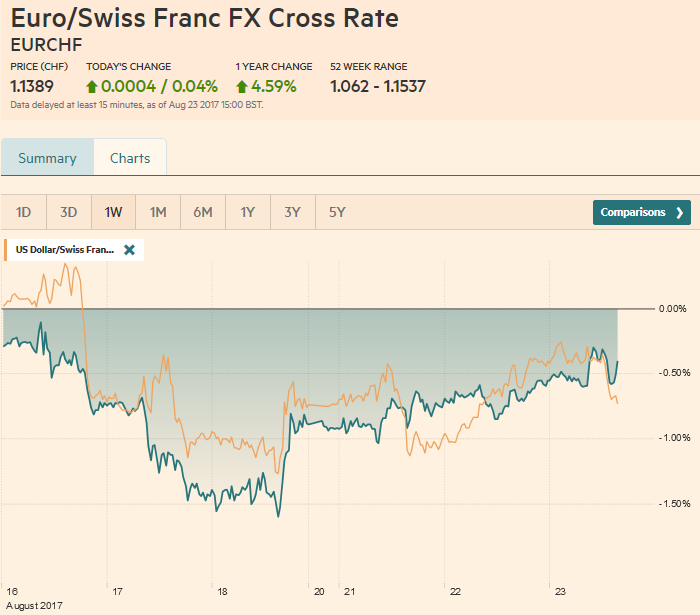

Swiss Franc The Euro has risen by 0.04% to 1.1389 CHF. EUR/CHF and USD/CHF, August 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates A mixed US dollar will greet the North American participants today. It is softer against the euro and yen, but firmer against the dollar-bloc currencies. Among the emerging market currencies, the eastern and central European currencies are moving higher in the euro’s draft. The US recognition that North Korea has not escalated the war of words even though it just announced new sanctions on 10 Russian and Chinese companies and half dozen individuals were aiding it; the Korean won posted its third consecutive advancing sessions. Asian

Topics:

Marc Chandler considers the following as important: AUD, CAD, EUR, EUR/CHF, Eurozone Manufacturing PMI, Eurozone Markit Composite PMI, Eurozone Services PMI, Featured, France Manufacturing PMI, France Services PMI, FX Trends, GBP, Germany Manufacturing PMI, Germany Services PMI, Japan Manufacturing PMI, JPY, newslettersent, U.S. Manufacturing PMI, U.S. Services PMI, USD

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Swiss FrancThe Euro has risen by 0.04% to 1.1389 CHF. |

EUR/CHF and USD/CHF, August 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

