The inventory saga, planetary in its reach. As you’ve heard, American demand for goods supercharged by the federal government’s helicopter combined with a much more limited capacity to rebound in the logistics of the goods economy left a nightmare for supply chains. As we’ve been writing lately, a highly unusual maybe unprecedented inventory cycle resulted (creating “inflation”). The worse the shipping snafus, the more was ordered and piled into it – if for no other reason than to increase the odds of receiving something out of the supply mess particularly before the upcoming Christmas holiday almost everyone believes will be total gangbusters. Believed? . On the other hand, should it not go so smoothly on the demand side, then we’d expect to see softening

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, China, china nbs manufacturing pmi, china nbs non-manufacturing pmi, currencies, economy, exports, Featured, Federal Reserve/Monetary Policy, global trade, Inventory, inventory cycle, manufacturing, Markets, new export orders, new orders, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The inventory saga, planetary in its reach. As you’ve heard, American demand for goods supercharged by the federal government’s helicopter combined with a much more limited capacity to rebound in the logistics of the goods economy left a nightmare for supply chains. As we’ve been writing lately, a highly unusual maybe unprecedented inventory cycle resulted (creating “inflation”).

The worse the shipping snafus, the more was ordered and piled into it – if for no other reason than to increase the odds of receiving something out of the supply mess particularly before the upcoming Christmas holiday almost everyone believes will be total gangbusters. Believed? |

. |

| On the other hand, should it not go so smoothly on the demand side, then we’d expect to see softening perhaps more than that for new orders from down at the production level. Retailers and wholesales may have been confident in Uncle Sam’s “stimulus” holding off the worst potential about this rush of inventory, a very different story if demand does not keep to the plan.

The unusual inventory cycle then risks transforming into its classic case more like what used to be of downturn even recession. New orders, then, that’s what to watch. |

