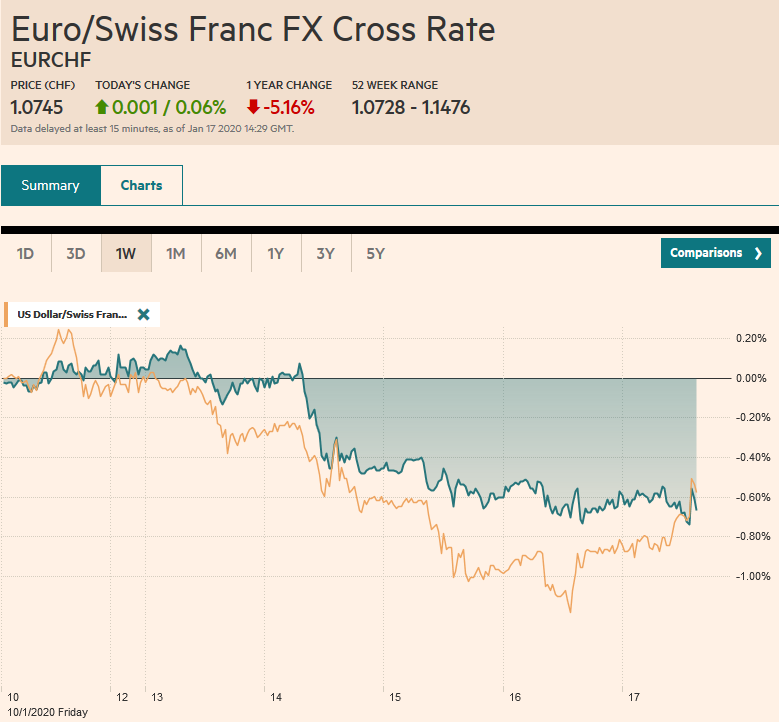

Swiss Franc The Euro has risen by 0.06% to 1.0745 EUR/CHF and USD/CHF, January 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Helped by new record highs in the US, global stocks are moving higher today. Nearly all the markets in the Asia Pacific region advanced and the seventh consecutive weekly rally is the longest in a couple of years. Europe’s Dow Jones Stoxx 600 is at new record highs and appears set to take a four-day streak into next week. US shares are trading firmly. Since the end of last September, the S&P 500 has fallen in only three weeks. A shockingly poor UK retail sales report is helping to extend the decline in UK interest rates. The 10-year yield is off a couple basis points to bring this

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, Currency Movement, EUR/CHF, Featured, Federal Reserve, FX Daily, newsletter, Singapore, U.K., USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.06% to 1.0745 |

EUR/CHF and USD/CHF, January 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Helped by new record highs in the US, global stocks are moving higher today. Nearly all the markets in the Asia Pacific region advanced and the seventh consecutive weekly rally is the longest in a couple of years. Europe’s Dow Jones Stoxx 600 is at new record highs and appears set to take a four-day streak into next week. US shares are trading firmly. Since the end of last September, the S&P 500 has fallen in only three weeks. A shockingly poor UK retail sales report is helping to extend the decline in UK interest rates. The 10-year yield is off a couple basis points to bring this week’s decline to more than 13 bp. The implied yield on the March short-sterling futures contract has fallen almost 20 bp since the end of last year. Other European bonds yields are mostly a little softer. The US 10-year yield is steady a little above 1.80%. The dollar is paring its weekly loss against most of the major currencies. The yen and sterling underperformed this week. The JP Morgan Emerging Market Currency Index is a touch higher today but is off about a quarter of a percent this week. Gold is a little higher but is still poised to snap a five-week rally. Oil is little, and the March WTI contract is nursing a loss of about 0.75% on the week. |

