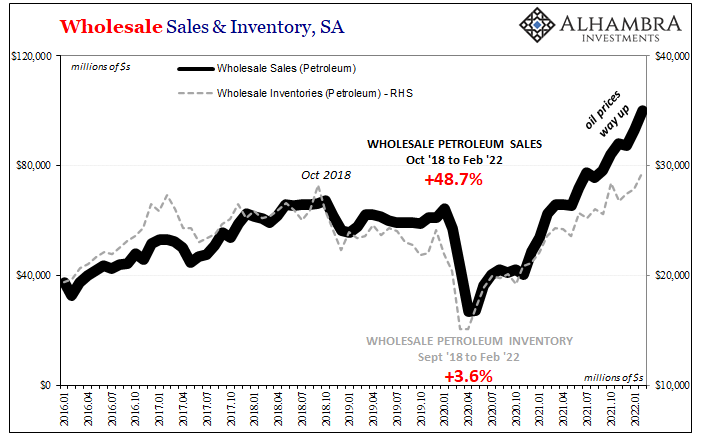

The Census Bureau provided some updated inventory estimates about wholesalers, including its annual benchmark revisions. As to the latter, not a whole lot was changed, a small downward revision right around the peak (early 2021) of the supply shock which is consistent with the GDP estimates for when inventory levels were shrinking fast. What’s worth noting about the figures now is how much of a problem there is in terms of petroleum. By that I mean two ways. First, wholesale sales of petroleum have absolutely skyrocketed, no surprise. Just amazing the level of increase, keeping in mind much of it due to price changes rather than as-rapid volume expansion. According to the estimates now for February 2022, dollar-value sales of crude and whatnot were just about 50%

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, currencies, economy, Featured, Federal Reserve/Monetary Policy, FOMC, inflation, Markets, newsletter, rate hikes, supply chain, wholesale inventory, wholesale sales, Yield Curve, yield curve inversion

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The Census Bureau provided some updated inventory estimates about wholesalers, including its annual benchmark revisions. As to the latter, not a whole lot was changed, a small downward revision right around the peak (early 2021) of the supply shock which is consistent with the GDP estimates for when inventory levels were shrinking fast.

What’s worth noting about the figures now is how much of a problem there is in terms of petroleum. By that I mean two ways. First, wholesale sales of petroleum have absolutely skyrocketed, no surprise. Just amazing the level of increase, keeping in mind much of it due to price changes rather than as-rapid volume expansion. According to the estimates now for February 2022, dollar-value sales of crude and whatnot were just about 50% higher than the previous peak set back in October 2018 entering that “cycle’s” landmine event. For all that, inventories of the same commodity aren’t even 4% more than back in September 2018 (the prior top for inventory). |

|

| This disparity, obviously, reflected in price yet also of production (lack of). Unless the FOMC has a secret fracking code hidden within its rate hikes, what good will they otherwise do? (I know, I know; their true purpose is shock-psychology, therefore the rabidness of these hawks lately).

