In this issue of “All Inflation Is Transitory, The Fed WIll Be Late Again.“ Market Review And Update All Inflation Is Temporary The Fed Should Be Hiking Now Portfolio Positioning #MacroView: No. Bonds Aren’t Overvalued. Sector & Market Analysis 401k Plan Manager Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha Catch Up On What You Missed Last Week Market Review & Update Last week, we said: “The market is trading well into 3-standard deviations above the 50-dma, and is overbought by just about every measure. Such suggests a short-term ‘cooling-off’ period is likely. With the weekly ‘buy signals’ intact, the markets should hold above key support levels during the next consolidation phase.” “As shown above, that is what is currently

Topics:

Lance Roberts considers the following as important: 401-k Plan Manager, 9) Personal Investment, 9a.) Real Investment Advice, Featured, Investing, newsletter, Technical Analysis

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

In this issue of “All Inflation Is Transitory, The Fed WIll Be Late Again.“

- Market Review And Update

- All Inflation Is Temporary

- The Fed Should Be Hiking Now

- Portfolio Positioning

- #MacroView: No. Bonds Aren’t Overvalued.

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Catch Up On What You Missed Last Week

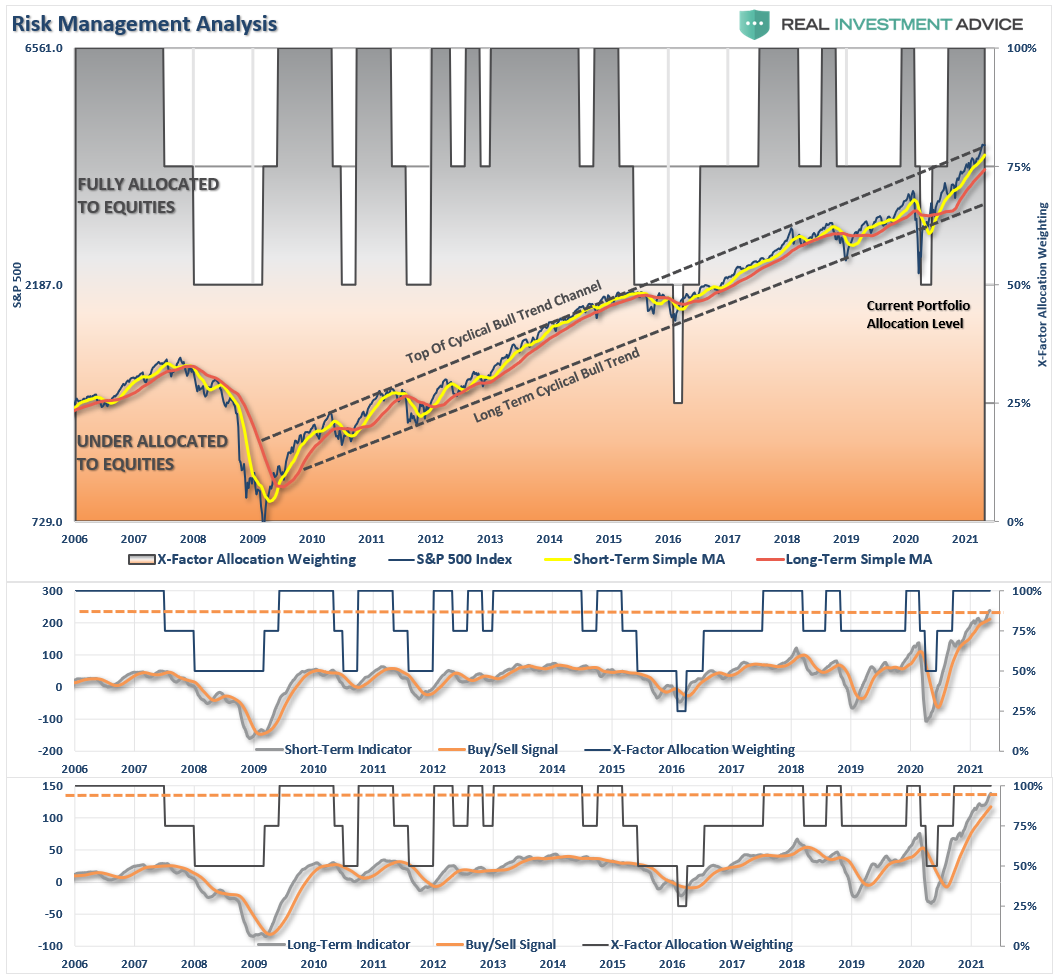

Market Review & Update

Last week, we said:

