Someone once said that the stock market is always climbing a wall of worry. Maybe that had been true in some long-ago day, but whether or not it might nowadays is beside the point. The nugget of truth which makes the prosaism memorable is the wall rather than the climber. There’s always something going on somewhere to get worked up over. And it matters to far more than financial actors, the entire global economy must surmount what can seem like an unending series of events each one at certain times described as the most wicked and befouling disaster humanity has ever confronted. Such hyperbole, however, is applied only selectively to those times when the economy can’t seem to overcome these things. . When the system is humming along, or even just barely

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, currencies, economy, Featured, Federal Reserve/Monetary Policy, manufacturing, Markets, newsletter, services, U.S. ISM Manufacturing PMI, U.S. ISM Non-Manufacturing PMI

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Someone once said that the stock market is always climbing a wall of worry. Maybe that had been true in some long-ago day, but whether or not it might nowadays is beside the point. The nugget of truth which makes the prosaism memorable is the wall rather than the climber.

There’s always something going on somewhere to get worked up over. And it matters to far more than financial actors, the entire global economy must surmount what can seem like an unending series of events each one at certain times described as the most wicked and befouling disaster humanity has ever confronted. Such hyperbole, however, is applied only selectively to those times when the economy can’t seem to overcome these things. |

. |

| When the system is humming along, or even just barely reflating, the regular interjection of geopolitics is left in the background as nothing more than interesting noise.

Once downturn-ed, suddenly then every small event is the biggest thing ever. How else are we supposed to explain “unexpected” economic weakness that the mainstream constantly assures us isn’t legit weakness? Right now, for instance, Jay Powell says the US economy is in terrific shape, therefore it has to be Russia/Ukraine. After all, for being in an inarguably strong position, the biggest, most sophisticated markets in human history (with an actually enviable track record of making predictions and factoring reality) are quite vocal with the arguing. Before Russia, it was omicron. Remember omicron? The reason it barely recalls now is it wasn’t the disaster many said it would be. And yet, here we are further along that same path toward inversion, downturn, possibly worse. These “somethings” aren’t ever really the issue merely the latest stab at an excuse. |

. |

| Last week, the ISM reported more sobering numbers for the manufacturing sector. The real issue over here is inventory, a historical flood of which risks taking down the lone outlier for the entire global system. Early last year, Uncle Sam juiced up demand for online shopping, then, bam, the entire supply chain was overburdened.This was mistaken for a real, robust recovery particularly how it, like a classic supply shock case, showed up in the CPI.

We’re only since last October really starting to see by how much, and by how insane wholesalers and retailers had gone crazed with government mania. |

. |

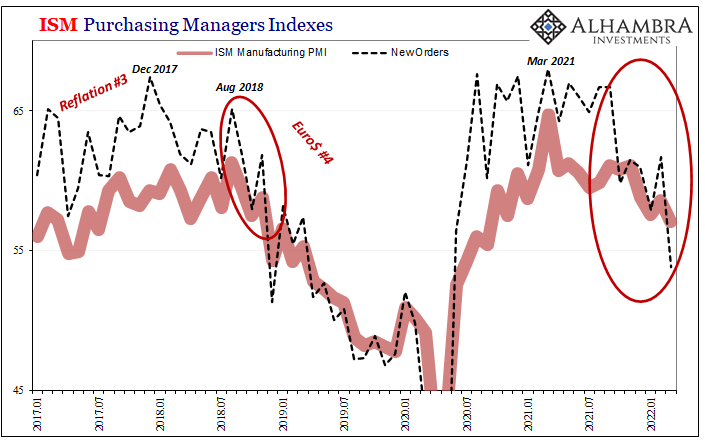

| According to the ISM’s estimates for March 2022, the headline index on manufacturing fell to 57.1 from 58.6 in February.

