A nod to just how backward and upside down the world is now. The economic data everyone is made to pay attention to, payrolls, that one is, in my view, irrelevant. As is the consumer price estimates from earlier this week, the PCE Deflator. That’s another one which receives vast amounts of interest even though it is already old news. Yet, in the very same data release as the PCE, some other accounts importantly tied to labor, personal income, they slip unnoticed under the radar even though what they show is far more meaningful than either of the above. . We’re focused entirely on those that don’t matter and miss the one(s) which does. . By “we”, I mean, of course, mainstream analysis and commentary, modern day Economics. The bond market isn’t fooled. Not only

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, currencies, economy, Featured, Federal Reserve/Monetary Policy, inflation, Markets, newsletter, PCE, Personal Income, personal spending, real personal income excluding transfer receipts, Recession, U.S. Treasuries, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| A nod to just how backward and upside down the world is now. The economic data everyone is made to pay attention to, payrolls, that one is, in my view, irrelevant. As is the consumer price estimates from earlier this week, the PCE Deflator. That’s another one which receives vast amounts of interest even though it is already old news.

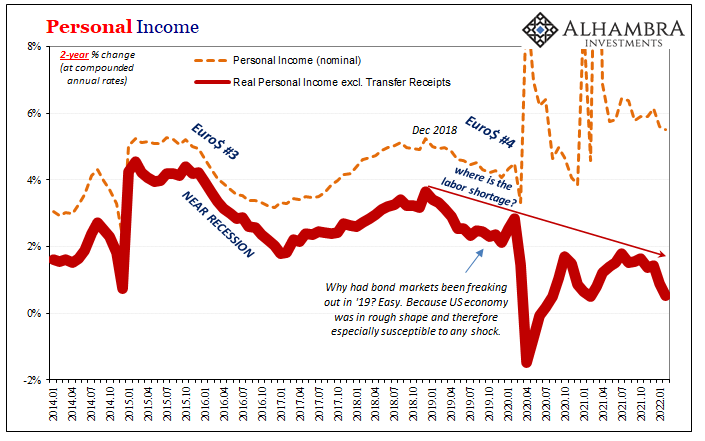

Yet, in the very same data release as the PCE, some other accounts importantly tied to labor, personal income, they slip unnoticed under the radar even though what they show is far more meaningful than either of the above. |

. |

| We’re focused entirely on those that don’t matter and miss the one(s) which does. |

. |

| By “we”, I mean, of course, mainstream analysis and commentary, modern day Economics. The bond market isn’t fooled.

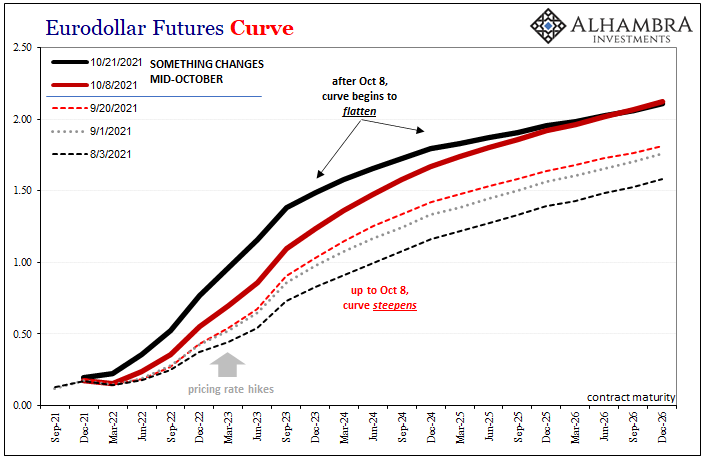

Not only do we have the inventory flood arriving in October to bolster the macro case for curves (along with the real money, collateral case), there’s maybe more importantly an income claim to such rapidly gaining pessimism, too. |

. |

| Like inventory, it has also to do with the supply shock effect.

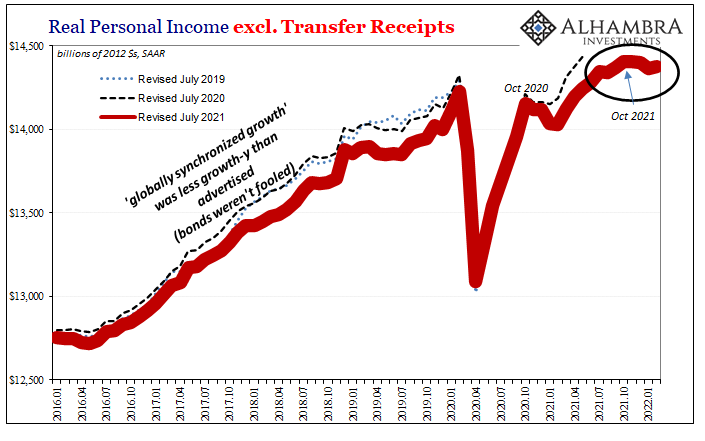

More Americans are working, as the payroll reports show, and more earned income is being generated, yet it’s not enough to keep up with the artificial surge in prices. According to the BEA, Real Personal Income excluding Transfer Receipts has declined since…October. A string of negative months in this same account is used by the NBER to help declare recessions. |

. |

. |

|

. |

|

| Pay more, get less. Get paid more, it buys less.