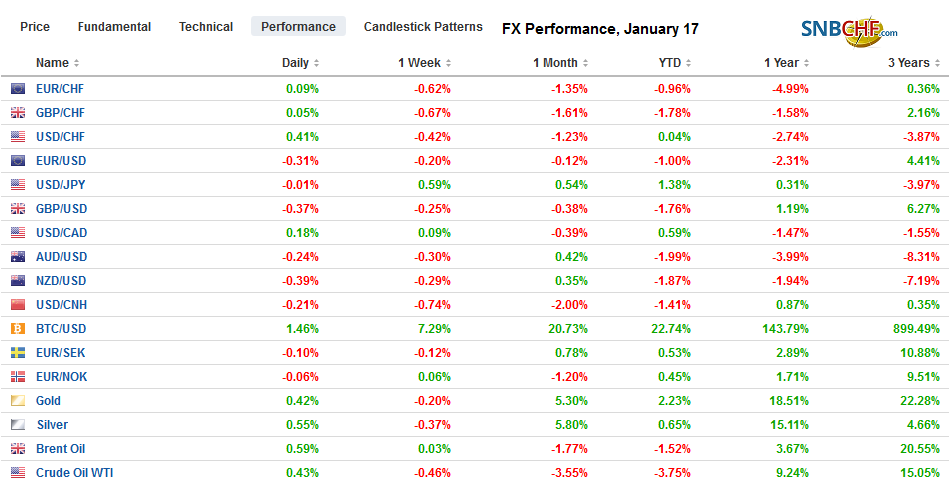

FX Performance, January 17 - Click to enlarge |

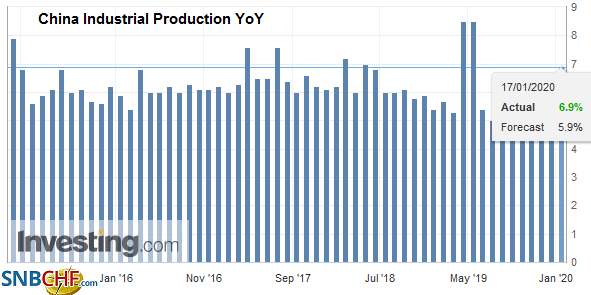

Asia PacificChina’s data showed that even though the economy slowed, it ended on a solid note, and appeared to be finding some traction before the trade deal was struck. With most US tariffs still in place, the trade deal might buy Beijing some time, but it does not appear to directly help the world’s second-largest economy. Some of the liberalization efforts may support growth indirectly, and the imports of foodstuff may help ease prices. The economy grew 1.5% in Q4 for a 6% year-over-year rate. December industrial output rose 6.9% from 6.2% year-over-year in November and is the best since March. Retail sales rose 8.0%, the same as in November. Investment in fixed assets rose (5.4% vs. 5.2%) for the first time since June. |

China Industrial Production YoY, December 2019(see more posts on China Industrial Production, ) Source: investing.com - Click to enlarge |

Japan’s sales tax increase and typhoon in October distorted economic activity, and outside of consumption, the economy appears to be recovering. The November tertiary index rose 1.3%, which is a bit more than expected, but the October series was revised down to show a 5.2% decline instead of 4.6% that was initially reported.

Separately, Singapore reported non-oil exports rose 1.1% in December. Economists had expected a decline. Singapore is often seen to capture the regional economic trends, and its trade figures are consistent with improved intra-regional trade. That said, electronic exports were weak, falling 21.3% year-over-year. Economists had expected greater improvement after the 23.3% decline in November. Back near the middle of the year, electronic exports were off closer to a third than a quarter.

The dollar stretched to new eight-month highs against the yen near JPY110.30. A band of resistance is seen in the JPY110.50-JPY110.70 area. There is an option for nearly $400 mln JPY110.40 that will be cut today. The Australian dollar is steady to higher. The last five sessions have seen it close in a tight range of $0.6898-$0.6904. A large expiring option (A$1.3 bln) may cap the upside in front of $0.6925. The Chinese yuan extended its recent gains to new six-month highs. The dollar saw CNY6.8535 for the first time since early last July. Today’s move brings the dollar’s loss since last September’s peak to about 4.6%.

