The missing piece so far is consumers. We’ve gotten a glimpse at how businesses are taking in the shock, both shocks, actually, in that corporations are battening down the liquidity hatches at all possible speed and excess. Not a good sign, especially as it provides some insight into why jobless claims (as the only employment data we have for beyond March) have kept up at a 2mm pace. These are second order effects. In terms of consumer spending, it’s, as always, spend versus save. Are consumers going to change their behavior, too? If the propensity to spend was one level before March, will it be at a lesser rate once the non-economic dislocation passes by? If so, that will cause and amplify further not-short run economic damage. That’s how exogenous shocks like

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, CARES Act, consumer spending, currencies, economy, Featured, Federal Reserve/Monetary Policy, Markets, newsletter, PCE, Personal Consumption Expenditures, Personal Income, personal savings rate, real personal consumption expenditures, real personal income excluding transfer receipts, transfer payments

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

The missing piece so far is consumers. We’ve gotten a glimpse at how businesses are taking in the shock, both shocks, actually, in that corporations are battening down the liquidity hatches at all possible speed and excess. Not a good sign, especially as it provides some insight into why jobless claims (as the only employment data we have for beyond March) have kept up at a 2mm pace. These are second order effects. In terms of consumer spending, it’s, as always, spend versus save. Are consumers going to change their behavior, too? If the propensity to spend was one level before March, will it be at a lesser rate once the non-economic dislocation passes by? If so, that will cause and amplify further not-short run economic damage. That’s how exogenous shocks like COVID-19 become far more than the incidental damage they cause. |

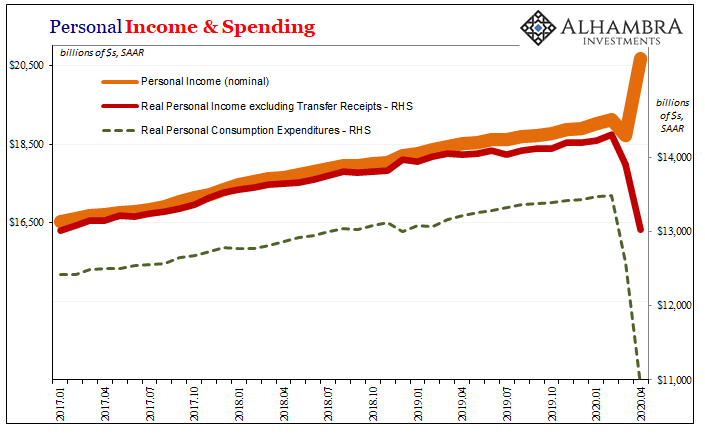

Personal Income & Spending, 2017-2020 - Click to enlarge |

| The lingering demand destruction is brought about by changes in how everyone in it behaves – if there are any.

Right now, the mainstream assumption is for the biggest and best “V”; that once the economy reopens everything will go right back to the way it was before anyone had heard of the coronavirus. Furthermore, the government’s recklessness in fiscal as well as monetary matters is being viewed as more than sufficient insurance so as to make this likely. Again, so far the business side isn’t on the government’s side (including Jay Powell). The BEA today published its April estimates for personal income and spending – the consumer end of the economy. As with everything else to this point, the first step into the crisis has been a disaster though I’ll qualify this straight away by noting we shouldn’t put too much stock into this one month of data. For one thing, April is completely out of the ordinary, a true outlier month especially for consumers if ever there was one. Second, the government’s transfer payments had just started showing up. What these figures show is that Americans were finally getting paid on their unemployment claims as well as “helicopter” money though they didn’t spend much or any of it.The difference between the surging orange line above (nominal personal income) compared to the falling red line (real income) just below it is all that “stimulus” money. And though it was pushed up by an unprecedented $2.1 trillion last month, that’s at a seasonally-adjusted annual rate. In actual dollars, the monthly level for transfer payments was far less. In fact, as you can see above, these preliminary assessments suggest spending was down way more than earned income fell. This pushed the personal savings rate to exactly one-third, or 33%; essentially meaningless. |

Real Personal Income, 1960-2020 - Click to enlarge |

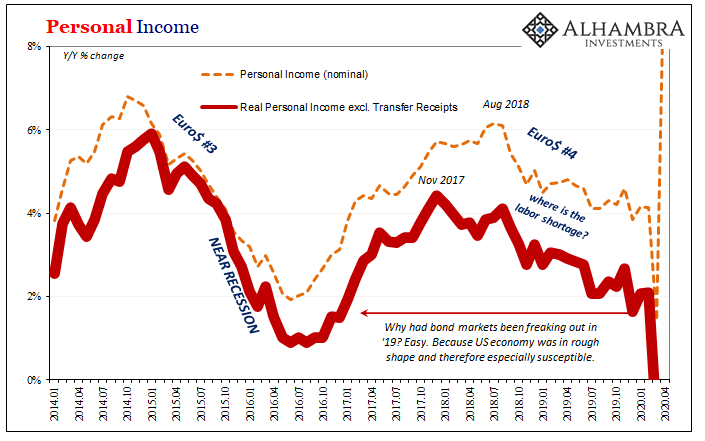

| To put this in perspective, the 7.2% year-over-year decline in non-transfer income was the largest on record for a series that dates back sixty years. |

