resolved, and US drama continues, while several hot spots in the EMU are emerging. Three of the four G5 central banks meet in the week ahead: the Federal Reserve, the Bank of England and the Bank of Japan. Only the Fed is expected to change policy, and investors are as sure that a 25 bp hike will be delivered as they can be. This need not be a question of whether monetary policy is market-dependent or data-dependent. The confusion may lay with the popular claim that the Fed has a dual

Topics:

Marc Chandler considers the following as important: AUD, EUR, Featured, FX Trends, GBP, JPY, newsletter, SEK, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Summary:

FOMC, BoE, and BOJ meet next week; only the Fed is expected to change policy.

High frequency data may be less important than the central bank meetings and politics in the week ahead.

UK political situation is far from resolved, and US drama continues, while several hot spots in the EMU are emerging.

Three of the four G5 central banks meet in the week ahead: the Federal Reserve, the Bank of England and the Bank of Japan. Only the Fed is expected to change policy, and investors are as sure that a 25 bp hike will be delivered as they can be.

This need not be a question of whether monetary policy is market-dependent or data-dependent. The confusion may lay with the popular claim that the Fed has a dual mandate. In truth, it has three. In addition to full-employment and price stability, is financial stability. The tightening of financial conditions in Q3 15 deterred the Fed from hiking in September, as it had encouraged investors to anticipate (and strategists:-( ).

A preliminary proposal was for a very small start (understood to be a few billion dollars) and gradually (quarterly) increasing. There seemed to be an inclination to include both Treasuries and MBS in the process. There was little indication of the end game or desired size of the Fed’s balance sheet, but it seems to be understood that it will have to be bigger than status quo ante.

Given that monetary policy is still open-throttle easing, then it follows that officials would prefer the movement of the currency not run in the opposite direction. Our general impression remains that Japanese businesses and officials are content with JPY110-JPY120. However, barring a change in rhetoric or practices, the near-term direction seems broadly driven by the change in US yields.

Political developments compete with economic developments for investors’ attention. UK Prime Minister May’s top two advisers resigned, but there does not appear to change in key cabinet positions. May is trying to hold on, but reports suggest the pressure to resign is mounting. It is difficult to envision her last for long. In terms of Brexit, EU President Tusk noted that the end date of negotiations is fixed, the start date is not. The controversial positions of the DUP, upon the government will rely on to support the minority government, in some ways makes the Tories appear even more desperate and weak rather than strong and stable. Rates will likely remain lower for longer, and sterling may be a bit weaker than it otherwise would have been. The UK appears to have entered a more fluid political situation just as the negotiations were to begin. Its position seems to have been compromised. There still seems to be little scope for a soft Brexit if by that is mean a dilution of the EU’s demand that the four freedoms must be respected.

At the same time, the risk is hubris among the celebratory Labour. It is not clear how much was due to Corbyn’s newly discovered charisma and how much was a vote against something (what that something seems to be a bit of a Rorschach Test presently). Moreover, a moral victory may sound nice, but Labour still lost, and it follows a drubbing in the local elections last month. Even if another election is forced, as many now think will be the case, perhaps later this year, a Labour government still does not seem a likely scenario.

The first round of the French parliamentary election is likely to show the hope and enthusiasm for Macron and his new party that may incite a realignment of French politics. It is a bit too stylistic to push the point far, but it is as if Macron is taking part of the pro-business right-wing of the Socialists and combining them with centrists and moderates among conservatives (the Republicans and others) to forge this new political movement. In addition to a strong pro-European stance, Macron has indicated that labor market reforms will be his first big push.

Separately, we note the large Italian banks are considering injecting capital into the two troubled regional banks so to allow a precautionary recapitalization. This would avoid equity investors and subordinated creditors from realizing losses. Reports suggest that a junior credit of one of the troubled banks matures on June 21, so a decision would seem to have to be made before then.