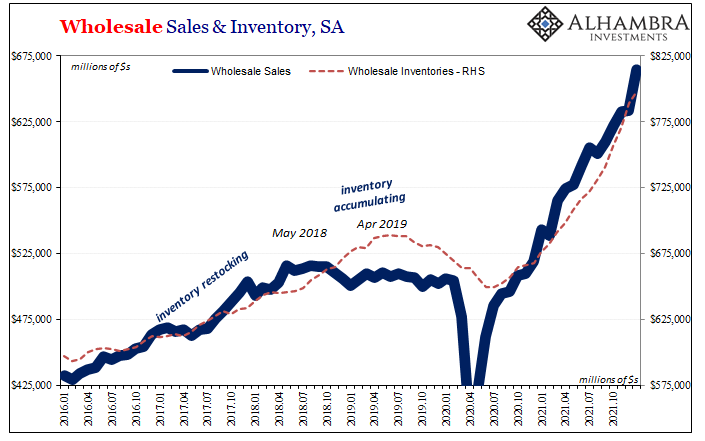

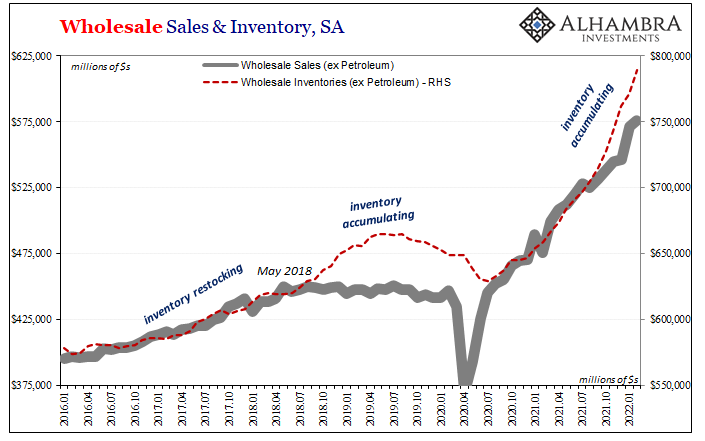

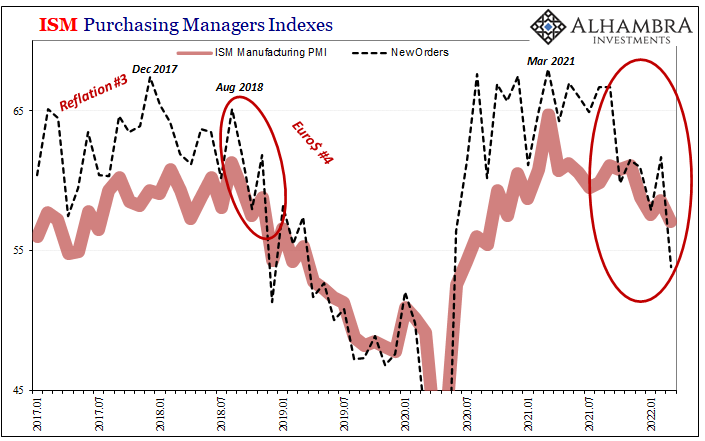

If you don’t account for the supply shock rather than actual inflation hidden within the oil patch, mismatch rebound in demand versus restricted supply, then the entire wholesale level of the supply chain appears to be itself relatively well balanced, so inflation. Even as inventories surge in historic fashion, overall wholesale sales have kept pace. Removing petroleum, however, you then see the wider economic problem. |

|

| Since crude inventories are not growing, not really, that means wholesale inventories outside of oil must be accumulating that much more rapidly. On the other side, since wholesale sales of petroleum remain wild, wholesale sales apart from those are a little less heated.

The remainder is a widening gap inventory over sales. And it really goes back to around last September and October (as the curves priced in addition to the stupidity of the debt ceiling). |