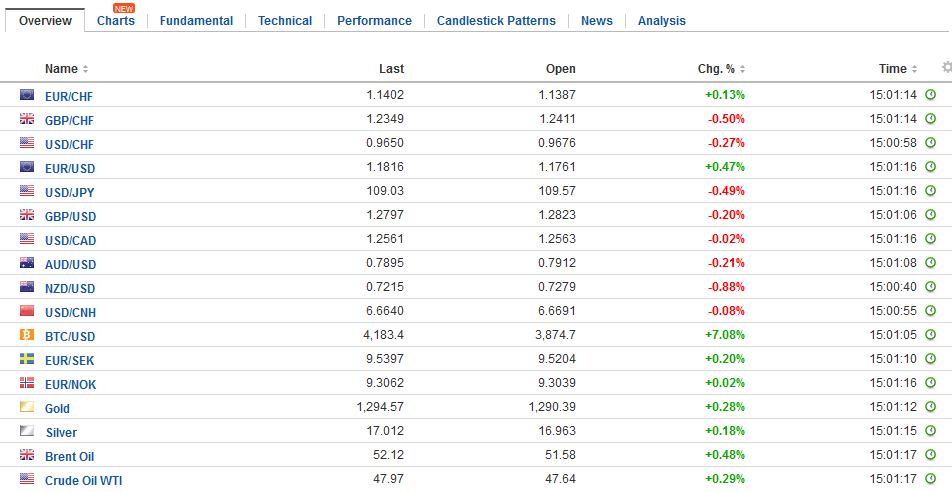

FX RatesA mixed US dollar will greet the North American participants today. It is softer against the euro and yen, but firmer against the dollar-bloc currencies. Among the emerging market currencies, the eastern and central European currencies are moving higher in the euro’s draft. The US recognition that North Korea has not escalated the war of words even though it just announced new sanctions on 10 Russian and Chinese companies and half dozen individuals were aiding it; the Korean won posted its third consecutive advancing sessions. Asian equities advanced with the MSCI Asia Pacific Index also posting small gains for each day this week and seven of the past eight days. Some of the markets that are open late struggled and European equities are mostly lower. The Dow Jones Stoxx 600 is off 0.2%. Financials and materials are bucking the drag from the other sectors, led by consumer discretionary and utility sectors. It is the fourth losing session in the past five. Sovereign 10-year benchmark yields are mostly firmer, with Italy and Portugal seeing yields rise five-six basis points. Although a key controversial adviser to President Trump was dismissed last week, the opportunity to re-start may be closing. Last night, Trump made two unsettling remarks. First, he suggested that he may be willing to accept a shut down of the government if that is what is necessary to get Congress to authorize funding for the controversial wall on the border with Mexico. The spending authorization is needed by the end of September as the US begins a new fiscal year. Government shutdowns are not unprecedented in the US, of course, and they typically are mildly disruptive. They are not good for the investment climate. |

FX Daily Rates, August 23 - Click to enlarge |

| Congress may seek to link the spending authorization bills with the debt ceiling. The failure to renew the spending authorization leads to a government shutdown, but failure to lift the debt ceiling impairs the ability to service the debt. While political maneuvering can lead to a shutdown, missing a debt payment is considerably more serious and one that in this game of brinkmanship largely within the Republican Party neither side seems to want to risk.

Secondly, Trump also threatened that he may still bring the US out of NAFTA. The re-opening of negotiations just began last week. There were much optimism and favorable spin in most of the media. Although reports suggest that, contrary to the normal course where easy issues are resolved first, controversial issues were discussed. Yes, they were discussed, but it seemed to turn into a simple restatement of each main issues. Domestic content and the conflict resolution mechanism seems to be on what the negotiations will ultimately turn. Between the new efforts to get funding for the wall and the threat to pull out of NAFTA, it is little wonder that the Mexican peso is the weakest of the emerging market currencies today (-0.7%) and rivaling the New Zealand dollar (-0.8%) as the weakest currency in the world today. |

FX Performance, August 23 - Click to enlarge |

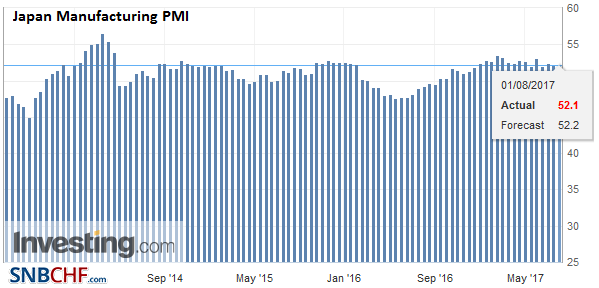

JapanJapan and EMU have reported preliminary PMI readings for August. Japan’s manufacturing PMI rose to 52.8 from 52.1 in July. Last year it averaged 50.0. This year’s average is 52.7. It is also the average for Q2. Similar to many other high income countries, the pressing challenge for Japan is not growth but prices. Before the weekend Japan reports July CPI. The core rate (excluding fresh food) stood at 0.4% in June and may have ticked up to 0.5% in July. |

Japan Manufacturing PMI, Aug 2017(see more posts on Japan Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