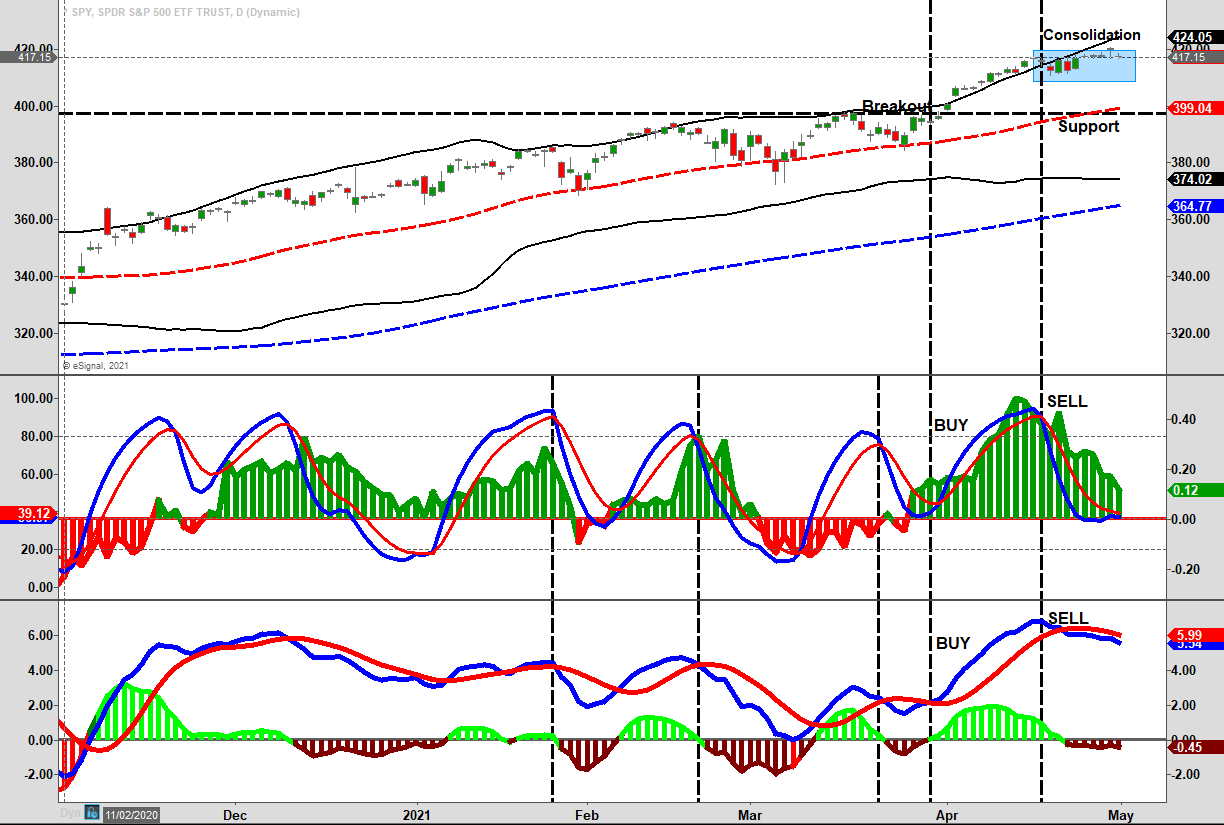

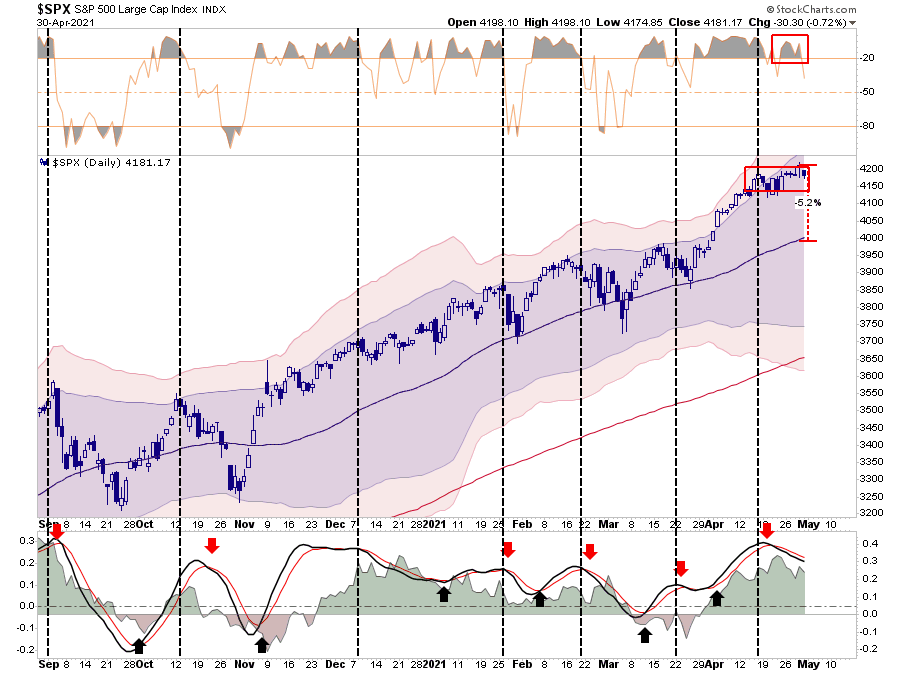

“The market is trading well into 3-standard deviations above the 50-dma, and is overbought by just about every measure. Such suggests a short-term ‘cooling-off’ period is likely. With the weekly ‘buy signals’ intact, the markets should hold above key support levels during the next consolidation phase.”

“As shown above, that is what is currently occurring. While the market remains in a very tight range, the “money flow” sell signal (middle panel) is reversing quickly. Importantly, note that the money flows (histogram) are rapidly declining on rallies which is a concern.”

While the “sell signal” remains intact, not surprisingly, the breakout above the consolidation on Thursday failed, with the selloff on Friday putting the market back where it started the week. Furthermore, the MACD “sell signal” in the lower panel also suggests that prices may remain somewhat capped for the time being.

As noted, the concern remains of the decline in actual money flows. While the market is holding up near all-time highs, the support of positive money flows continues to deteriorate. Weakening money flows with the market remaining at more overbought conditions also suggest upside is limited over the next few weeks.

We discussed these concerns in more detail in the latest 3-Minutes video (click to subscribe.)

For now, the market trend remains bullish and doesn’t suggest a sharp decrease of risk exposures is required. However, after reducing equity exposure previously, we are starting to look for the next short-term opportunity to increase risk. However, we aren’t expecting much before we get into the summer months, where, as we will discuss, the risk begins to rise markedly.

All Inflation Is Transitory

On Wednesday, Jerome Powell commented that while he sees inflation, he believes it to be transitory. As my colleague Mish Shedlock noted:

“Inflation jumped as predicted, and so was the Fed comment about transitory.”