Personal Income, 2014-2020 - Click to enlarge |

| And what that series had already shown before March 2020 was a labor market being slowly squeezed by a globally synchronized downturn that had left the US economy in very susceptible shape long before the pandemic arrived. It’s been my view that this will make a difference going forward even as the reopening takes place.

These figures for April are dishearteningly consistent with this position, though, again, there’s no hard conclusions yet to be drawn from just this one month.

I’m *very* much in favor of helping American workers and even doing so in this way; by all means, send out the $1,000 checks. What I’m very much against is the idea that it will do much systemic good.https://t.co/9WEsjK8H96— Jeffrey P. Snider (@JeffSnider_AIP) March 17, 2020 |

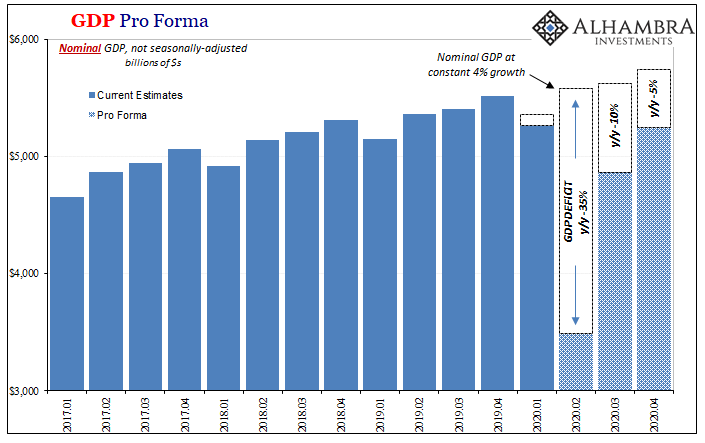

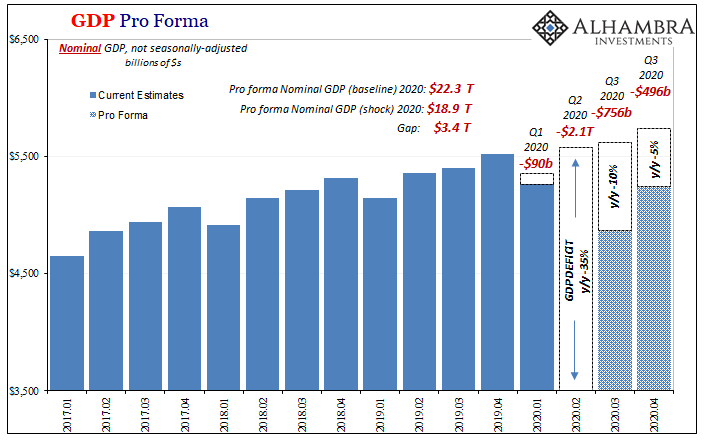

GDP Pro Forma, 1984-2020 - Click to enlarge |

| It is possible perhaps likely that a lot of the “stimulus” money does end up being spent – if it hasn’t already been during the month of May. But then the question becomes one of lost income versus these transfer receipts. The size of the income hole compared to the government’s direct aid (it’s not stimulus) intending to redistribute money since the economy isn’t.

While we wait for more data over the coming months to confirm or deny this prospect, on just plain common-sense terms it’s hard to see how consumers (like businesses) aren’t going to be changed by what’s happened. In fact, it’s very likely why even the optimists aren’t really all the optimistic about the economy going forward. The major econometric models might be giving “stimulus” too much credit, perhaps way too much, but even then they still end up with a situation that can’t be properly called a “V.” Why?

It’s not conclusive by any means, but this is more preliminary evidence that 2020 isn’t going to be different this time. “L”, in other words. My “gap” calculations (below) are so far proving to be too generous. |

GDP Pro Forma, 2017-2020 - Click to enlarge |

GDP Pro Forma, 2017-2020 - Click to enlarge |

You Might Also Like

Three Straight Quarters of 2 percent, And Yet Each One Very Different

Three Straight Quarters of 2 percent, And Yet Each One Very Different

Headline GDP growth during the fourth quarter of 2019 was 2.05849% (continuously compounded annual rate), slightly lower than the (revised) 2.08169% during Q3. For the year, the Bureau of Economic Analysis (BEA) puts total real output at $19.07 trillion, or annual growth of 2.33% and down from 2.93% in 2018. Last year was weaker than 2017, the second lowest out of the six since 2013.