Even if you don’t fall for the Russia blame, these numbers just don’t sound bad whatsoever. Near 60? That’s pretty good, seems like the US is weathering whatever alarm-of-the-day rather well. Or is it? You take the ISM Manufacturing headline at 57.1 and then realize not only is it the lowest since September 2020, this continues a trend which month after month more and more resembles the wrong kind. The kind since October which falls into the same category as late 2018/early 2019. As if needs to be pointed out, that’s already not good and we’re only getting started. While there had been any number of geopolitical apologies offered back then, too (ah 2018, when it was only Korean missiles about to ignite WWIII instead of actual war; when always-chaotic Italian politics could allegedly be the cause of major global market upset), none of them were ever able to adequately account for what became a globally synchronized downturn. Here we are again in that same boat if with different geopolitics along for the ride. |

. |

| Where it begins to look more 2019 than 2018 is, for ISM’s Manufacturing, the all-important New Orders category (above). Lost in the shuffle of last Friday’s March payroll report was a rather sharp drop in this component, falling to 53.8 from 61.7.

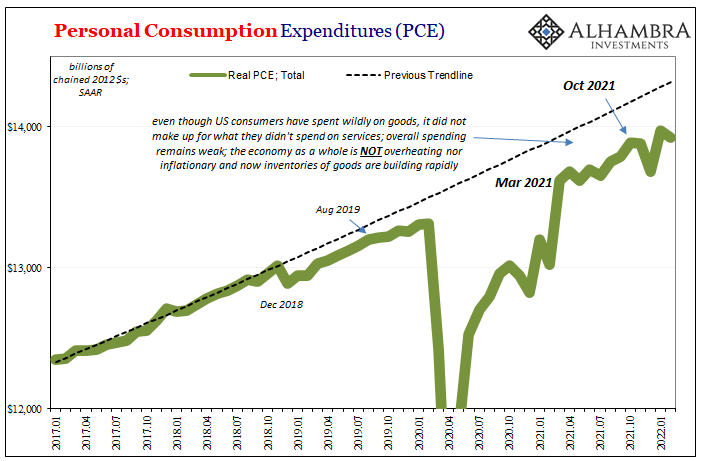

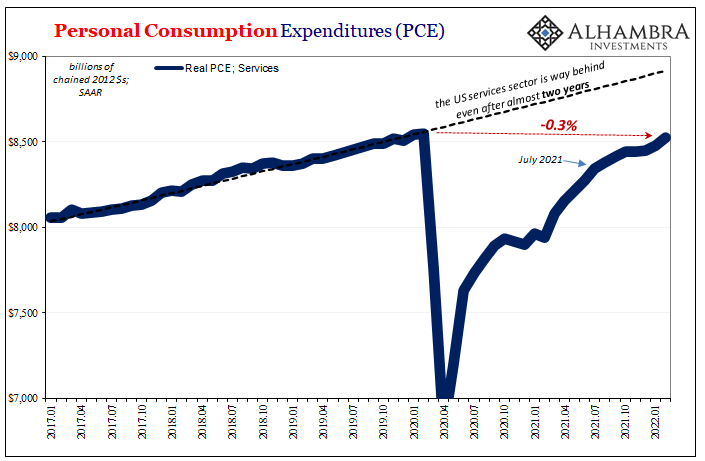

Again, 53.8, OK, big decline but still comfortably above 50. Yet, that’s the worst since May 2020, looking more like what was going on at that woeful time rather than inflationary hot with each noisy monthly release. Should anyone then flip over to services, the ISM today gives no comfort there, either. Typically, post-2008 world, the services sector had held up several times better in the face of what repeatedly became sharp “manufacturing recessions” one after another. In the post-2020 environment, as I stated above, manufacturing has been far and away the star with services left almost all the way out of it. Could the latter restore its own then the whole economy’s glory? That’s been offered by many as the next attempted explanation for what’s shaping up over in manufacturing (of course goods production is slowing, people are just normalizing, buying a few fewer goods after getting back out of the house again!) If this was the case, the ISM certainly doesn’t show it. On the contrary, while the numbers all rebounded in March from February lows, that they were so low in February to begin with and didn’t come back much in March hints at other problems beside omicron, Russia, or the lack of lockdowns. |

