This isn’t going to be like the tale of Goldilocks, at least not how it’s usually told. There are three central banks, sure, call them bears if you wish, each pursuing a different set of fuzzy policies. One is clearly hot, the other quite cold, the final almost certainly won’t be “just right.” Rather, this one in the middle simply finds itself…in the middle of the other two. Running red-hot to the point of near-horror, that’s “our” Federal Reserve. The FOMC minutes from last month’s rate hike meeting were published today, not that anyone needed any addition to the ongoing jawboning. Speeches and appearances by any of the FOMC between then and now have clearly indicated just how uncomfortable policymakers have become about the CPI (or PCE Deflator, if you prefer,

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, China, Christine Lagarde, currencies, ECB, economy, Europe, Featured, Federal Reserve/Monetary Policy, FOMC, Markets, newsletter, PBOC, QE, rate cuts, rate hikes, tapering, yi gang

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| This isn’t going to be like the tale of Goldilocks, at least not how it’s usually told. There are three central banks, sure, call them bears if you wish, each pursuing a different set of fuzzy policies. One is clearly hot, the other quite cold, the final almost certainly won’t be “just right.” Rather, this one in the middle simply finds itself…in the middle of the other two.

Running red-hot to the point of near-horror, that’s “our” Federal Reserve. The FOMC minutes from last month’s rate hike meeting were published today, not that anyone needed any addition to the ongoing jawboning. Speeches and appearances by any of the FOMC between then and now have clearly indicated just how uncomfortable policymakers have become about the CPI (or PCE Deflator, if you prefer, like they do). Pure political theater, the word used in the minutes was “expeditiously.” In other words, the committee members want to get the fed funds range up to what they consider “neutral” (whatever that might be; it is defined as a theoretical rate neither tight nor accommodative, so it won’t contribute more to “inflation” assuming rates actually matter in this way; they don’t) as fast as possible. |

. |

| To that demand, the minutes also wrote how “many participants” would have preferred a double to kick things off last month, a fifty hike rather than the typical, stoic twenty-five, and that “many participants” clearly prefer a few fifties moving expeditiously forward.

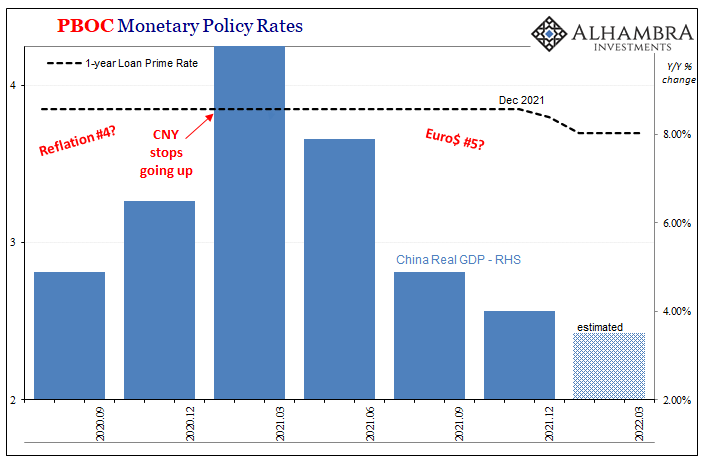

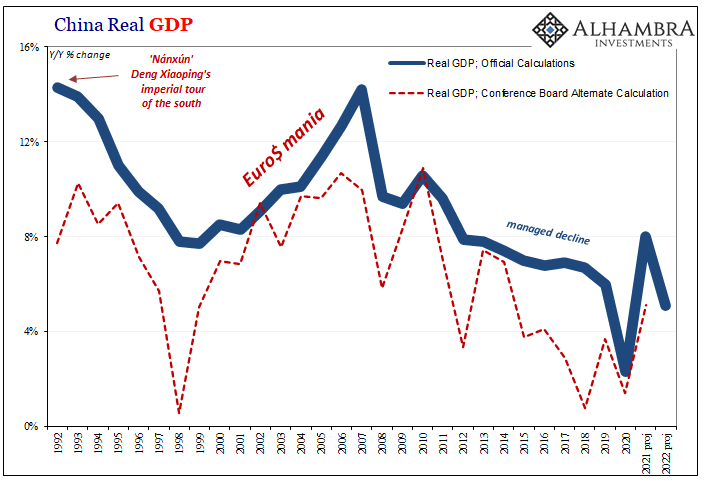

While the Federal Reserve is scorching with rate hiking, consumer price theater, their Chinese counterparts are chilling down freezing cold. The PBOC may have paused for both February and March, yet everyone (including those at the PBOC) expects already prior rate cuts (December and January) to resume later this month. |

. |

| China’s economy is wrestling with more than draconian, frankly dystopian zero-COVID insanity. While that isn’t helping, and might explain the depths of temporary downside monthly data, far more alarming is the trend which remains unbroken to the upside even after whichever latest variant (and lockdowns) passes meekly through history.