|

|

|

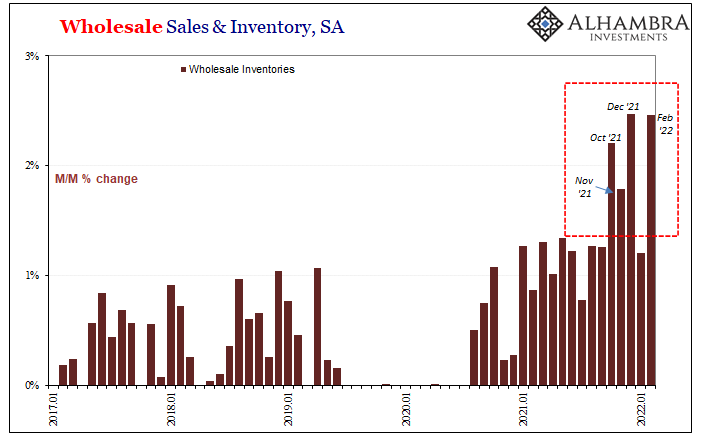

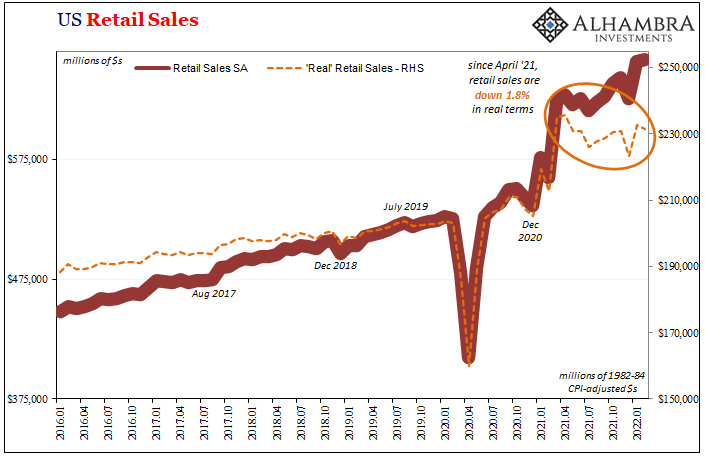

| These revisions to the wholesale inventory data now put four of the last five months as the four highest single-month increases on record (which includes price effects). Again, though wholesale sales remain brisk (also including price effects), they aren’t as brisk outside energy, as the supply chain scales have tipped more definitively toward accumulation of goods and product.

And there’s more coming. The second major problem indicated by the petroleum imbalance is demand destruction. Wholesalers are having no trouble whatsoever moving oil and gasoline up to the retail level though prices have surged dramatically. |

|

| Could that be partly responsible for a slightly less pace to wholesale sales elsewhere around the goods economy?

Demand destruction takes place when consumers forced to pay more for necessities like gasoline then can’t afford to spend on other things, such as the way they might have last year when stuck at home shopping online using Uncle Sam as everyone’s (debt-ridden) benefactor. |

