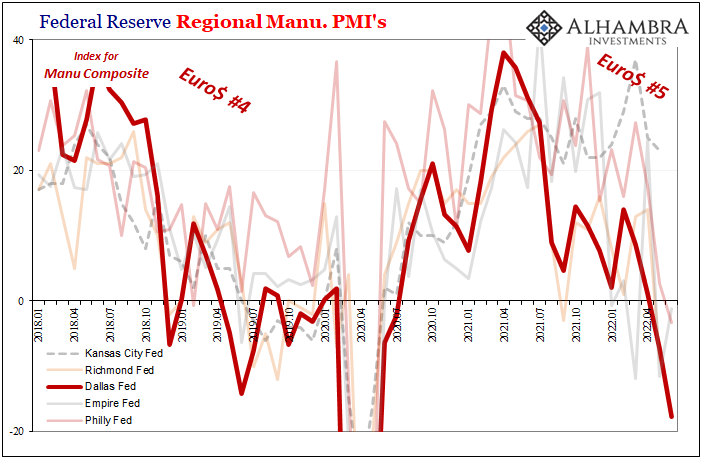

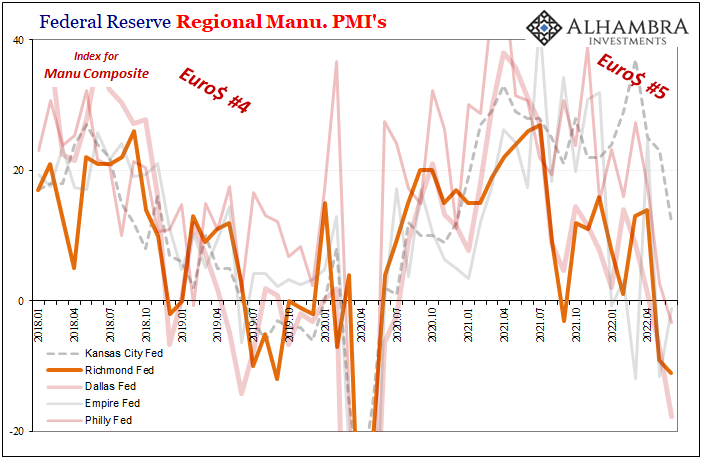

Well, that was a mess. The Richmond Fed’s Manufacturing Survey was at first released before being taken back. Initially reported as a plunge in the headline number, it was quickly scrapped once the statisticians remembered they had just discontinued their average workweek component – but had kept a zero in its place when tallying the overall PMI. With it, the PMI was originally calculated to have gone from bad in May (-9) to horrible in June (-19). Refiguring the whole thing for what today are now fewer inputs, the good folks in Richmond confidently say the corrected number is “merely” -11. Talk about exceeding radically lowered expectations. It wasn’t the case, however, where it counts the most going forward. . As always, new orders. Unaffected by the litany of

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, Consumer Confidence, currencies, economy, Featured, Federal Reserve/Monetary Policy, manufacturing, Markets, new orders, newsletter, Recession

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Well, that was a mess. The Richmond Fed’s Manufacturing Survey was at first released before being taken back. Initially reported as a plunge in the headline number, it was quickly scrapped once the statisticians remembered they had just discontinued their average workweek component – but had kept a zero in its place when tallying the overall PMI.

With it, the PMI was originally calculated to have gone from bad in May (-9) to horrible in June (-19). Refiguring the whole thing for what today are now fewer inputs, the good folks in Richmond confidently say the corrected number is “merely” -11. Talk about exceeding radically lowered expectations. It wasn’t the case, however, where it counts the most going forward. |