In between the PBOC and the Fed, our friends over in Europe. This one’s even more compelling if not weird because European consumer prices accelerated to 7.5% year-over-year (preliminary) for March 2022, which, you’ll note, is practically the same pace for US prices. However, unlike the Powell panic, Christine Lagarde’s ECB continues to play it rather cool. |

. |

| Officials there have steadfastly claimed rate hikes will not begin until the QEs are wound completely down to nothing, which will take several months more.

And even when those done and gone, Lagarde also has repeatedly stated how her hikes may not start up immediately after the asset purchasing ends. On top of that, she also purposefully dropped the word “gradual” several more times, meaning that once European rate hikes do begin (if ever) they will not proceed expeditiously. Three central banks, each moving forward in separate ways. Only one global economy. |

. |

| Meaning, that there aren’t separate scenarios (decoupling) where all three do the “right” thing, each one best responding to individual and isolated idiosyncratic circumstances, rather it is an either/or situation that, like 2018-19, is bound to get synchronized in one way or the other.

Will it be the way the Fed is leaning, rate hikes taming sustained red hot consumer prices leading to the, um, Goldilocks soft landing? Or the PBOC, where rate cuts are increasingly seen even by mainstream cheerleaders as truly warranted if only to keep that part of the global system from tanking any further than it already has (see: recent PMIs, including Caixin)? How about the ECB and Ms. |

. |

| Lagarde’s more determined cautiousness which isn’t all Russian spillover?

For the latter pair, there is the lesson of 2018 to begin with. Mario Draghi, Lagarde’s immediate predecessor, you might recall his huge error when from the start of that year he dismissed growing weakness (in Europe as well as China) as nothing more than an immaterial slowdown from a rapid high in 2017. It did not work out well for him, or, you know, Europe and the rest of the world. Rather importantly, it also didn’t go very well at all for one Jay Powell. It might be that Christine unlike Mario is more attuned to not just that mistake but also how it could’ve been avoided by paying much closer attention to what was going on in China and with the PBOC’s interpretation of risks and tendencies rather than sticking closely by the uncontroversial mainstream-ness of Powell and the Fed. Given how much China directly affects Europe, far more than Russia (in broad macro terms, outside of energy, yes), you have to wonder just how much of a wary eye the ECB is keeping on the Far East rather than the rest of the West’s inflation clutching. |

. |

. |

|

. |

|

| Also, markets. A whole lot of markets.