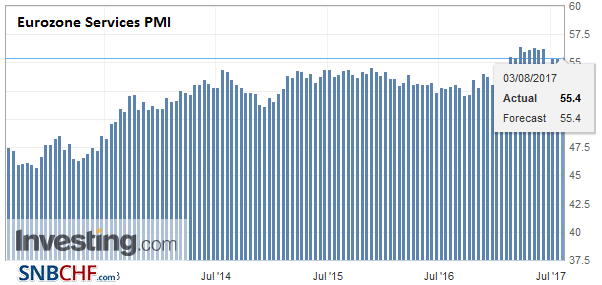

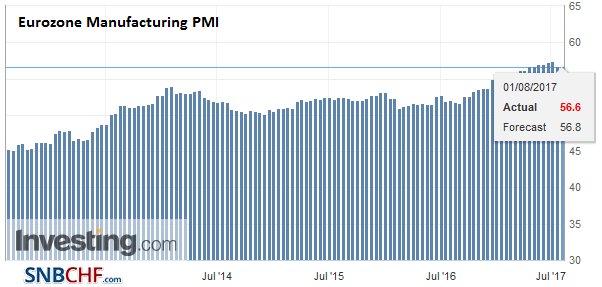

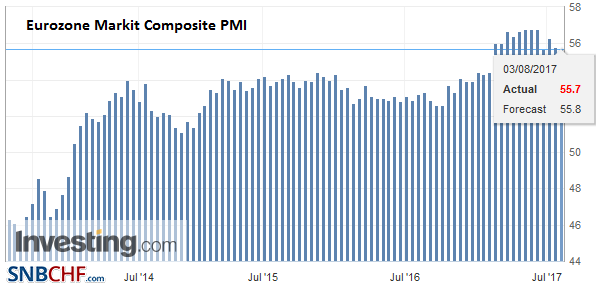

EurozoneIn Europe, the weakness in services was offset by the strength of manufacturing, leaving the composite virtually unchanged at 55.8 (vs. 55.7). The manufacturing reading rose to 57.4 from 56.6. This matches the cyclical high seen in June. The service reading, which covers a larger part of the economy slipped to 54.9 from 55.4. The index peaked in April at 56.4. |

Eurozone Services PMI, Aug 2017(see more posts on Eurozone Services PMI, ) Source: Investing.com - Click to enlarge |

| There are three takeaways from the EMU PMI. First, the economy continues to operate at a strong level, but the momentum has moderated. Second, price components suggest that the pullback in inflation since February may be coming to an end. Third, the euro’s appreciation has so far not undermined export orders, where the sub-index rose to its best level in six years. |

Eurozone Manufacturing PMI, Aug 2017 (flash)(see more posts on Eurozone Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

| This, in turn, may have some bearing on how to understand the level of concern among the ECB regarding the euro’s strength. We think the concern is still very mild. It also may impact the bias going into Jackson Hole. In his speech earlier today, Draghi defended the effectiveness of its asset purchase program. |

Eurozone Markit Composite PMI, Aug 2017 (flash)(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

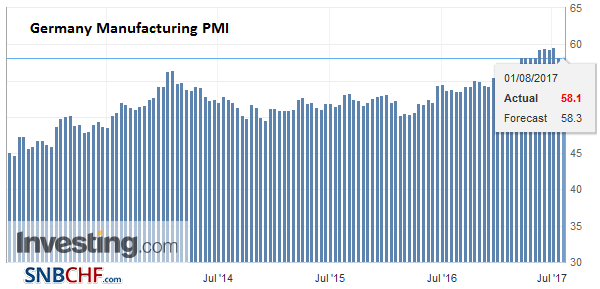

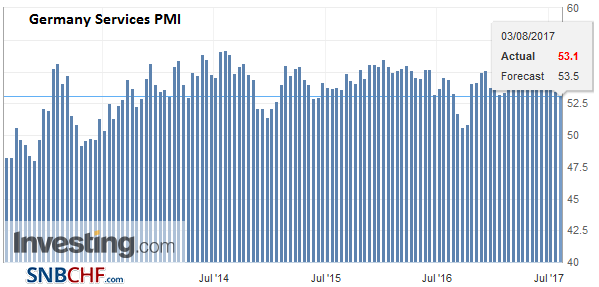

Germany |

Germany Manufacturing PMI, Aug 2017 (flash)(see more posts on Germany Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Germany Services PMI, Aug 2017 (flash)(see more posts on Germany Services PMI, ) Source: Investing.com - Click to enlarge |

