Joseph Y. Calhoun

October 10, 2021

SNB & CHF

Bonds sold off again last week with the yield on the 10 year Treasury closing over 1.6% for the first time since early June. The yield is now down just 16 basis points from the high of 1.76% set on March 30. But this rise in rates is at least a little different than the fall that preceded it. When nominal rates fell from April through July, real rates fell right along with them. The nominal bond yield fell by 63 basis points and the 10 year TIPS yield fell by 57....

Read More »

Stephen Flood

October 9, 2021

SNB & CHF

In our post on January 28, 2021 “Gold, The Tried-and-True Inflation Hedge for What’s Coming!” we outlined four reasons that we expect higher inflation over the next several years. The brief bullet points are:

Money Supplies have risen dramatically

Commodity Prices are rising again

Reduced Globalization as ‘Made at Home’ policies are proliferating

Pent up demand

Headlines such as this one last week from Bloomberg “Inflation gauge Hits Highest Since 1991 as Americans...

Read More »

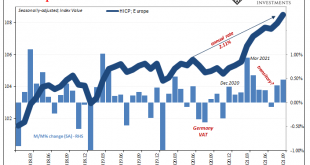

Jeffrey P. Snider

October 7, 2021

SNB & CHF

We’ve got one central bank over here in America which appears as if its members can’t wait to “taper”, bringing up both the topic and using that particular word as much as possible. Jay Powell’s Federal Reserve obviously intends to buoy confidence by projecting as much when it does cut back on the pace of its (irrelevant) QE6.

On the other side of the Atlantic, Europe’s central bank will be technically be doing the same thing likely at the same time. Except,...

Read More »

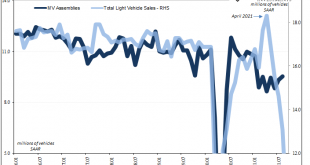

Jeffrey P. Snider

October 5, 2021

SNB & CHF

Last night, Autodata reported its first estimates for September auto sales in the US. According to its own as well as those compiled by the Bureau of Economic Analysis (the same government outfit which keeps track of GDP), vehicle sales have been sliding overall ever since April. For a couple months in the middle of Uncle Sam’s helicopter-fed frenzy, the number of vehicle units had surged to a high of more than 18 million (seasonally-adjusted annual rate) in both...

Read More »

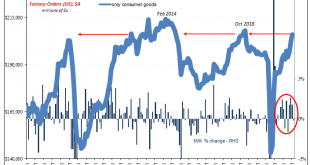

Jeffrey P. Snider

October 5, 2021

SNB & CHF

US factories are humming along, constrained only by supply issues which might occasionally limit production. That’s the story, anyway. There’s too much business because of them, manufacturers taking in only more orders by the day leaving them struggling to catch up.

But what kind of stuff is it that is being ordered from our nation’s factories?

Without thinking too much about it, you’d probably say that they’re ridiculously busy trying as best as possible to fill...

Read More »

Joseph Y. Calhoun

October 3, 2021

SNB & CHF

How often do you check your brokerage account? There is a famous economics paper from 1997, written by some of the giants in behavioral finance (Thaler, Kahnemann, Tversky & Schwartz), that tested what is known as myopic loss aversion. What they found was that investors who check their performance less frequently are more willing to take risk and experience higher returns. Investors who check their results frequently take less risk and perform worse. And that...

Read More »

Jeffrey P. Snider

October 3, 2021

SNB & CHF

The inventory saga, planetary in its reach. As you’ve heard, American demand for goods supercharged by the federal government’s helicopter combined with a much more limited capacity to rebound in the logistics of the goods economy left a nightmare for supply chains. As we’ve been writing lately, a highly unusual maybe unprecedented inventory cycle resulted (creating “inflation”).

The worse the shipping snafus, the more was ordered and piled into it – if for no...

Read More »

Jeffrey P. Snider

September 30, 2021

SNB & CHF

Is it delta COVID? Or the widely reported labor shortage? Something has created a soft patch in the presumed indestructible US economy still hopped up on Uncle Sam’s deposits made earlier in the year. And yet, there’s a nagging feeling over how this time, like all previous times, just might be too good to be true, too.

To start with, the rebound from last year’s recession is decidedly, maybe even uniquely uneven. Not just explosive goods sector vs. moribund...

Read More »

Jeffrey P. Snider

September 29, 2021

SNB & CHF

One reason why I still believe the US most likely would have entered a recession at some point in 2020 even without COVID wasn’t just the yield curve inversion that popped up several months before then. In August of 2019, the small part of the Treasury curve most people pay attention to (2s10s) did send out that dreaded signal, suggesting already to expect contraction in the intermediate term ahead of then.

But there was more to it than that, much moving in the...

Read More »

Jeffrey P. Snider

September 24, 2021

SNB & CHF

You’ve heard of the virtuous circle in the economy. Risk taking leads to spending/investment/hiring, which then leads to more spending/investment/hiring. Recovery, in other words.

In the old days of the 20th century, quite a lot of the circle was rounded out by the inventory cycle. Both recession and recovery would depend upon how much additional product floated up and down the supply chain. Deflation, too.

On the contraction side, demand might fall off a bit for...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org