. |

. |

|

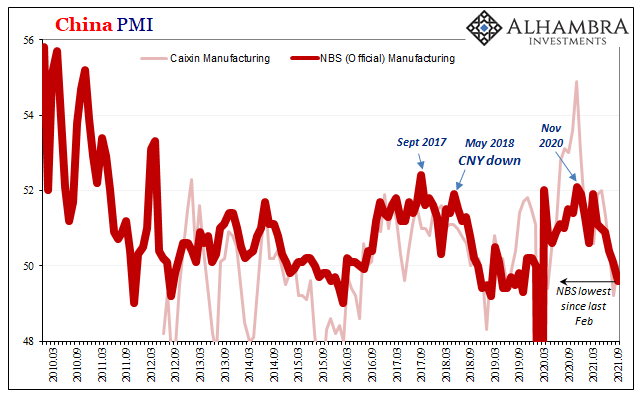

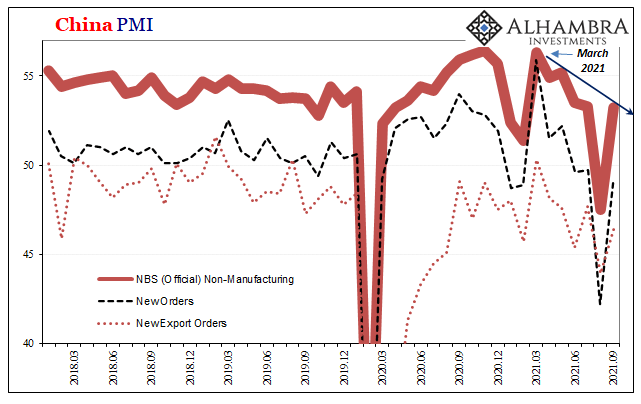

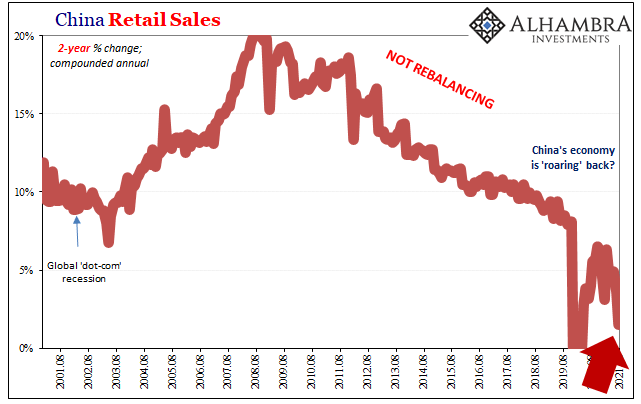

| According to China’s National Bureau of Statistics (NBS) late last night, that country’s official manufacturing PMI dropped under 50 for the first time since February 2020. At 49.6, it’s not how far under fifty – not far – that’s the plain issue, rather the unbroken and ongoing declining trend as well as the timing of its arrival. Like inflation numbers in the US or globally more deflationary bond yields, March and April will still have marked a turning point.The reason for this sub-50 market, to our inventory point, just ugly for…new orders. Such gross colorization includes lessening rather than quickening for both internal Chinese demand (the index of total New Orders for Chinese manufacturers was 49.5) as well as what China’s manufacturers have been trying to send overseas, the United States in particular (the index of orders for export at 49.3). |

. |

| But that’s just COVID!

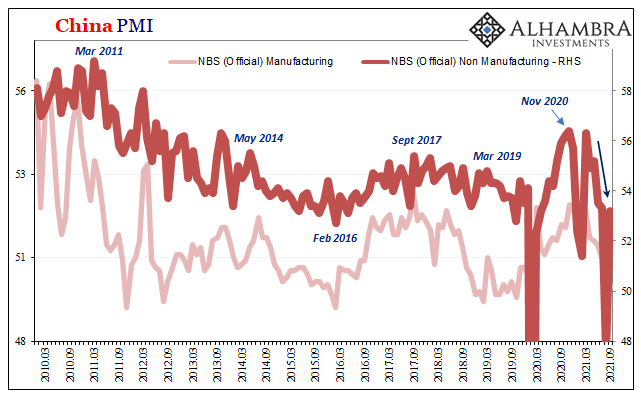

This was certainly the claim for the abysmal numbers in China outside of manufacturing during August. The NBS had put its non-manufacturing index as one of the worst in the entire series. Much of that extreme may, indeed, have been attributable to renewed pandemic measures which, apparently, didn’t spillover into September. The official PMI for services rebounded from that awful low of 47.5 last month to a still-low 53.2 this month. While certainly better, 53.2 is less than July’s 53.5 because being substantially below 50 in new orders – both overall as well as the one for export. |

. |

. |

|

| In other words, if the depth of August’s obscene drop was COVID, then into September that the downtrend continued regardless.

This, then, indicates that the further deterioration in Chinese manufacturing presented by the latest PMI estimates sure wasn’t very likely to have been the coronavirus. If it had been, why no rebound at all? Services reopened up, yet still dented by the weakening economy while manufacturing continues to suffer worse from the same underlying problem. That’s not inflation.But it just might be inventory. Like several regional Fed manufacturing surveys lately, it’s still too early to draw hard conclusions but the possibility keeps rising by the month; by the datapoint no matter where it originates. |

. |

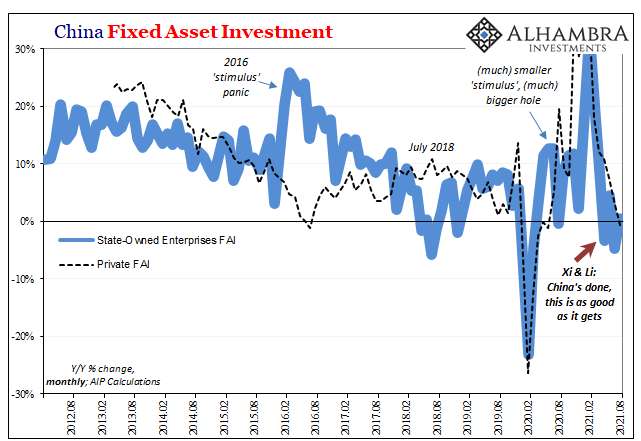

| If there is anything somewhat surprising, it’s not that this inventory issue may be working out in this way, rather how quickly it may have come about. In the end, the global economy gets globally synchronized more often than not, just never in legit, inflationary growth. |