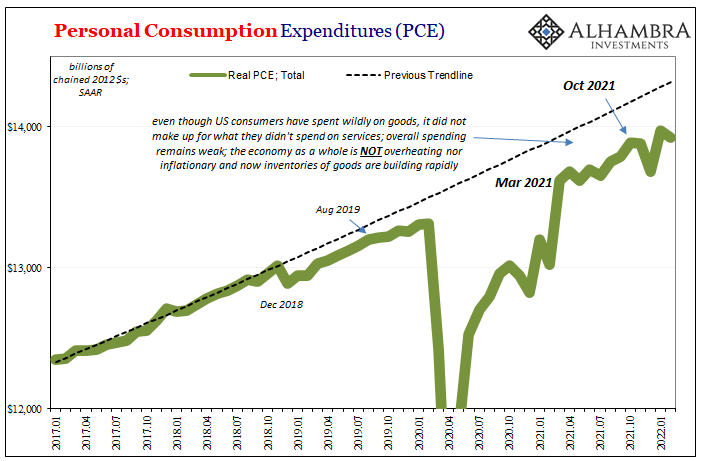

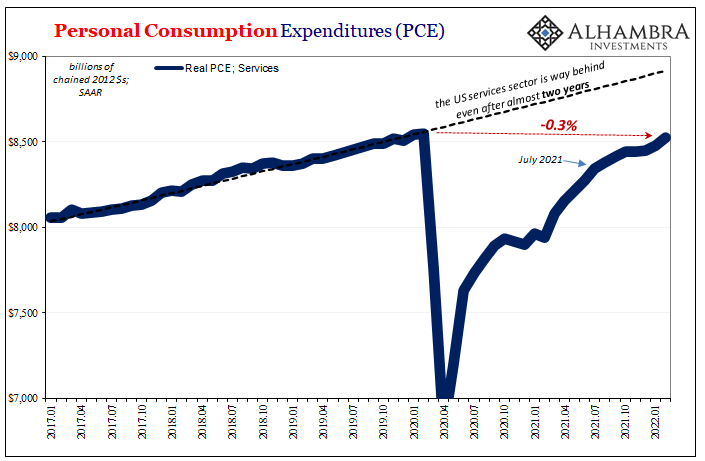

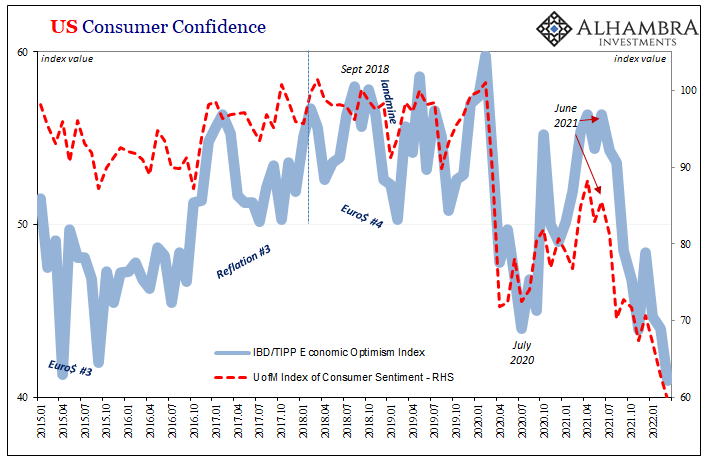

Simple relationships which form the basis for demand destruction. And it only takes some time before the second order effects begin to overshadow those first. As the inability to keep up with especially oil prices (gasoline) wears on discretionary spending, it begins to have a psychological impact, too. Not only do consumers as workers fall further behind, they compound the problem in macro terms by cutting back – destroying demand – as they themselves grow understandably angry and increasingly cautious. |

. |

. |

|

. |

|

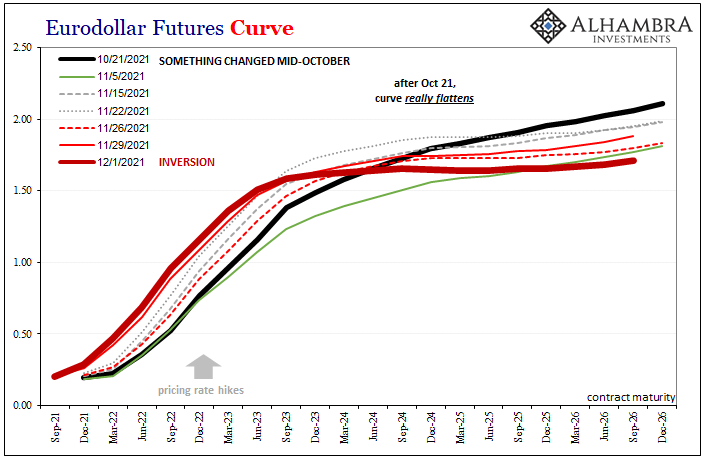

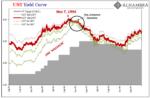

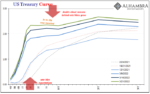

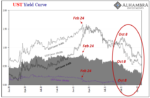

| In that sense, we’ve already seen the second order really begin to bloom.