. |

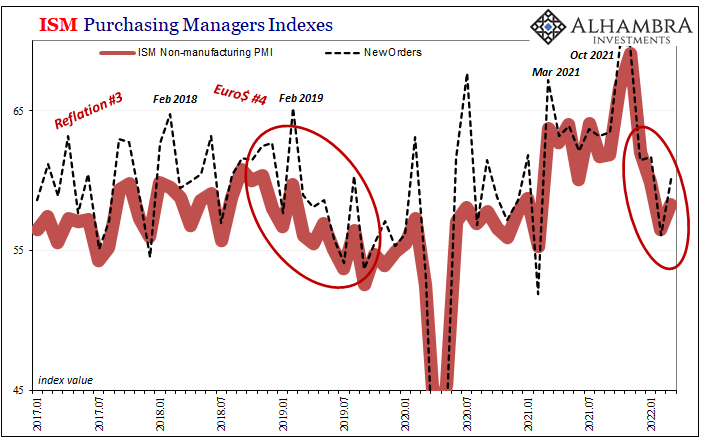

| The headline index was 58.3 last month, up from 56.5 during February. New orders reached 60.1 following 56.1 prior.

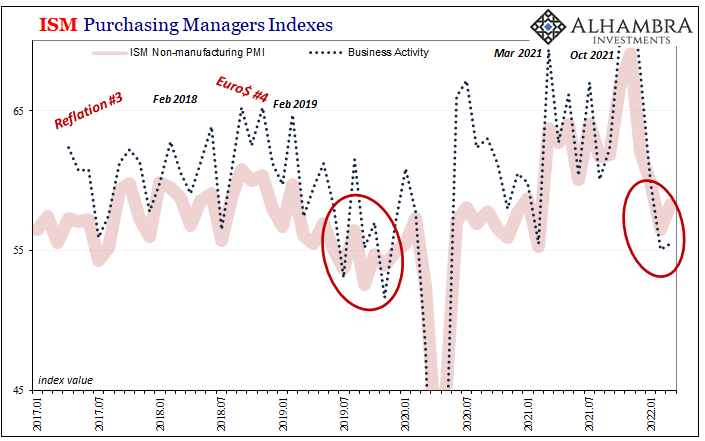

Once more, these sound pretty good if not borderline terrific. Yet, they are verging in on Summer 2019 comparisons. When the services sector is supposedly coming back up to save us from manufacturing slowdowns, these estimates are just around the same range as when, August 2019, yes, the 2s10s yield curve last inverted. That’s not all. Much of the seeming “terrificness” of the headline (either one) is due to factors and components beyond output and ordering. Prices have skewed the numbers as have dispersion surveys for things like backlogs. Judging by activity alone, in the ISM’s Non-manufacturing survey (above), services, sentiment surrounding output slightly worse than Summer 2019, edging now into the territory of later 2019 when much of the rest of the world economy had already begun to regularly (pre-COVID) feature negative GDP numbers. Setting aside recession or any worries over severity, 55.5 for Business Activity (following a 55.1) is just no good at all regardless of how it may at first sound. |

. |

| Is it the wall of worry? No. The same wall was in place last year just like it had been around in 2017 or 2014. The specific geopolitics change all the time because they happen all the time, ultimately what’s really left is the inevitable downside slide.

How far or fast it goes, well, that’s a matter for curve. |

. |

. |

You Might Also Like

SWIFT Isn’t The ‘Nuclear Option’ For Russia, Because Russia can sell the dollars elsewhere and NOT via Swift

SWIFT Isn’t The ‘Nuclear Option’ For Russia, Because Russia can sell the dollars elsewhere and NOT via Swift

2022-03-01

As everyone “knows”, the US dollar is the world’s reserve currency which can only leave the US government in control of it. Participation is both required and at the pleasure of American authorities. If you don’t accept their terms, you risk the death penalty: exile from the privilege of the US dollar’s essential business.From what little most people know about that essential business, it seems like it has something to do with that thing called SWIFT. Thus, Russia. In fact, the White House’s statement from a few days ago confirms these things. At least, it seems to confirm what most people already believe:

First, we commit to ensuring that selected Russian banks are removed from the SWIFT messaging system. This will ensure that these banks are disconnected from the international

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)

2022-01-16

How is that US Treasury rates out in the independent longer end of the yield curve have now “suffered” a seven percent CPI to go along with double taper and triple maybe quadruple (if the whispers are to be believed) rate hikes this year, yet have weathered all of that allegedly bond-busting brutality with barely a market fluctuation?