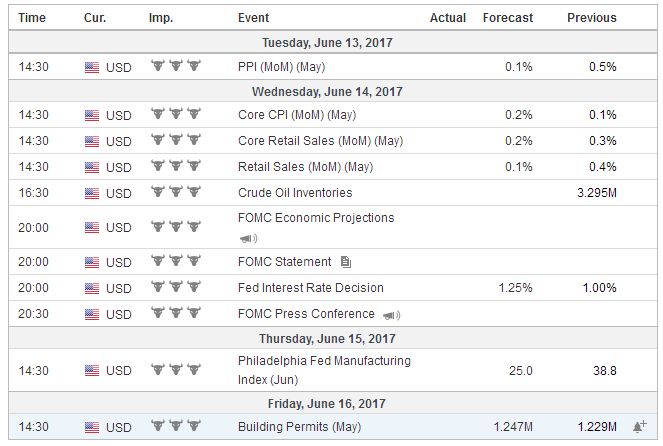

United StatesOur calculations, based on assumptions where Fed funds will effectively trade (weighted average) for the second half of the month and where it may trade on the last day of the month (quarter end), suggested that fair value on a 25 bp hike would have the June contract imply a yield of 1.04%. Before the weekend it closed at 1.0325%. Bloomberg, which recently changed its methodology, suggests the market has discounted a 97.8% chance of a hike, while the CME is even higher at 99.6%. Ironically, the third hike since the US election last November is so greatly assumed, that it is not the most important element of the FOMC meeting, though if it is not delivered, that would indeed overshadow everything else. The simple, even if unpleasant, truth is that the economy’s rebound from the typical Q1 weakness is disappointing, and more, to the point, the preferred core PCE deflator has drifted lower for three consecutive months. The Atlanta Fed’s GDP tracker for Q2 has fallen from a little more than 4.0% to 3.0%. It has converged with the median in Bloomberg’s survey, but the risk is that it is too high still. Our own thinking is more in line with the NY Fed’s tracker that puts it at 2.25%. The NY Fed’s model is not optimistic about Q3, for which it puts GDP at 1.8%. The most important part of the outcome of the FOMC meeting is what it reveals about how officials see these challenges. The market is not convinced that there will be another rate hike this year (Bloomberg and CME calculations show about a 42% chance that Fed funds target will be at 1.25%-1.50% before the end of the year). Some officials, like Governor Brainard, have already expressed some concerns. Are those shared? What about the reduced expectations for fiscal support this year? The economic projections (dot plot) may take on heightened significance. There has been much discussion that financial conditions eased in the face of the Fed’s gradual effort to remove accommodation. There are several different measures, but they agree that financial conditions, which take into account various interest rates, equity prices and exchange rates, are at two or three-year lows. This is a powerful argument in favor of additional Fed efforts. It judges that level of monetary accommodation that the economy needs. It judges it needs less, but for various, and admittedly not always well understood, complex factors, conditions are more accommodative. Investors also will focus on indications about the coming new balance sheet regime, where the Fed will not simply roll over all maturing issues. In effect, it will unwind the swap that has been dubbed QE. The Fed swapped reserves for Treasury bonds and mortgage-backed securities. Officials want to make the process as least disruptive as possible. Lastly, US political drama will not go away. It is still, however, too early to tell the extent of the distraction on the legislative process that is taking place. Committee work continues. The Financial Choice Act that seeks to replace and repeal the national financial regulatory framework (Dodd-Frank) passed the House of Representatives last week. However, its fate is similar but different than the attempt to replace and repeal the Affordable Care Act (Obamacare). The House version will not pass the Senate, and the Senate leaders have indicated they have other priorities. Many are closely following the tight congressional race in Georgia to fill the seat vacated by the new Secretary of Housing and Human Services. It has become the most expensive congressional election in history, and between the first round (April 18) and the second round (June 20), the UK called and held a national election. In any event, both parties see it as an important harbinger for the midterm elections in 2018. |