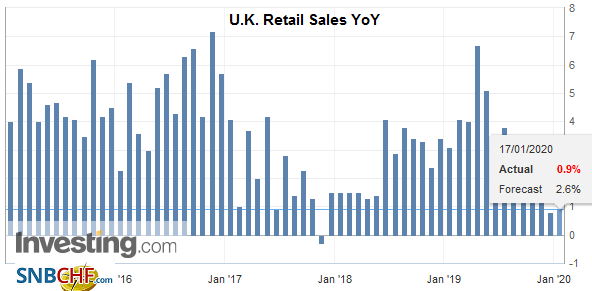

EuropeUK December retail sales were dismal. Instead of rising by 0.6%, as the median forecast in the Bloomberg survey anticipated, retail sales fell by 0.6% and adding insult to injury, the November series was revised to show a 0.8% decline rather than 0.6%. Excluding petrol, retail sales dropped by 0.8%, matching the November decline. Neither the election results nor Black Friday and Cyber Monday sales appeared to lift the UK consumer spirits. The retail sales deflator fell by 0.6%, suggesting lower prices may have exaggerated the decline. Still, retail sales have been flat or falling for the last five months of 2019. Given the recent spate of comments from officials, the market has moved to discount a 75% chance of a rate cut when the BOE meets on January 30. A week ago, the odds were less than 25%. |

U.K. Retail Sales YoY, December 2019(see more posts on U.K. Retail Sales, ) - Click to enlarge |

| Germany, as it is well appreciated, runs a budget surplus. Many critics, largely outside of Germany, do not approve, and especially with negative interest rates. However, German ordoliberalism rejects demand management through fiscal policy, and the problem with debt is not tied to the cost. Merkel has signaled, though, a willingness to open the purse strings. Specifically, she is endorsing a 40 bln euro plan to help regions, utilities, and workers transition away from coal. |

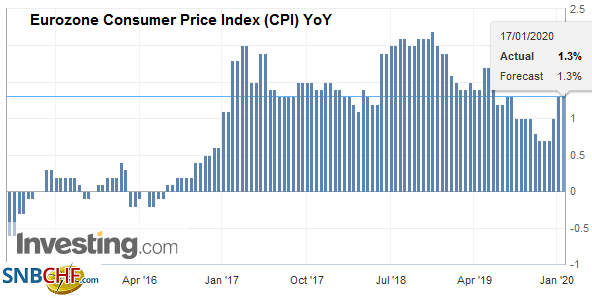

Eurozone Consumer Price Index (CPI) YoY, December 2019(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

| German missed the 2020 targets of the Paris Agreement, and this seems to be a classic Merkel move. She steals some of the thunder from the Greens, who the CDU might have to be in a national alliance with under certain conditions in the coming years (and has been tried in a few state governments). The risk is she exposes her right-flank. The AfD has made inroads in the east, which is more dependent on coal.This is also an issue for central and eastern Europe. It ought not to surprise if Merkel found an issue that allows her to tack to the right and protect the CDU/CSU’s flank. |