. |

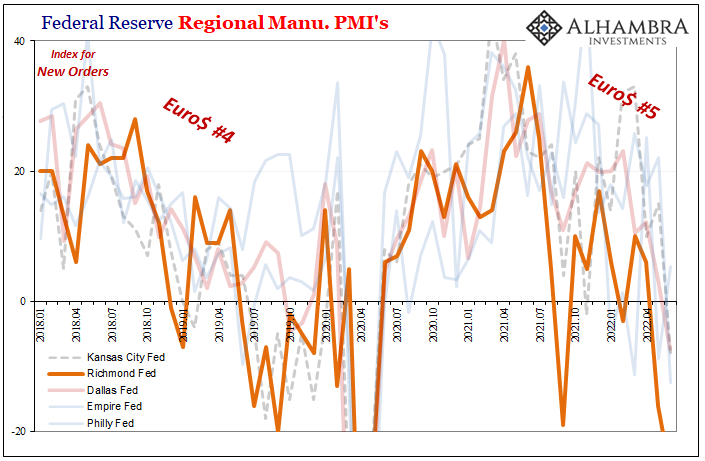

| As always, new orders. Unaffected by the litany of bad computations above, Richmond’s New Orders index actually did collapse – and from an already-awful level in May.

These June figures took last month’s worst-in-our-survey -16 and dropped another ten from it for this month; a blatantly recession-is-here -26 and right off my chart (third one below, following first a corrected-Dallas Fed from yesterday – Richmond isn’t the only place for mistakes – which wasn’t updated to the way-worse June estimate). |

. |

. |

|

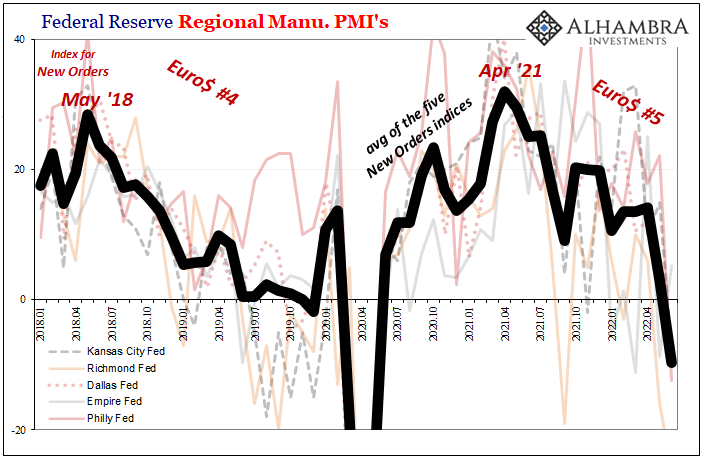

| As a result of all these changes and newly issued estimates, the headline average for the five surveys we follow sunk to -4.2. It’s only going to get much worse from here given forward-looking orders, with an average for those across the quintet a decidedly atrocious -9.7.

That’s significantly less than at any point during the lead-up to 2019’s pre-COVID downturn/likely recession, and is a level equivalent to past recessions in the database. We also have to take note of the pace for the decline here. |

. |

But it’s not just production nor inventory. As I wrote yesterday after the Fed’s Dallas branch had served up the ugly (and there’s more today; I’ll get to Dallas services later):

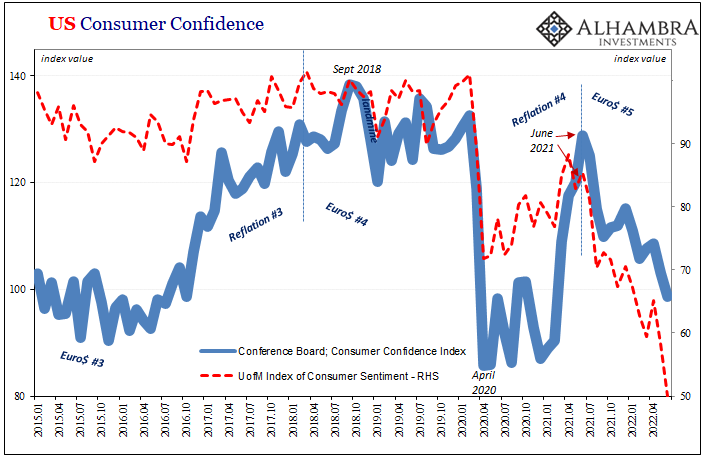

When the orders were placed during last year, companies appear to have fully bought into (literally) the permanent plateau of fiscal prosperity brought about by repeated war-scale government interventions. They never questioned the current nor future state of the American consumer, laser-focused instead on supply problems exclusively. Demand. Demand. Demand. We’ve already seen consumer confidence plummet from the University of Michigan’s poll, as well as the one produced by IBD/TIPP. The lone outlier had been the Conference Board’s, for whatever reason(s). The Board just released its figure for June and, as you can see, it’s no longer holding up so well. While still not nearly as dire as pictured in the other surveys, the direction and more and more its lower and lower levels are corroborating such widespread deterioration. Deterioration where? The demand side; turning into the perfect storm of not-good goods. |

