Swiss Economicblogs.org

Swiss Economicblogs.org

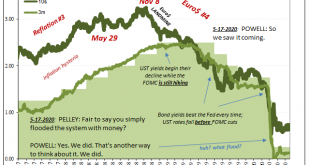

Have we entered a new bull market? Was the 35% pullback in the S&P 500 in March the fastest bear market in history? Or is this just a continuation of the bull market that started in 2009, interrupted by a rather large correction? Bull markets and bear markets are about behavior, about the human emotions of fear and greed. While we got a brief bout of fear in March, greed has since overwhelmed all sense, common and otherwise. What we’re seeing in the casino…er,...

Read More »We Have Reached The Silly Phase of the Bull Market