Team Asset Allocation and Macro Research

My articles My siteMy booksMy videos

Follow on:TwitterFacebook

Having laid down our expectations for the World economy in 2018, in this note we describe a number of potential surprises to the outlook. The usual suspects, or ‘known unknowns’, include a larger-than-expected fiscal boost from US tax cuts, (geo-)political risks, economic policy mistakes, inflation surprises, a financial bubble burst, or a Minsky moment in China, to name a few. We chose to include some of the out-of-the box surprises that have remained under the radar. By definition, none of them are include d in our baseline scenario. US 1. Rising oil prices fuel a ‘Texas boom’ The experience of recent years has shown that falling (rising) oil prices are in fact bad (good) news for the US economy owing to the

Topics:

Team Asset Allocation and Macro Research considers the following as important: 2018 outlook, Featured, global macro, Macroview, newsletter, Pictet Macro Analysis, Swiss and European Macro, World economy

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Having laid down our expectations for the World economy in 2018, in this note we describe a number of potential surprises to the outlook. The usual suspects, or ‘known unknowns’, include a larger-than-expected fiscal boost from US tax cuts, (geo-)political risks, economic policy mistakes, inflation surprises, a financial bubble burst, or a Minsky moment in China, to name a few. We chose to include some of the out-of-the box surprises that have remained under the radar. By definition, none of them are include d in our baseline scenario.

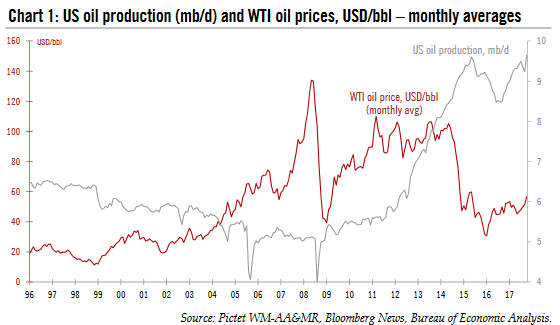

US1. Rising oil prices fuel a ‘Texas boom’The experience of recent years has shown that falling (rising) oil prices are in fact bad (good) news for the US economy owing to the ballooning US oil production on the back of the ongoing shale boom. From 2.9% in 2015, US GDP growth slowed to 1.5% in 2016, the same year WTI touched a low of USD 26.05 (on 11 February 2016). The pick-up in oil drilling, in the wake of the oil price rebound, has been a major driver of the US economy’s recent dynamism – and a key support of the recent uptick in investment. That being said, the oil futures curve is currently in backwardation (future prices are below spot prices), and commodity market participants seem to expect that oil prices will drift down from current levels in the coming months. Should oil prices start to price a more positive scenario – for instance, due to stronger global demand – US oil investment could see a major uptick, and Texas could accelerate, in turn lifting US growth. A quick regression of mining’s role in US GDP in recent years shows that a USD 10 increase in WTI oil prices boosts annual US GDP by 0.15 percentage point. A USD 20 rise in oil prices from current levels could therefore be potentially amplify the likely 2018 GDP boost from Congress’s tax cuts. That being said, we should still watch for the potential hit of higher oil prices to private consumption, which, while being more diffuse, still exist s, and could start to bite in 2019 2. More hawkish officials are nominated at the Fed BoardThe turnover at the Federal Reserve’s Board of governors has been particularly high lately , and there could be further changes to come. Fed Chair Janet Yellen will leave the Fed Board once Jerome Powell (a governor since 2012) has been sworn in as Chair in early 2018. Vice Chair Stanley Fischer left in October and there is no replacement so far. There are also changes at the regional Fed banks. In particular, the influential New York Fed president Dudley will leave next summer. Meanwhile, the Trump administration has named Randal Quarles as Vice Chair for banking supervision.

|

US Oil Production, 1996 - 2017 - Click to enlarge |

| That being said, our view is that the impact of this turnover on the Fed’s policy will be quite modest. Policy wise, we think Powell will be in the same vein as Yellen. We also feel that the Fed staff will be instrumental in influencing the Fed board towards a gradual normalisation.