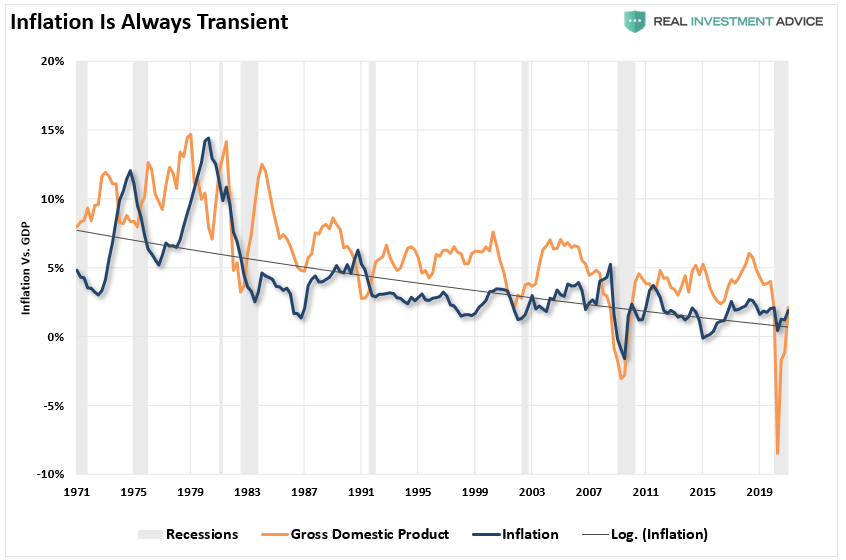

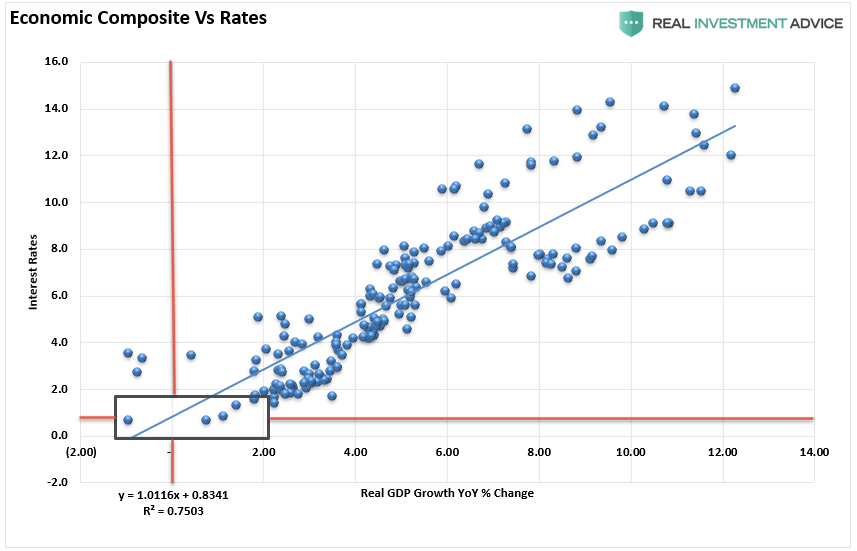

As Mish discusses, inflation depends much on how you measure it and who it impacts. However, inflation is and remains an always “transient” factor in the economy. As shown, there is a high correlation between economic growth and inflation. As such, given the economy will quickly return to sub-2% growth over the next 24-months, inflation pressures will also subside.

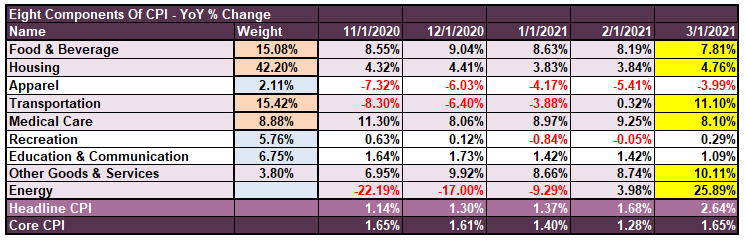

Significantly, given the economy is roughly comprised of 70% consumption, sharp spikes in inflation slows consumption (higher prices lead to less quantity), thereby slowing economic growth. Such is particularly when inflation impacts things the bottom 80% of the population, which live paycheck-to-paycheck primarily, consume the most. The table below shows the current annual percentage change in the various categories.

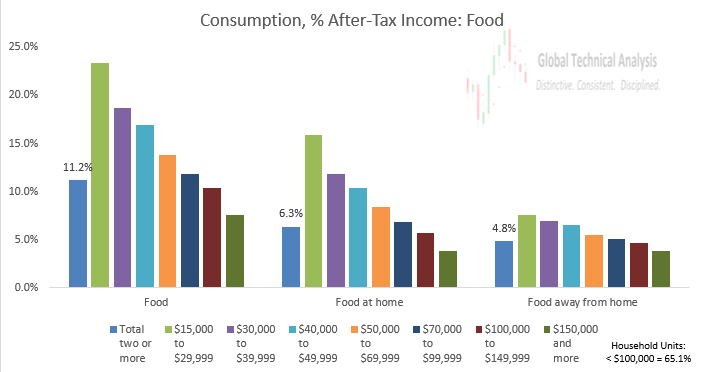

As shown above, food and beverage prices make up 15.08% of the CPI calculation. The chart below from Brett Freeze breaks down how consumers spend their money based on income classes. The lowest income earners, making $15,000 to $29,999, pay almost 25% of their earnings on food. That compares to only 7.5% for families making more than $150,000.