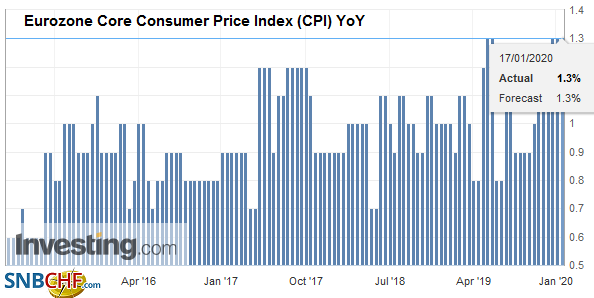

Eurozone Core Consumer Price Index (CPI) YoY, December 2019(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The euro peaked in front of $1.1175 yesterday, reversed lower. Follow-through selling today has pushed it a little below $1.1115 in the European morning. Chunk option expirations today by impact activity. There are 2.7 bln euros of options struck in the $1.1120-$1.1125 area and another set for 1.6 bln euros at 1.1100. Above the market are options for 2.1 bln euro at $1.1150. The euro finished last week near $1.1120. Sterling was bid to a new high for the week (almost $1.3120) before the retail sales disappointment saw it reverse course. A break and close below yesterday’s low (~$1.3025) would weaken the technical tone. Sterling closed near $1.3065 last week.

America

Some observers still insist that the Fed’s T-bill purchases and repo operations are equivalent to quantitative easing (QE) though the officials deny this vehemently. Sometimes the rally in US stocks to new record highs is cited as evidence, even though stocks rallied strongly before the Fed announced the T-bill purchases and sustained repo operations. From December 2018, low through August 2019, the S&P 500 gained almost 30% and has risen another roughly 11.5% since the end of September 2019. The Fed indicated it will reduce the amount offered in the term repos starting next month to $30 bln from $35 bln. Did it just tighten a bit? Probably after the mid-April tax date, the Fed will likely reduce its new T-bill purchases ($60 bln a month through it says some time in Q2) and maintain rolling over maturing issues to maintain the size of its balance sheet. It is not just a case of should it be seen as a tightening or tapering, but will it, in fact, be seen as such by the investment community? Net-net Fed expectations are mostly unchanged since the middle of June. On June 14, the implied yield of the December 2020 fed funds futures contract closed at 1.39%. It is now 1.36%.

The US Treasury announced that it will soon begin issuing 20-year bonds. The Trump Administration has been pushing to issue longer-dated securities to take advantage of the low-interest rates. However, there was a pushback against the 50-year and 100-year bonds that the administration appeared to favor. The 20-year issue is a fair compromise. = It is longer than the average maturity of the outstanding marketable Treasuries, which is a little less than six years. The new supply consideration saw the much-watched 2-10 year yield curve steepen a little. It had flattened by around 12 basis points since the start of the year when it was about 34 bp.

President Trump formally nominated Shelton and Waller to the Board of Governors of the Federal Reserve. It has long been signaled that this was likely to be the case, though why it took so long is a bit of a mystery. In any event, Shelton is the more controversial nomination, but she has been through the confirmation process to secure her current post as Executive Director of the European Bank for Reconstruction and Development. Waller is from the hallowed institution itself, as Director of Research at the St. Louis Fed. Both advocate easier monetary policy.

The US reports December housing starts and permits, and industrial production figures today. Housing starts are expected to have edged higher, but permits may come in lower. Industrial output and manufacturing are more important data points, and after a surge (1.1% gain for both) in November, as autoworkers returned, a small decline is expected. Preliminary January consumer confidence by the University of Michigan and its long-term inflation expectation component (was 2.2% in December) will draw some attention. Economists, more than market participants, watch the JOLTS job opening report. Canada’s portfolio flows report (November) attracts some interest.

The Canadian dollar is flat on the day and has gone nowhere this week. A week ago, the greenback finished near CAD1.3050 and now is stuck in a narrow range near CAD1.3040. There is an $820 mln option at CAD1.3030 that will be cut today. The US dollar remains in the range set on January 9 (CAD1.3025-CAD1.3105). Meanwhile, the greenback continues to bleed lower against the Mexican peso. It has fallen every week since the end of November but one. The dollar closed last week near MXN18.7950. It is testing the MXN18.75 area today. The high real and nominal yields continue to attract savings and levered accounts like it as a carry-trade against the yen. The Dollar Index enjoys a slightly firmer bias today and is near 97.40. It finished last week near 97.35.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,China,Currency Movement,EUR/CHF,Featured,federal-reserve,FX Daily,newsletter,Singapore,U.K.,USD/CHF