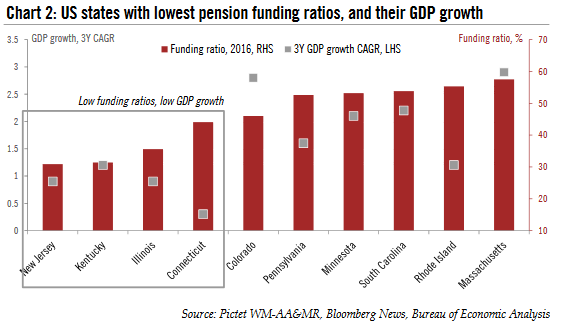

That being said, there remains some uncertainty with regard to the various vacant seats on the Fed Board, and the appointments could affect the Fed’s policy more than we expect. While Trump has preferred continuity in the Fed’s leadership with Powell, he could still put more hawkish officials on the Fed Board. In turn, the risk remains that the very benign normalisation being priced by money markets – which is well below the Fed’s planned trajectory via the median dots – could be called into question. This unexpected turn could in turn lead to much tighter financial conditions, a nd hit US growth. 3. Chicago defaults on its bonds, creating turmoil on the muni marketPuerto Rico’s debt woes amplified this year, particularly as the island was rocked by a severe hurricane , which further depleted its financial resources. But the ‘contagion’ to the wider US municipal bond market was inexistent. The question is whether this would change if an ‘onshore’ municipality were to default. While US growth remains favourable, many US cities and states are facing budget difficulties, particularly as pension costs continue to escalate. Illinois and the city of Chicago are particularly affected by the negative jaws of rising pension costs, slow activity and unfavourable demographics (population outflows in particular). Should the situation worsen in Chicago, the question is whether investors could have a second (and more pessimistic) look at the pension situation at many of these municipalities. The total volume of municipal debt outstanding amounted to USD 3.6 trillion in Q3 2017. A sharp tightening in market conditions for municipal debt could lead to a slowdown in infrastructure investment at the local level. |

US States with Lowest Pension Funding, 2016 - Click to enlarge |

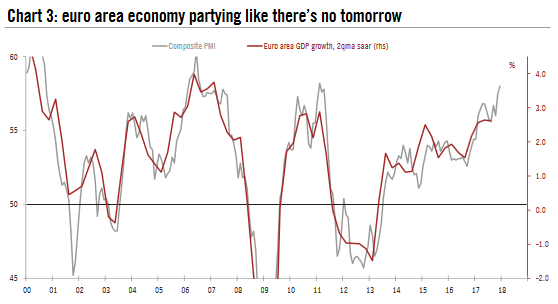

Europe4. The ECB hikes rates as ‘Euroboom’ morphs into ‘Eureflation’Our upbeat 2018 outlook for the euro area describes an economy reaching escape velocity in the form of a broad -based and self -sustained expansion. We forecast euro area real GDP growth of 2.3% in both 2017 and 2018. Yet risks remain tilted to the upside, most importantly in terms of credit-fuelled investment spending. A revival of animal spirits in those countries with the largest investment gap relative to pre-crisis trends could lift GDP growth above 3% on a sustained basis. True, the euro area only recorded similar growth rates when some sectors were in bubble territory, including 3.2% growth on average in 2006-07 (Spanish property boom), or 3.1% in 1997-2000 (dot-com bubble, before the euro was introduced). This time looks different, though. The prospect of macroeconomic stability and institutional progress (including in terms of a stronger EU and tighter monetary union) could lead to the unleashing of large pent-up demand, if only because of the slack accumulated through the crisis years catching up with rising aggregate demand. Moreover, robust global growth could help, at least at the margin, by boosting net trade as price competitiveness recovers. Although the ECB has committed not to raise interest rates until “well past” the end of its net asset purchases, forward guidance is not set in stone. In fact, prominent ECB officials, including Executive Board member Benoît Coeuré, have started to challenge the exit sequencing this year. Strong growth alongside early signs of a revival in inflation could prompt the ECB to re-think its exit path. It would certainly be no easy ride, but it looks feasible, and as a side-effect it would help reduce internal divisions with the hawks. If the communication shift is managed properly, the ECB could also engineer a steeper yield curve while keeping sovereign debt spreads in check, both supporting rising bank profits. The ECB would start with an adjustment of its forward guidance, allowing for greater flexibility in how each policy rate (the deposit facility rate, the main refinancing rate, and the marginal facility rate) can move relative to the others. This would be a pre-requisite for an early deposit rate hike, in our view, from the current -0.40% to a less negative level in 2018. Meanwhile, the ECB could keep the current exit sequencing intact when it comes to the main refinancing rate, currently at 0%, hinting at a first hike in 2019 only once asset purchases have been tapered in full |

Euro Area Economy, 2000 - 2017 - Click to enlarge |

5. Hélène Rey emerges as the next ECB President in-waiting

Several top EU jobs are due to be filled in the next couple of years, including the ECB’s Vice-President and President whose terms end in May 2018 and October 2019, respectively. Arguably, ECB President Mario Draghi’s successor is unlikely to be known before the beginning of 2019 at the earliest, but the ‘grand bargaining’ will start earlier, especially as Germany wants to secure some key positions (even though they have the presidency of the EIB and the ESM already).