Housing comprises 56.3% of spending for the lowest income class and only 20% for the highest. The CPI inflation calculation does not accurately portray how inflation affects a large percentage of the population. (This is also the group whose entire boost in income from the stimulus will get absorbed by higher prices)

The Fed May Be Right For The Wrong Reason

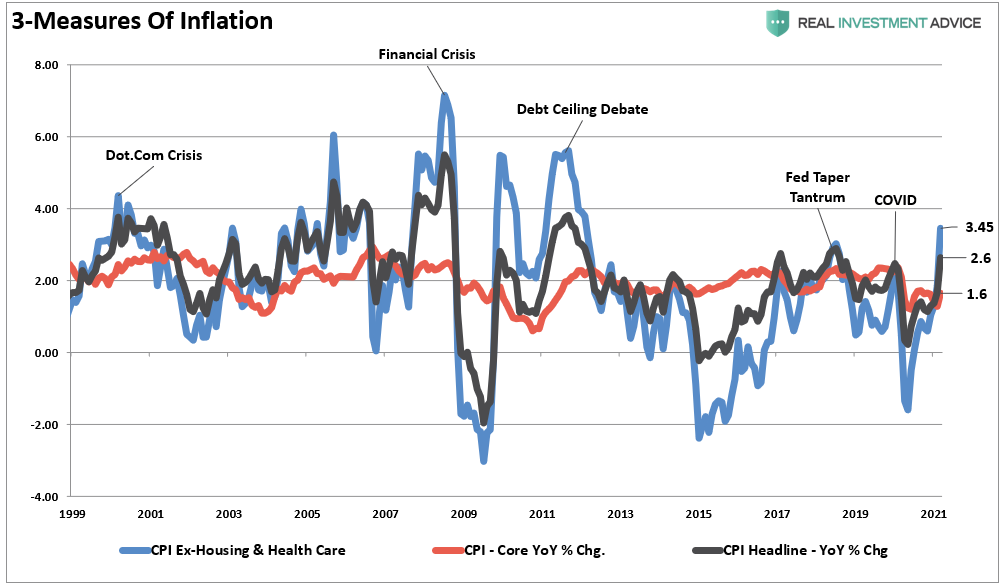

With double-digit rates of change in essential items like transportation (going back to work), food, goods and services, and energy, the impact on disposable incomes will come much quicker than expected. If we strip out “housing and healthcare,” which are fixed budget items (mortgage and insurance payments), we see that “household” inflation is pushing 3.5% annualized.

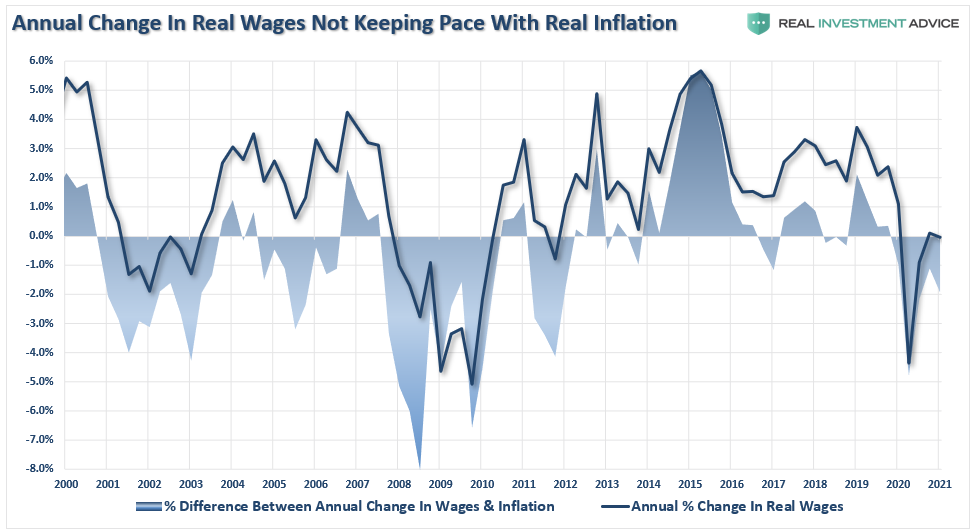

Such is particularly problematic when wages aren’t keeping up with inflation.