Economic Events: United States, Week June 12 - Click to enlarge |

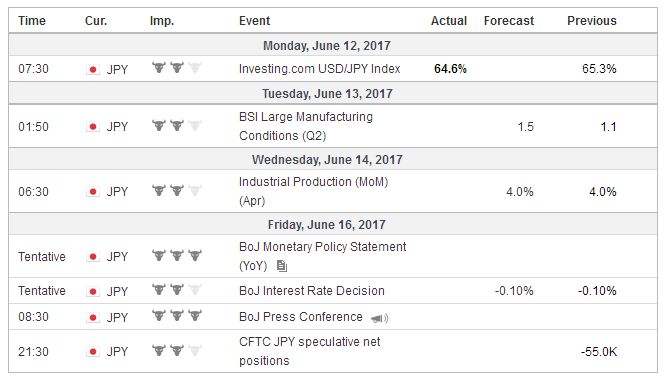

JapanThe Bank of Japan meets. There seems to be an increase of interesting in the Diet and media about the exit strategy. The message from the Bank of Japan is patience. It is too early to have a meaningful discussion. Although some measures deflation has abated, the Q1 GDP deflator, which some economists argue is a more accurate measure of prices, was minus 0.8%. The fact that the central bank’s balance sheet is growing by less than the JPY80 trillion target ought not be confused with tapering. It is a modification to QQE. The shift to targeting the 10-year yield necessitated buying fewer government bonds. Ideas that the BOJ would revise up its growth forecasts were dashed last week when the estimate for Q1 GDP was halved to 0.3%. Nevertheless, the stronger foreign impulses and the increasing investment may be bolstering the official confidence of that economic growth is solid a little above trend, and the output gap gradually is being closed. |

Economic Events: Japan, Week June 12 - Click to enlarge |

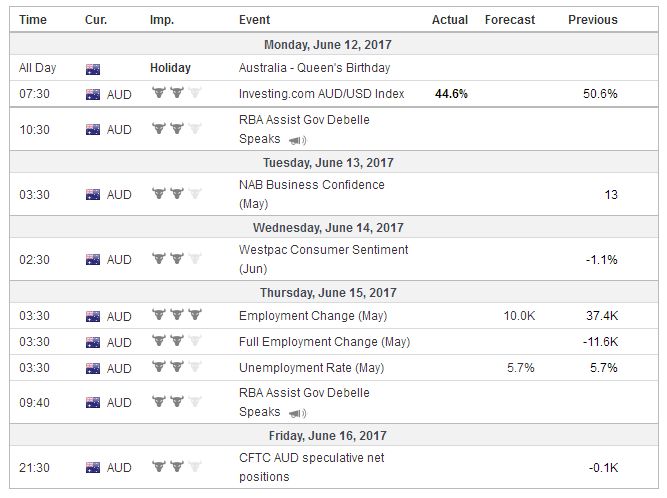

| Australia reports June inflation expectations. It has been between 4.0% and 4.3% since the start of the year. Even though in May was at the lower end of the range, we see downside risks. It finished last year at 3.4%. Australia also reports May employment data. It is likely to return toward earth from its recent stellar performance, creating 60k jobs in March and 37.4k positions in April. Last year’s average was a little less than 9k a month. The 2015 and 2016 average was almost 17k. |

