The US dollar remains under pressure. It is off for the third day against the yen and slipped below JPY109 for the first time in a little more than two weeks. The Nikkei struggled to cope with the foreign exchange developments, lost 2.3%, the most in a month, after gapping lower. At JPY108.50, the dollar would have given back 50% of its rally off the May 3 low near JPY105.50. Below there, the JPY107.80 is the 61.8% retracement. The euro is north of .12 after having briefly dipped below .11 at the start of the week. Last week’s high was set near .1245, and the 20-day average is found a little above .1250. Barring a very strong ADP report or a surprise from the ECB, the euro may head toward .13, which is a 38.2% retracement of the euro’s slide since key reversal from .16 on May 3. After dropping more than 1.5% over the past two sessions, sterling is stabilizing today. It is trading within yesterday’s ranges and holding above .44. The calm appears to be more a function of the softer dollar than positive developments in the UK. One-month implied volatility remains elevated near 20% (closed last week near 16.6%), and the put/call skew is more extreme with puts favored by 6,2% (closed last week near 5.6%). Click to enlarge.

Topics:

Marc Chandler considers the following as important: AUD, EUR, Featured, FX Daily, FX Trends, GBP, JPY, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

The US dollar remains under pressure. It is off for the third day against the yen and slipped below JPY109 for the first time in a little more than two weeks. The Nikkei struggled to cope with the foreign exchange developments, lost 2.3%, the most in a month, after gapping lower. At JPY108.50, the dollar would have given back 50% of its rally off the May 3 low near JPY105.50. Below there, the JPY107.80 is the 61.8% retracement.

|

|

|

The euro is north of $1.12 after having briefly dipped below $1.11 at the start of the week. Last week’s high was set near $1.1245, and the 20-day average is found a little above $1.1250. Barring a very strong ADP report or a surprise from the ECB, the euro may head toward $1.13, which is a 38.2% retracement of the euro’s slide since key reversal from $1.16 on May 3.

After dropping more than 1.5% over the past two sessions, sterling is stabilizing today. It is trading within yesterday’s ranges and holding above $1.44. The calm appears to be more a function of the softer dollar than positive developments in the UK. One-month implied volatility remains elevated near 20% (closed last week near 16.6%), and the put/call skew is more extreme with puts favored by 6,2% (closed last week near 5.6%).

|

Click to enlarge. |

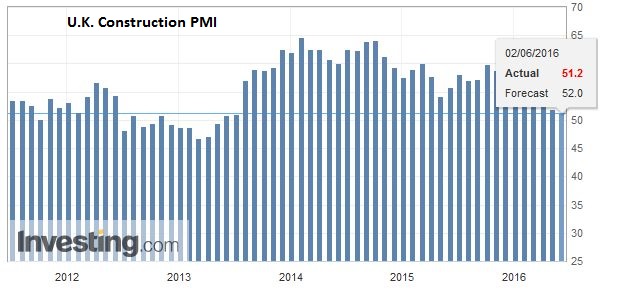

United KingdomAlthough the UK’s manufacturing PMI was a bit stronger than expected yesterday, pushing back just above the 50 boom/bust level, today’s construction PMI was poor at 51.2, down from 52.0 (median expected unchanged). The construction PMI has not risen once this year, and the May reading is the second lowest in its brief history (mid-2013). The average in Q1 was 54.5. |

Click to enlarge. |

United StatesThere are two readings of the US labor market for investors today. First is the weekly jobless claims. This is the closest thing to a real-time check of US jobs. There has been some deterioration in recent weeks which is partly a function of strike activity. The four-week moving average has risen to 278k, its highest level since the end of January. Second, is the ADP estimate for private sector employment. The median forecast on Bloomberg is for an increase in ADP from 156k in April to 173k in May.

|

Click to enlarge. |

Graphs and additional information on Swiss Franc by the snbchf team