In the event that no agreement can be reached on the ECB’s top job, for instance if France and other countries oppose Jens Weidmann’s candidacy, then an alternative would be to name an outsider, in the form of an economist well-known to the central banking world but currently working in academic circles. One of our favourite candidates would be Hélène Rey, Professor of Economics at the London Business School, and highly respected for her work on global financial flows and macroeconomic stability, among many other things. She happens to be a woman, which may help, but also French, and this could complicate her candidacy. One could think of many alternative candidates, including another French woman, current IMF Managing Director Christine Lagarde. The implications for markets would likely be positive overall as any non-German ECB President would be perceived as less hawkish, at least initially.

6. Jeremy Corbyn gets the keys to 10 Downing Street

Theresa May’s Conservative government may be weak and rudderless, but, with Jeremy Corbyn waiting in the wings, it will attempt to soldier on. However, Conservative hardline eurosceptics are even more focused on, for them, the biggest prize — a hard Brexit. As such, it is not hard to imagine a Tory implosion. As negotiations with Brussels on a new trading agreement flounder in the second half of 2018 and UK business panics, May looks ready to concede on a transition period of considerably more than two years, during which the UK would remain subject to Single Market rules. Brexiteers are apoplectic. Boris Johnson, backed by Michael Gove, mounts a leadership challenge against May. But “the hand that wields the knife shall never wear the crown,” and after May loses a confidence vote among Tory MPs, Johnson’s disloyalty is punished by elimination ahead of the final round, the membership ballot, in the ensuing leadership vote. The Conservatives’ pro-Brexit (and overwhelmingly elderly) support base plump for the straight-talking and hardcore Brexiteer Jacob Rees- Mogg over the modernising (but soft-on-Brexit) candidate, Amber Rudd.

Rees-Mogg has a problem though: parliament has been promised a vote on the Brexit deal, and he knows there isn’t a majority for hard Brexit. Buoyed by initially strong personal approval ratings, and a bounce for the Tories in opinion polls, he gambles on an election. However, Rees-Mogg’s throwback social views hamper him under the campaign spotlight, and the Tories are outfought in key marginals by Labour’s strong ground operation. In the hung parliament that results, an alliance with the Scottish Nationalists, the Liberal Democrats and the Greens gives Labour’s Jeremy Corbyn the keys to Downing Street, leading the most left-wing UK government since the 1970s. But is this 1974 (when a tired Conservative government temporarily ceded power to a weak and ineffective Labour administration before storming back five years later) or 1979 (when a period of political upheaval and economic weakness ended with the election of one of the most radically transformative governments in modern British history)? Only 2019 will tell.

7. SNB under pressure to ease further

Over the past few years, Swiss corporates have sought to offset the strength of the franc by adjusting their prices. Inflation returned to positive territory in 2017 for the first time in five years. The base effects of energy price fluctuations are likely to drive Swiss headline inflation lower in the near term, but we expect headline inflation to firm up as 2018 progresses.

Nevertheless, several other developments might dampen inflation more than we expect. First, as a result of the rejection of the “2020 pension reform” in a referendum in autumn 2017, VAT rates will be reduced to a standard rate of 7.7% (normal rate) and 3.7% (special rate for accommodation) as of 1 January 2018. The reduced rate of 2.5% will remain unchanged. The reduction of VAT rates will affect a range of consumer goods, putting some downward pressure on headline inflation. Second, rents (which account for 18% of the CPI index) are under pressure owing to the fall in the base rate, which will also impact inflation. In contrast, prices of imported goods are expected to rise because of the weaker franc.

If inflation surprises significantly on the downside, it may force the Swiss National Bank to maintain, if not to ease, its already a ccommodative monetary stance.

