Swiss Economicblogs.org

Swiss Economicblogs.org

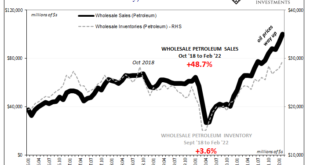

The Census Bureau provided some updated inventory estimates about wholesalers, including its annual benchmark revisions. As to the latter, not a whole lot was changed, a small downward revision right around the peak (early 2021) of the supply shock which is consistent with the GDP estimates for when inventory levels were shrinking fast. What’s worth noting about the figures now is how much of a problem there is in terms of petroleum. By that I mean two ways. First,...

Read More »Concocting Inventory