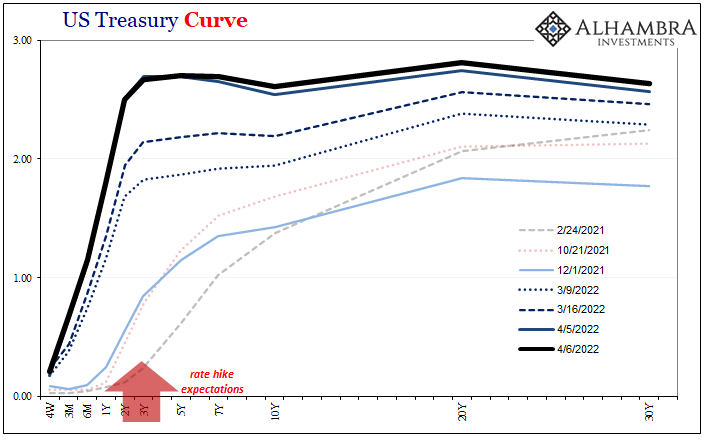

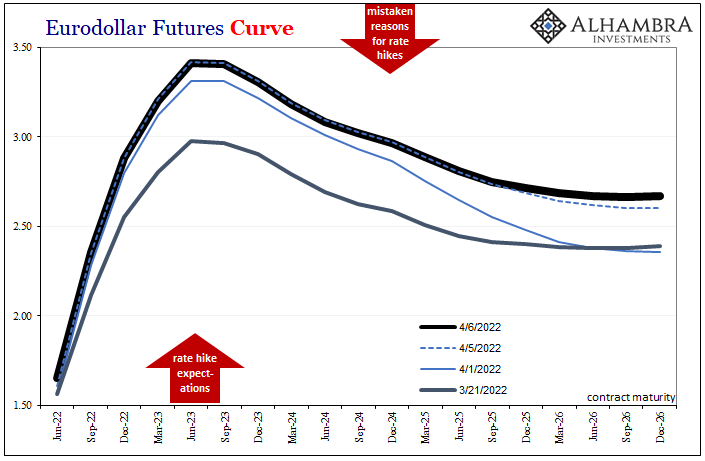

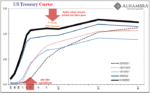

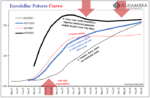

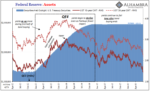

Despite rate hikes from the Fed and the confidence in the economy expressed by them, inversions all over. Deep, profound ugliness, the upside-down which, it should go without saying, isn’t anywhere close to the Goldilocks story (see: below; special attention to bills and fails which I’ll write more about tomorrow). Jay Powell’s doing his thing, Lagarde hers, and China’s Yi Gang totally opposite either. What a fascinating series of confused conundrums. Markets are far more with China, even the big one over in Europe. |

. |

| Goldilocks this time, like last time and the prior times, might just find the “right” answer is, in fact, still too cold. |

. |

. |

You Might Also Like

It Wouldn’t Be TIC Without So Much Other

It Wouldn’t Be TIC Without So Much Other

2022-03-23

With the Fed (sadly) taking center stage last week, and market rejections of its rate hikes at the forefront, lost in the drama was January 2022 TIC. Understandable, given all its misunderstood numbers are two months behind at their release. There were some interesting developments regardless, and a couple of longer run parts that deserve some attention.

Inversion Is The Real March Madness, Just Don’t Take It Literally

Inversion Is The Real March Madness, Just Don’t Take It Literally

2022-03-22

With such low levels of self-awareness, it isn’t surprising that the FOMC’s members continue to pour gasoline on the already-blazing curve fire. March Madness is supposed to be on the courts of college basketball, instead it is playing out more vividly across all financial markets.

Media Attention All Over FOMC, Market Attention Totally Elsewhere

Media Attention All Over FOMC, Market Attention Totally Elsewhere

2022-03-19

The Federal Reserve did something today, or actually announced today that it will do something as of tomorrow. And since we’re all conditioned to believe this is the biggest thing ever, I’ll have to add my own $0.02 (in eurodollars, of course, can’t be bank reserves) frustratingly contributing to the very ritual I’m committed to seeing end.We shouldn’t care much about the Fed.

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed

2022-03-16

This week will almost certainly end up as a clash of competing interest rate policy views. Everyone knows about the Federal Reserve’s upcoming, the beginning of what is intended to be a determined inflation-fighting campaign for a US economy that American policymakers worry has been overheated.

The Red Warning

The Red Warning

2022-02-24

Now it’s the Russian’s fault. Belligerence surrounding Donbas and Ukraine, raw materials and energy supplies to Europe threatened by Putin’s coiled bear. Why wouldn’t markets grow worried?There’s always a reason why we shouldn’t take these things seriously, or quickly dismiss them out of hand as the temporary product of whichever political fear-of-the-day.

The Hawks Circle Here, The Doves Win There

The Hawks Circle Here, The Doves Win There

2022-01-26

We’ve been here before, near exactly here. On this side of the Pacific Ocean, in the US particularly the situation was said to be just grand. The economy was responding nicely to QE’s 3 and 4 (yes, there were four of them by that point), Federal Reserve Chairman Ben Bernanke had said in the middle of 2013 it was becoming more than enough, creating for him and the FOMC coveted breathing space so as to begin tapering both of those ongoing programs.A full and complete recovery he believed was on schedule if not getting way ahead of it.

Taper Rejection: Mao Back On China’s Front Page

Taper Rejection: Mao Back On China’s Front Page

2021-12-29

Chinese run media, the Global Times, blatantly tweeted an homage to China’s late leader Mao Zedong commemorating his 128th birthday. Fully understanding the storm of controversy this would create, with the Communist government’s full approval, such a provocation has been taken in the West as if just one more chess piece played in its geopolitical game against the United States in particular.No. The Communists really mean it. Mao’s their guy again.

No. Let's recall that Chairman Mao• slaughtered thousands of his political adversaries in early 1930s• exterminated hundreds of thousands of landlords in early 1950s• starved 45 million peasants to death in Great Leap Forward• murdered 2 million in the Cultural Revolution— TheSeeqer (@TheSeeqer) December 26, 2021

When Deng Xiaoping

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

2021-11-03

Bring on the tantrum. Forget this prevaricating, we should want and expect interest rates to get on with normalizing. It’s been a long time, verging to the insanity of a decade and a half already that keeps trending more downward through time. What’s the holdup?

Tags: Bonds,China,Christine Lagarde,currencies,ECB,economy,Europe,Featured,Federal Reserve/Monetary Policy,FOMC,Markets,newsletter,PBOC,QE,rate cuts,rate hikes,tapering,yi gang