|

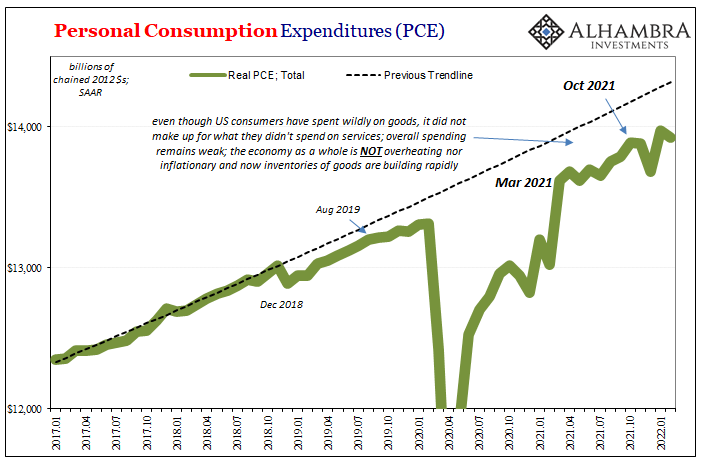

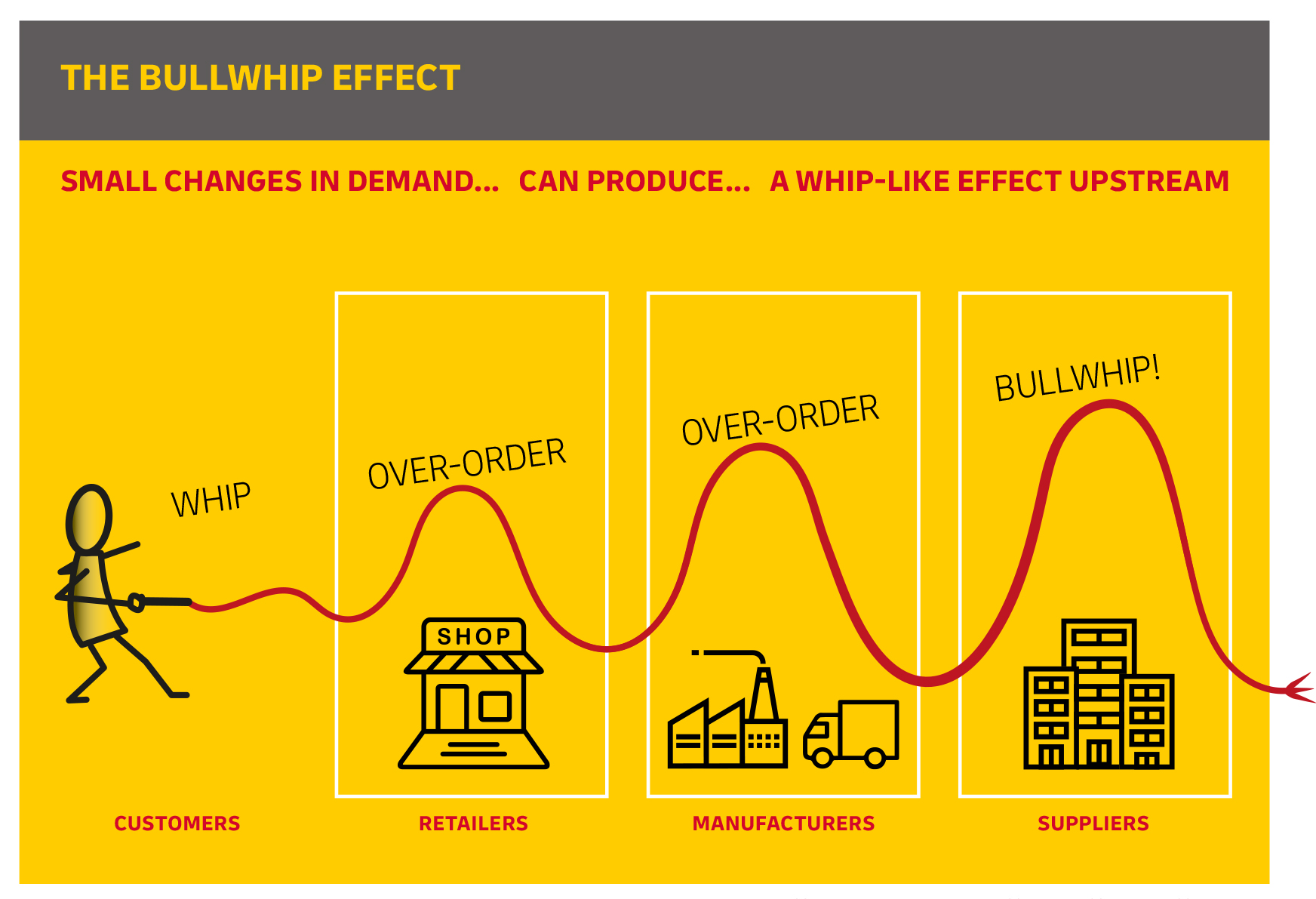

| More for gas and groceries, less from the feds, and the hot flame for the rest of last year’s goods economy begins to cool, if slowly at first. This, though, merely sets up for what economists call the bullwhip effect, and given the huge upswell in that goods economy from last year’s artificiality there’s more to the whip possible this time compared to others.

One whitepaper on this subject from 2020 co-authored by DHL wrote, “Time and again, it has been shown that industry’s favourite strategy in times of uncertainty is to stockpile,” and do so regardless of demand. |

|

Note: the graphic on bullwhip effect was taken from this paper

|

|

|

|

| Nearing two years later, oh yeah, just-in-case is just now timed to show itself.

