Swiss Economicblogs.org

Swiss Economicblogs.org

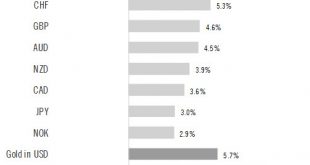

Although close to the end of a long-term up-cycle, the dollar has the potential to recover ground lost recently given the outlook for Fed rate rises and balance sheet reduction.Our latest forecasts for major currencies over the coming months can be summarised as follows:US dollar. In terms of duration and valuation, the USD up-cycle is likely close to ending. However, the USD is likely to remain strong on the back of robust US growth and the outlook for inflation. It should also benefit from...

Read More »Major currencies’ outlook