Economic Events: Australia, Week June 12 - Click to enlarge |

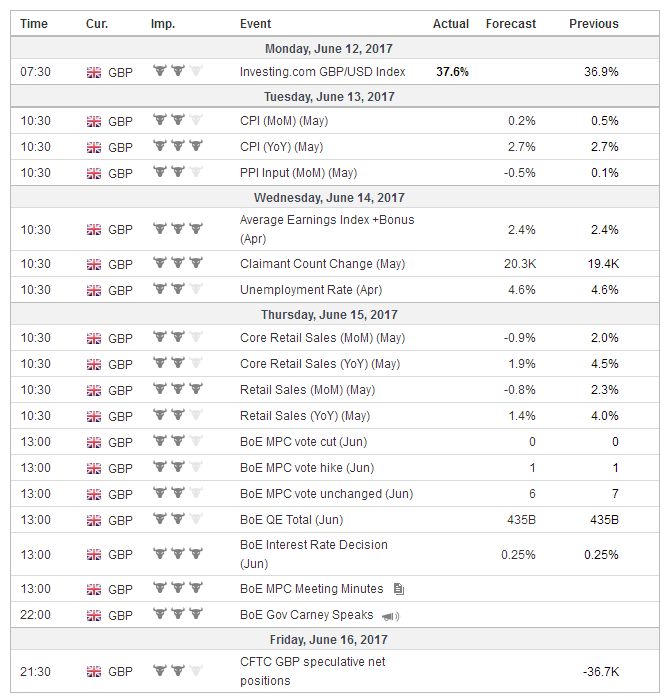

United KingdomThe Bank of England’s Monetary Policy Committee meets. No one expects a change in rates. Forbes, recently the lone dissent for an immediate rate hike will likely persist, but it is her last meeting. The MPC is also short a Deputy Governor, making a 7-1 vote is the most likely scenario. The electoral outcome may not be a direct economic factor or featured in the minutes. Sterling’s decline is not material. It appreciated by nearly 1.6% against the dollar so far in Q2 and was up about the same in Q1. The euro-sterling exchange rate has been in broad trading ranges since the second half of last November, roughly GBP0.8300-GBP0.8850. It was at GBP0.8340 at the end of June 2016. Sterling’s decline was not capital flight in the face of political uncertainty. British bonds and stocks rallied. Both the two and 10-year government yields eased 2.5 bp. The FTSE 100 rallied (~1.0%) ostensibly aided by a weaker sterling, but the more domestic FTSE 350 advanced nearly as much (~0.9%). The UK reports on inflation, employment, and retail sales. Simply put, CPI and labor conditions are expected to have been little changed, and retail sales will most likely weaken. The preferred CPIH expected to have risen 2.6% over the past year, the same pace as in April. It finished last year near 1.8%. The core rate may have eased to 2.3% from 2.4%. Employment growth is expected to be steady in May, and average weekly earnings are expected to have been steady in April, 2.4% above a year ago level (3m/3m). The ILO measure of unemployment is expected to be steady at 0.6%, but the claimant count spiked higher and remains elevated. Retail sales jump 2.0% in April, partly due to the calendar effect of Easter. Half or more of the rise will likely be unwound. |

Economic Events: United Kingdom, Week June 12 - Click to enlarge |

EurozoneThese central bank meetings and last week’s ECB meeting may render the market somewhat less sensitive to this week’s high frequency data. The high frequency data is expected to confirm the general macro situation. Of note, the US reports CPI (core likely stable at 1.9%), retail sales (soft headline and steady but inspired 0.2% increase in the GDP components), and industrial output (consensus expects a small gain, but the risk is for small declines especially after the outsized 1.0% increase in industrial output and manufacturing in April). In Europe, the eurozone reports April industrial production. It fell in February and March, but it is expected to have improved, rising 0.5%. It will reaffirm the sense the eurozone economy is growing at a steady pace. In Sweden, price pressures are expected to ease in April after a squeeze higher earlier. Meanwhile, the Eurogroup meeting will approve the tranche payment so Greece can make a seven bln debt servicing payment to it official creditors next month. However, the meeting promises to be dramatic. Unless the finance minister is prepared to reduce Greece’s debt burden in a meaningful and substantial way, the IMF will participate as an adviser and not provide funds. More importantly, it means that Greece still will not be able to return to the markets, and that, as we have warned, makes a fourth assistance package likely. At the same time, given the thrust of the US Administration, it is possible that it would block the IMF participating in a new package in any event. There is the talk of converting the ESM into a European IMF, with how the power is allocated to the institution an important distinction. Out of France and Germany, where Merkel is in a strong position to be re-elected, the political climate in Europe has a few areas of concern. Catalonia has indicated it will hold a referendum on independence on October 1. This will be a protracted conflict with Madrid, which has not given its approval. In Italy, the great political compromise of adopting a German-like electoral system appeared to collapse last week after a deputy from the Five-Star Movement submitted an amendment. The prospect of fall elections had weighed on Italian bonds, and the collapse of the compromise saw the Italian bonds rally. |

Economic Events: Eurozone, Week June 12 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week June 12 - Click to enlarge |

Tags: #GBP,#USD,$AUD,$EUR,$JPY,Featured,newsletter,SEK