|

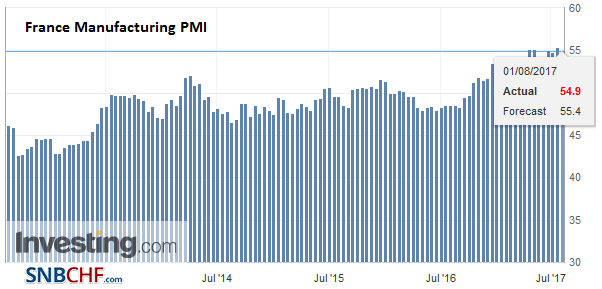

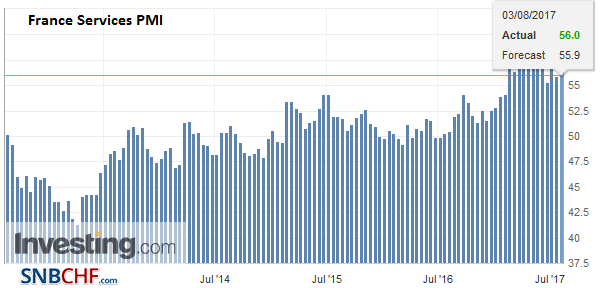

France |

France Manufacturing PMI, Aug 2017 (flash)(see more posts on France Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

France Services PMI, Aug 2017 (flash)(see more posts on France Services PMI, ) Source: Investing.com - Click to enlarge |

|

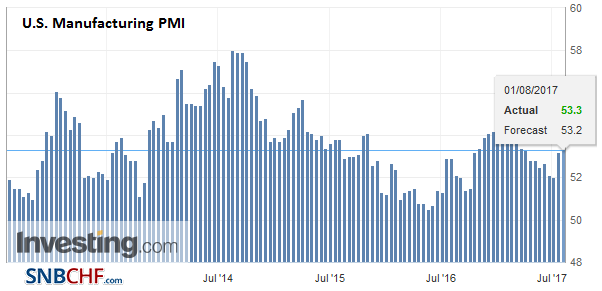

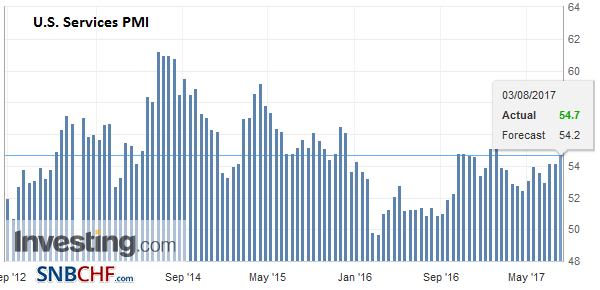

United StatesIn the US Markit reports its flash US PMIs and new home sales for July will be released. Barring significant surprises, the data are unlikely to have much impact. Trading remains choppy within a consolidative phase. We expect the phase to end shortly. The S&P 50 gapped higher yesterday and closed strongly. It set to open about 0.2% lower, and before the gap (~2430.6-2433.7) is filled, the 2440 area may act as a swing level. |

U.S. Manufacturing PMI, Aug 2017 (flash)(see more posts on U.S. Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

U.S. Services PMI, Aug 2017 (flash)(see more posts on U.S. Services PMI, ) Source: Investing.com - Click to enlarge |

United Kingdom

The UK continues its release of position papers on the Brexit. Today’s was on the judiciary. Again the UK softens its initial position, but it does not appear that these papers have had much on the EU negotiators. The position papers are more addressed to the domestic audience rather than as a negotiating tool. There still seems to be a sense of bewilderment. The UK, for example, still does not accept the EU’s negotiating sequence: first the divorce and then the arranging new friendship with potential benefits.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,Eurozone Manufacturing PMI,Eurozone Markit Composite PMI,Eurozone Services PMI,Featured,France Manufacturing PMI,France Services PMI,Germany Manufacturing PMI,Germany Services PMI,Japan Manufacturing PMI,newslettersent,U.S. Manufacturing PMI,U.S. Services PMI