. |

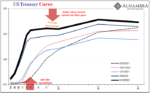

Markets have been pricing a U-turn for Jay Powell most of this year, and eurodollar futures since December last year, even as Chairman Powell has become the most “hawkish” rate-hiker since the “maestro” made his name (riding the coattails of eurodollars). Curves have not only remained adamant about a “policy pivot” even as the FOMC very loudly proclaimed the balance tipped toward consumer prices, they’ve also grown more certain he’ll turnaround this year despite so much official noise and fury otherwise.

This isn’t some modest macro downgrade; no garden variety slowdown would cause a wholesale (pun intended) change from ultra-hawk to rate-cutting and do it in a matter of just months! It’s not just recession what’s being served up and predicted, as more and more data confirms on both sides, supply and demand, it’s looking really nasty from here on.

While the rest of the world only now begins to make peace with recession, we’ve seen it coming the whole way. And now what we see from here is…even worse.

You Might Also Like

2022-06-27

It’s not recession fears, those are in the past. For much if not most (vast majority) of mainstream pundits and newsmedia alike, unlike regular folks this is all news to them (the irony, huh?) Economists and central bankers everywhere had said last year was a boom, a true inflationary inferno raging worldwide.

Prices As Curative Punishment

Prices As Curative Punishment

2022-06-14

It wasn’t exactly a secret, though the raw data doesn’t ever tell you why something might’ve changed in it. According to the Bureau of Economic Analysis, confirmed by industry sources, US new car sales absolutely tanked in May 2022.

ADP Front-Runs BLS and President Phillips

ADP Front-Runs BLS and President Phillips

2022-06-04

It’s gotten to the point that pretty much everyone is now aware of the risks. Public surveys, market behavior, on and on, hardly anyone outside politics thinks the economy is in a good place. Gasoline, sentiment, whatever, Euro$ #5 in total is much more than what’s shaping up inside the American boundary. Globally synchronized of which the US is proving to be a close part.

Can’t Blame COVID For This One

Can’t Blame COVID For This One

2022-06-03

Late in March 2021, then-German Chancellor Angela Merkel announced a reverse. Several weeks before that time, Merkel’s federal government had reached an agreement with the various states to begin opening the country back up, easing more modest restrictions to move daily life closer to normal.

President Phillips Emerges To Reassure On Growing Slowdown

President Phillips Emerges To Reassure On Growing Slowdown

2022-06-02

Just the other day, President Biden took to the pages of the Wall Street Journal to reassure Americans the government is doing something about the greatest economic challenge they face. Biden says this is inflation when that’s neither the actual affliction nor our greatest threat.

China Then Europe Then…

China Then Europe Then…

2022-05-08

This is the difference, though in the end it only amounts to a matter of timing. When pressed (very modestly) on the slow pace of the ECB’s “inflation” “fighting” (theater) campaign, its President, Christine Lagarde, once again demonstrated her willingness to be patient if not cautious.

The Short, Sweet Income Case For Ugly Inversion(s), Too

The Short, Sweet Income Case For Ugly Inversion(s), Too

2022-04-04

A nod to just how backward and upside down the world is now. The economic data everyone is made to pay attention to, payrolls, that one is, in my view, irrelevant. As is the consumer price estimates from earlier this week, the PCE Deflator. That’s another one which receives vast amounts of interest even though it is already old news.

Media Attention All Over FOMC, Market Attention Totally Elsewhere

Media Attention All Over FOMC, Market Attention Totally Elsewhere

2022-03-19

The Federal Reserve did something today, or actually announced today that it will do something as of tomorrow. And since we’re all conditioned to believe this is the biggest thing ever, I’ll have to add my own $0.02 (in eurodollars, of course, can’t be bank reserves) frustratingly contributing to the very ritual I’m committed to seeing end.We shouldn’t care much about the Fed.

Tags: Consumer Confidence,currencies,economy,Featured,Federal Reserve/Monetary Policy,manufacturing,Markets,new orders,newsletter,recession