With that sort of economic backdrop, flattening and now inverted curves well into their historic recession watch only make sense. The Fed and its rate hike panic does not. In grounded markets, logic and honest assessment are more than a requirement. In the puppet theater of non-money monetary policy, irrationality is practically invited. |

. |

You Might Also Like

We Can Only Hope For Another (bond) Massacre

We Can Only Hope For Another (bond) Massacre

2022-03-30

To begin with, the economy today is absolutely nothing like it had been almost thirty years ago. That fact in and of itself should end the discussion right here. However, comparisons will be made and it does no harm to review them.I’m talking about 1994, or, more specifically, the eleven months between late February 1994 and early February 1995.

Inversion Is The Real March Madness, Just Don’t Take It Literally

Inversion Is The Real March Madness, Just Don’t Take It Literally

2022-03-22

With such low levels of self-awareness, it isn’t surprising that the FOMC’s members continue to pour gasoline on the already-blazing curve fire. March Madness is supposed to be on the courts of college basketball, instead it is playing out more vividly across all financial markets.

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

2022-01-28

It’s not hard to reason why there continues to be this conflict of interest (rates). On the one hand, impacting the short end of the yield curve, the unemployment rate has taken a tight grip on the FOMC’s limited imagination. The rate hikes are coming and the markets like all mainstream commentary agree that as it stands there’s nothing on the horizon to stop Jay Powell’s hawkishness.

Good Time To Go Fish(er)ing Around The Yield Curve

Good Time To Go Fish(er)ing Around The Yield Curve

2022-01-21

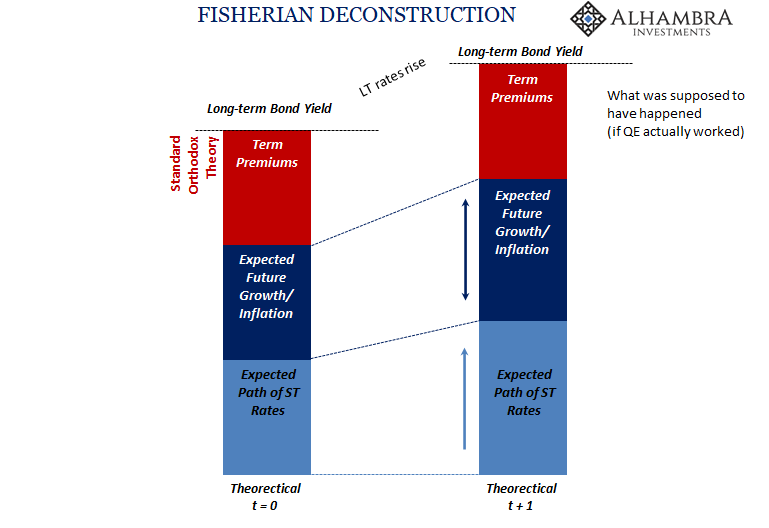

It should be as simple as it sounds. Lower LT UST yields, less growth and inflation. Thus, higher LT UST yields, more growth and inflation. Right? If nominal levels are all there is to it, then simplicity rules the interpretation. Visiting with George Gammon last week, he confessed to committing this sin of omission.

Conflict Of Interest (rates): 10-year Treasury Yield Highest in Almost Two Years

Conflict Of Interest (rates): 10-year Treasury Yield Highest in Almost Two Years

2022-01-12

The dollar was high and going higher. Emerging markets had been seriously complaining. In one, the top central banker for India outright warned, “dollar funding has evaporated.” The TIC data supported his view, with full-blown negative months, net selling from afar that’s historically akin to what was coming out of India and the rest of the world.

White-Hot Cycles of Silence

White-Hot Cycles of Silence

2021-12-28

We’re only ever given the two options: the economy is either in recession, or it isn’t. And if “not”, then we’re led to believe it must be in recovery if not outright booming already. These are what Economics says is the business cycle. A full absence of unit roots. No gray areas to explore the sudden arrival of only deeply unsatisfactory “booms.”

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century

2021-12-22

Have oil producers shot themselves in the foot, while at the same time stabbing the global economy in the back? It’d be quite a feat if it turns out to be the case, one of those historical oddities that when anyone might honestly look back on it from the future still hung in disbelief. Let’s start by reviewing just the facts.

An Anti-Inflation Trio From Three Years Ago

An Anti-Inflation Trio From Three Years Ago

2021-10-26

Do the similarities outweigh the differences? We better hope not. There is a lot about 2021 that is shaping up in the same way as 2018 had (with a splash of 2013 thrown in for disgust). Guaranteed inflation, interest rates have nowhere to go but up, and a certified rocking recovery restoring worldwide potential.

Tags: Bonds,currencies,economy,Featured,Federal Reserve/Monetary Policy,inflation,Markets,newsletter,PCE,Personal Income,personal spending,real personal income excluding transfer receipts,recession,U.S. Treasuries,Yield Curve