Start Long With The (long ago) End of Inflation

Start Long With The (long ago) End of Inflation

2021-12-24

With the eurodollar futures curve slightly inverted, the implications of it are somewhat specific to the features of that particular market. And there’s more than enough reason to reasonably suspect this development is more specifically deflationary money than more general economic concerns.

Testing The Supply Chain Inflation Hypothesis The Real Money Way

Testing The Supply Chain Inflation Hypothesis The Real Money Way

2021-12-18

Basic intuition says this is a no-brainer. Producer prices rise, businesses then pass along these higher input costs to their customers in the form of consumer price “inflation” so as to preserve profits. This is the supply chain hypothesis. Statistically, we’d therefore expect the PPI to lead the CPI.And this was expected for much of Economics’ history, taken for granted as one of those self-evident truths (kind of like the Inflation Fairy). After the dreadful experience of the Great Inflation, and the dreadful performance of Economics during it, a few scholars went back to take a second look.One of the most cited contrary studies was published in 1995 by Todd Clark of the Federal Reserve’s branch in Kansas City (Economic Review; vol. 80, issue Q III, 25-39). Using econometric evidence,

What Does Taper Look Like From The Inside? Not At All What You’d Think

What Does Taper Look Like From The Inside? Not At All What You’d Think

2021-11-05

Why always round numbers? Monetary policy targets in the post-Volcker era are changed on even terms. Alan Greenspan had his quarter-point fed funds moves. Ben Bernanke faced with crisis would auction $25 billion via TAF. QE’s are done in even numbers, either total purchases or their monthly pace.

Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?

Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?

2021-11-02

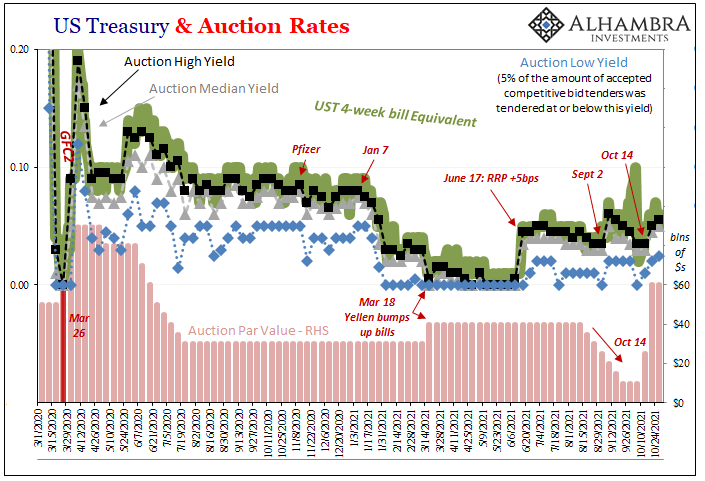

Treasury Secretary Janet Yellen hasn’t just been busy hawking cash management bills, her department has also been filling back up with the usual stuff, too. Regular T-bills. Going back to October 14, at the same time the CMB’s have been revived, so, too, have the 4-week and 13-week (3-month). Not the 8-week, though.

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited

The Enormously Important Reasons To Revisit The Revisions Already Several Times Revisited

2021-10-29

Extraordinary times call for extraordinary commitment. I never set out nor imagined that a quarter century after embarking on what I thought would be a career managing portfolios, researching markets, and picking investments, I’d instead have to spend a good amount of my time in the future taking apart how raw economic data is collected, tabulated, and then disseminated.

Far Longer And Deeper Than Just The Past Few Months

Far Longer And Deeper Than Just The Past Few Months

2021-10-20

Hurricane Ida swept up the Gulf of Mexico and slammed into the Louisiana coastline on August 29. The storm would continue to wreak havoc even as it weakened the further inland it traversed. By September 1 and 2, the system was still causing damage and disruption into the Northeast of the United States.

Tags: Bonds,currencies,economy,Featured,Federal Reserve/Monetary Policy,manufacturing,Markets,newsletter,services,U.S. ISM Manufacturing PMI,U.S. ISM Non-Manufacturing PMI