GDP + GFC = Fragile

GDP + GFC = Fragile

March 15 was when it all began to come down. Not the stock market; that had been in freefall already, beset by the rolling destruction of fire sale liquidations emanating out of the repo market (collateral side first). No matter what the Federal Reserve did or announced, there was no stopping the runaway devastation.

We All Know Who’s On First, But What’s On Second?

We All Know Who’s On First, But What’s On Second?

It wasn’t entirely unexpected, though when it was announced it was still quite a lot to take in. On September 1, 2005, the Bureau of Economic Analysis (BEA) reported that the nation’s personal savings rate had turned negative during the month of July. The press release announcing the number, in trying to explain the result was reduced instead to a tautology, “The negative personal saving reflects personal outlays that exceed disposable personal income.

Getting A Sense of the Economy’s Current Hole and How the Government’s Measures To Fill It (Don’t) Add Up

Getting A Sense of the Economy’s Current Hole and How the Government’s Measures To Fill It (Don’t) Add Up

The numbers just don’t add up. Even if you treat this stuff on the most charitable of terms, dollar for dollar, way too much of the hole almost certainly remains unfilled. That’s the thing about “stimulus” talk; for one thing, people seem to be viewing it as some kind of addition without thinking it all the way through first.You have to begin by sizing up the gross economic deficit it is being haphazardly poured into – with an additional emphasis on “haphazardly.”

If The Best Case For Consumer Christmas Is That It Started Off In The Wrong Month…

If The Best Case For Consumer Christmas Is That It Started Off In The Wrong Month…

Gone are the days when Black Friday dominated the retail calendar. While it used to be a somewhat fun way to kick off the holiday shopping season, it had morphed into something else entirely in later years. Scenes of angry shoppers smashing each other over the few big deals stores would truly offer, internet clips of crying children watching in horror as their parents transformed their local Walmart into Thunderdome.

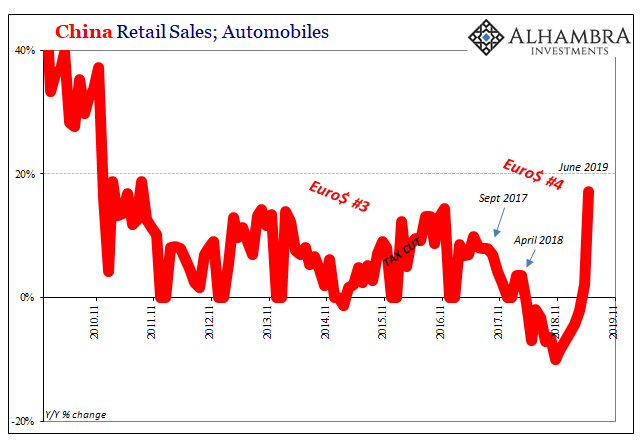

China Data: Something New, or Just The Latest Scheduled Acceleration?

China Data: Something New, or Just The Latest Scheduled Acceleration?

The Chinese government was serious about imposing pollution controls on its vast stock of automobiles. The largest market in the world for cars and trucks, the net result of China’s “miracle” years of eurodollar-financed modernization, for the Chinese people living in its huge cities the non-economic costs are, unlike the air, immediately clear each and every day.

China Enters 2020 Still (Intent On) Managing Its Decline

China Enters 2020 Still (Intent On) Managing Its Decline

Chinese Industrial Production accelerated further in December 2019, rising 6.9% year-over-year according to today’s estimates from China’s National Bureau of Statistics (NBS). That was a full percentage point above consensus. IP had bottomed out right in August at a record low 4.4%, and then, just as this wave of renewed optimism swept the world, it has rebounded alongside it.

No Flight To Recognize Shortage

No Flight To Recognize Shortage

If there’s been one small measure of progress, and a needed one, it has been the mainstream finally pushing commentary into the right category. Back in ’08, during the worst of GFC1 you’d hear it all described as “flight to safety.” That, however, didn’t correctly connote the real nature of what was behind the global economy’s dramatic wreckage. Flight to safety, whether Treasuries or dollars, wasn’t it.

Tags: CARES Act,consumer spending,currencies,economy,Featured,Federal Reserve/Monetary Policy,Markets,newsletter,PCE,personal consumption expenditures,Personal Income,personal savings rate,real personal consumption expenditures,real personal income excluding transfer receipts,transfer payments