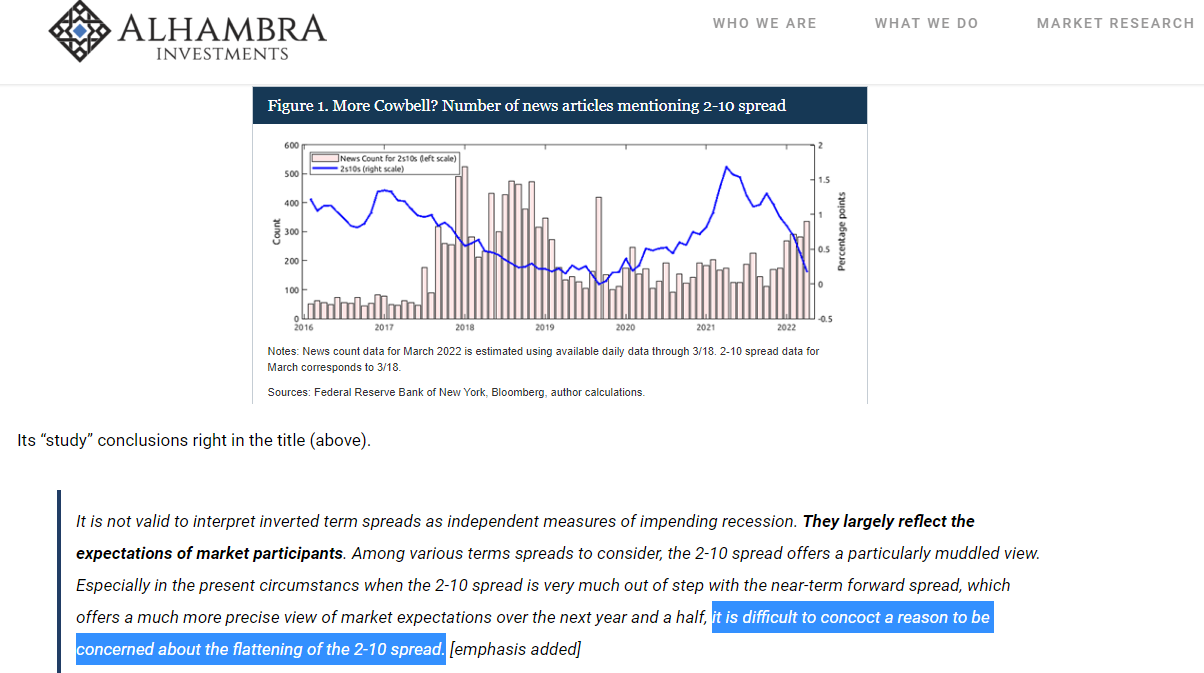

In 2022, as demand maybe starts to cool off, or has, and actually does more so in other places first like Europe, the case for just-in-case reverses only with the other end of the whip far more exposed. That’s the risk, anyway, and a(n honest) survey around the world shows a possible beginning to it – rather than omicron or Russia – from even before the Fed’s first move. For the FOMC, contrary to the ECB or PBOC, US policymakers will be hiking rates based on what they see of the petroleum imbalance alone, factoring that consumers and businesses will focus exclusively on it, too, while instead it likely will be everything else what makes the economic difference only in the other direction. Contrary to what nonsense Fed researchers keep serving, the case(s) behind curve inversion(s) just isn’t challenging to “concoct.” |

|

You Might Also Like

We Can Only Hope For Another (bond) Massacre

We Can Only Hope For Another (bond) Massacre

2022-03-30

To begin with, the economy today is absolutely nothing like it had been almost thirty years ago. That fact in and of itself should end the discussion right here. However, comparisons will be made and it does no harm to review them.I’m talking about 1994, or, more specifically, the eleven months between late February 1994 and early February 1995.

Inversion Is The Real March Madness, Just Don’t Take It Literally

Inversion Is The Real March Madness, Just Don’t Take It Literally

2022-03-22

With such low levels of self-awareness, it isn’t surprising that the FOMC’s members continue to pour gasoline on the already-blazing curve fire. March Madness is supposed to be on the courts of college basketball, instead it is playing out more vividly across all financial markets.