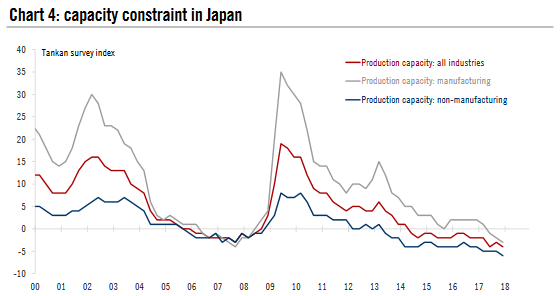

Asia8. Japanese inflation surprises to the upsideWhile growth in Japan is picking up on both the domestic and external fronts, inflation has been a major disappointment. Nearly five years after the Bank of Japan (BoJ) started its unprecedented monetary easing, core inflation still lies stubbornly below 1%, less than half the BoJ’s target. However, inflationary pressure is quietly building up in Japan as capacity constraints continue to tighten, especially in the labour market. The unemployment rate has dropped to 2.8%, the lowest since mid -1994. So far the tight labour market has not brought significant increases in average workers’ wages, but no one really knows how long this can last, as it is becoming increasingly difficult for businesses to hire additional workers, especially in the service sectors. If inflation were to surprise to the upside, it could force the BoJ to reconsider its monetary policies, especially when policy-makers are increasingly wary of the negative side effects of the ultra-loose monetary conditions. In this event, the BoJ may surprise the market by adjusting its yield curve control earlier than expected. For example, it could decide to raise its yield target earlier in 2018, or to re-anchor its long-end yield target from the 10 year Japanese government bond to shorter maturities such as 5 years. |

Capacity Constraint in Japan, 2000 - 2017 - Click to enlarge |

9. China beats growth estimates again

After a strong 2017, Chinese growth surprises on the upside again on solid exports and domestic consumption, despite continued financial deleveraging and more stringent environmental standards. Fixed-asset investment avoids a sharp deceleration, as corporate capex picks up tocompensate for the slowdown in property and infrastructure construction. New industries such as internet services, electrical vehicles and biotechnology post strong growth, in contrast to the decline in traditional manufacturing such as toys and footwear.

Headline growth comes in considerably above 6.5%. Consumer price inflation surprises on the upside by shooting above 3%, and producer prices continue to be supported by the government’s efforts to cut excess capacity in upstream industries such as steel making and coal. Strong real growth and high inflation lead to double-digit growth in nominal GDP for the second year in a row.

China’s debt-to-GDP ratio exhibits a sustained decline for the first time since the global financial crisis, thanks to the strong rise in nominal GDP and slower pace of debt accumulation. Higher inflation forces the People’s Bank of China (PBoC) to turn more hawkish and hike its policy interest rate. With much wider interest rate differentials with the US and a reversal of capital outflows, the Chinese renminbi appreciates against the USD by 5% or more in 2018.

10. Increased geopolitical tensions in the region

Geopolitics is back in Asia. While on the focus at present is on the tensions surrounding North Korea, other threats in the region that currently lying below the radar may pop up from time to time to catch the headlines.

The first candidate is the territorial dispute between Japan and China over Senkaku Islands (also known as Diaoyu Islands by the Chinese). The recent proposal by the Mayor of Ishigaki City of Japan to change the official name of the islands by explicitly adding the word “Senkaku” could presage a future escalation. The fresh mandate that Abe obtained after the snap election will likely allow him to make bolder moves in pursuing the LDP’s long-term agenda of amending Japan’s pacifist constitution. Nuclear threats from North Korea have clearly helped Abe make the case to the Japanese public. Tensions with China may provide some more momentum for such an agenda.

The contest for dominance between the US and China in the South China Sea has never stopped. The US navy has conducted at least three “freedom of navigation” patrols in waters claimed by China since the Trump administration took office. The Chinese military typically responds by sending warships to identify the US naval vessels and warn them away. Meanwhile, China’s militarisation of the man-made islands that it has built in the South China Sea continues. The frequent confrontations between the two navies risk leading to accidents.

In 2017, a two-month long military confrontation between the world’s two largest emerging economies (both nuclear powers) passed without the investment community even noticing it. However, the tensions between India and China over a small region called Doklam (or Donglang in Chinese) near the Himalayas has not really gone away. While the standoff between the two sides has come to an end, at least for now, both countries have beefed up their military presence in the region due to its strategic importance. War between India and China would not be without precedent. The latest major conflict between the two countries was in 1962, with thousands being killed or wounded, mostly on the Indian side.

Back to North Korea, a dramatic shock would come with China joining forces with Russia, the US and South Korea to invade North Korea. It is becoming increasingly clear that China is failing to exert significant influence on the Kim regime and contain its nuclear ambitions. To prevent the extremely undesirable outcome of the US gaining control of the entire Korean Peninsula after a disorderly collapse of the Kim regime, China may decide to take proactive action to secure its strategic interests in the region.

Tags: 2018 outlook,Featured,global macro,Macroview,newsletter,World economy