. |

You Might Also Like

Revisiting The Last Overhang

Revisiting The Last Overhang

2021-09-29

One reason why I still believe the US most likely would have entered a recession at some point in 2020 even without COVID wasn’t just the yield curve inversion that popped up several months before then. In August of 2019, the small part of the Treasury curve most people pay attention to (2s10s) did send out that dreaded signal, suggesting already to expect contraction in the intermediate term ahead of then.

Weekly Market Pulse: Not So Evergrande

Weekly Market Pulse: Not So Evergrande

2021-09-27

US stocks sold off last Monday due to fears over the potential – likely – failure of China Evergrande, a real estate developer that has suddenly discovered the perils of leverage. Well that and the perils of being in an industry not currently favored by Xi Jinping. He has declared that houses are for living in not speculating on and ordered the state controlled banks to lend accordingly.

What’s Real Behind Commodities

What’s Real Behind Commodities

2021-09-08

Inflation is sustained monetary debasement – money printing, if you prefer – that wrecks consumer prices. It is the other of the evil monetary diseases, the one which is far more visible therefore visceral to the consumers pounded by spiraling costs of bare living. Yet, it is the lesser evil by comparison to deflation which insidiously destroys the labor market from the inside out.

A Real Example Of Price Imbalance

A Real Example Of Price Imbalance

2021-08-11

It’s not just the trade data from individual countries. Take the WTO’s estimates which are derived from exports and imports going into or out of nearly all of them. These figures show that for all that recovery glory being printed up out of Uncle Sam’s checkbook, the American West Coast might be the only place where we can find anything resembling Warren Buffett’s red-hot claim.

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market

2021-07-15

And just like that, snap of the fingers, it’s gone. Without a “bad” Treasury auction, there was no stopping the bond market today from retracing all of yesterday’s (modest) selloff and then some. This despite the huge CPI estimates released before the prior session’s trading, and now PPI figures that are equally if not more obscene.

ISM’s Nasty Little Surprise Isn’t Actually A Surprise

ISM’s Nasty Little Surprise Isn’t Actually A Surprise

2021-07-07

Completing the monthly cycle, the ISM released its estimates for non-manufacturing in the US during the month of June 2021. The headline index dropped nearly four points, more than expected. From 64.0 in May, at 60.1 while still quite high it’s the implication of being the lowest in four months which got so much attention.

The Inflation Emotion(s)

The Inflation Emotion(s)

2021-06-10

Inflation is more than just any old touchy subject in an age overflowing with crude, visceral debates up and down the spectrum reaching into every corner of life. It is about life itself, and not just quality. When the prices of the goods (or services) you absolutely depend upon go up, your entire world becomes that much more difficult.

Real Dollar ‘Privilege’ On Display (again)

Real Dollar ‘Privilege’ On Display (again)

2021-04-08

Twenty-fifteen was an important yet completely misunderstood year. The Fed was going to have to become hawkish, according to its models, yet oil prices crashed and the dollar continued to rise. Both of those things were described as “transitory” by Janet Yellen, and that they were helpful or positive (rising dollar means cleanest dirty shirt!), but domestically American policymakers’ clear lack of conviction and courage about that rate hike regime showed otherwise.

Tags: Bonds,China,china nbs manufacturing pmi,china nbs non-manufacturing pmi,currencies,economy,exports,Featured,Federal Reserve/Monetary Policy,global trade,Inventory,inventory cycle,manufacturing,Markets,new export orders,new orders,newsletter