Consumer Prices And The Historical Pain(s)

Consumer Prices And The Historical Pain(s)

2022-03-12

The 1947-48 experience was truly painful, maybe even terrifying. The US and Europe had just come out of a decade when the worst deflationary consequences were so widespread that the period immediately following quickly erupted into the worst conflagration in human history.

The Red Warning

The Red Warning

2022-02-24

Now it’s the Russian’s fault. Belligerence surrounding Donbas and Ukraine, raw materials and energy supplies to Europe threatened by Putin’s coiled bear. Why wouldn’t markets grow worried?There’s always a reason why we shouldn’t take these things seriously, or quickly dismiss them out of hand as the temporary product of whichever political fear-of-the-day.

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

2022-01-28

It’s not hard to reason why there continues to be this conflict of interest (rates). On the one hand, impacting the short end of the yield curve, the unemployment rate has taken a tight grip on the FOMC’s limited imagination. The rate hikes are coming and the markets like all mainstream commentary agree that as it stands there’s nothing on the horizon to stop Jay Powell’s hawkishness.

The Hawks Circle Here, The Doves Win There

The Hawks Circle Here, The Doves Win There

2022-01-26

We’ve been here before, near exactly here. On this side of the Pacific Ocean, in the US particularly the situation was said to be just grand. The economy was responding nicely to QE’s 3 and 4 (yes, there were four of them by that point), Federal Reserve Chairman Ben Bernanke had said in the middle of 2013 it was becoming more than enough, creating for him and the FOMC coveted breathing space so as to begin tapering both of those ongoing programs.A full and complete recovery he believed was on schedule if not getting way ahead of it.

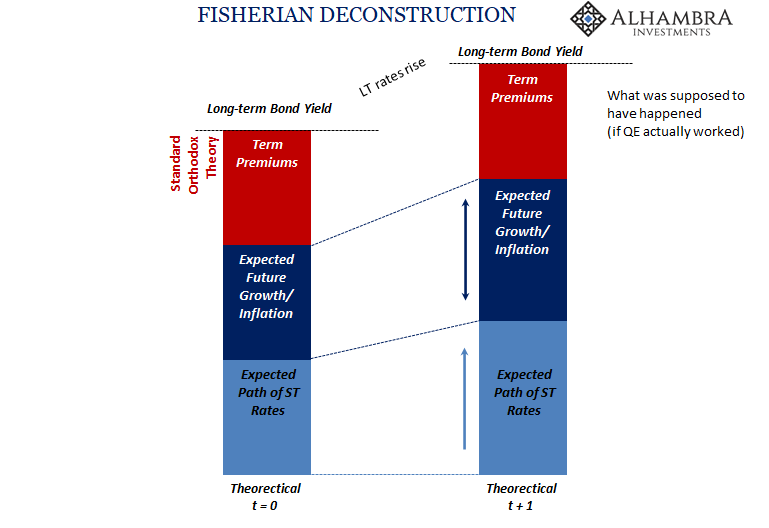

Good Time To Go Fish(er)ing Around The Yield Curve

Good Time To Go Fish(er)ing Around The Yield Curve

2022-01-21

It should be as simple as it sounds. Lower LT UST yields, less growth and inflation. Thus, higher LT UST yields, more growth and inflation. Right? If nominal levels are all there is to it, then simplicity rules the interpretation. Visiting with George Gammon last week, he confessed to committing this sin of omission.

This Is A Big One (no, it’s not clickbait)

This Is A Big One (no, it’s not clickbait)

2021-12-02

Stop me if you’ve heard this before: dollar up for reasons no one can explain; yield curve flattening dramatically resisting the BOND ROUT!!! everyone has said is inevitable; a very hawkish Fed increasingly certain about inflation risks; then, the eurodollar curve inverts which blasts Jay Powell’s dreamland in favor of the proper interpretation, deflation, of those first two.

Tags: Bonds,currencies,economy,Featured,Federal Reserve/Monetary Policy,FOMC,inflation,Markets,newsletter,rate hikes,supply chain,wholesale inventory,wholesale sales,Yield Curve,yield curve inversion