The Fed is probably right. Inflation will be transitory, but for all the wrong reasons.

Rates Tell The Same Story

As discussed in Friday’s #MacroView, interest rates also tell us that economic growth will deteriorate markedly over the next few quarters.

“The correlation should be surprising given that lending rates get adjusted to future impacts on capital.

- Equity investors expect that as economic growth and inflationary pressures increase, the value of their invested capital will increase to compensate for higher costs.

- Bond investors have a fixed rate of return. Therefore, the fixed return rate is tied to forward expectations. Otherwise, capital is damaged due to inflation and lost opportunity costs.

As shown, the correlation between rates and the economic composite suggests that current expectations of sustained economic expansion and rising inflation are overly optimistic. At current rates, economic growth will likely very quickly return to sub-2% growth by 2022.”

The problem for the Federal Reserve, and as quoted by Mish, is that the fiscal and monetary stimulus imputed into the economy is “dis-inflationary.”

“Contrary to the conventional wisdom, disinflation is more likely than accelerating inflation. Since prices deflated in the second quarter of 2020, the annual inflation rate will move transitorily higher. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that the inflation rate will moderate lower by year end and will undershoot the Fed Reserve’s target of 2%. The inflationary psychosis that has gripped the bond market will fade away in the face of such persistent disinflation.” – Dr. Lacy Hunt

The point here is that while economic growth may be booming momentarily, inflation, which is destructive when not paired with rising wages, will be transient. Given the massive surge in prices for homes, autos, and food, the reversal will cause a substantial disinflationary drag on economic growth.

The Fed Should Be Hiking And Tapering Now

There is a significant difference between a “recovery” and an “expansion.” One is durable and sustainable; the other is not.

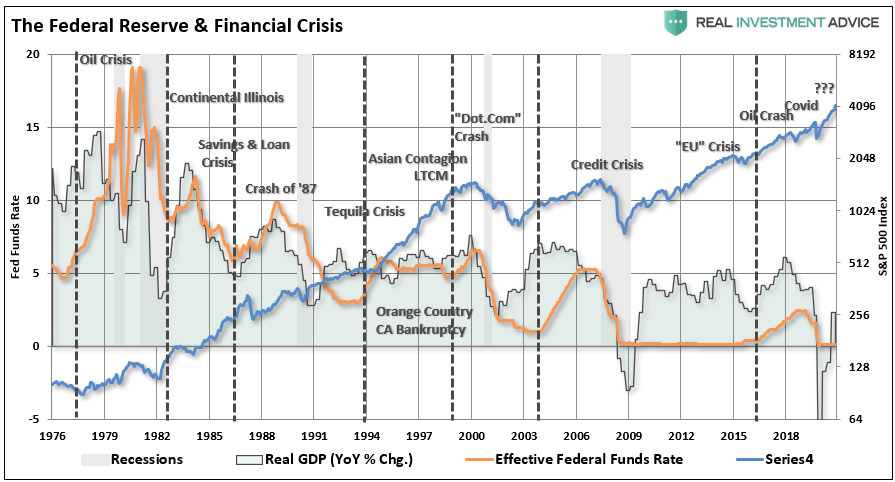

Following the financial crisis, the Federal Reserve cut rates and flooded the markets with liquidity. As discussed in “The Fed Continues To Make Policy Mistakes,” the Fed should have acted sooner to prepare for the next economic downturn.

“The Fed should have started lifting rates as the spike in economic growth occurred in 2010-2011 as both the Fed and Government flooded the economy with liquidity. While hiking rates would have slowed the advance in the financial markets, the excess liquidity sloshing around the system would have offset tighter monetary policy.”

The Fed is again suppressing rates but should be using the massive liquidity injections and economic recovery for hiking rates and taper bond purchases to prepare for the next downturn.

As Mohammed El-Erian noted:

“The majority of market participants are expecting an undramatic event including an upgraded economic outlook, a reiteration of uncertainties and signaling of no policy changes. Unfortunately, it’s an outcome that kicks the policy can down the road when the central bank should be thinking now about scaling back extraordinary measures.

The longer it takes to do so, the harder it will be to pull off eventual normalization without risking both significant market volatility and damaging what should and must be a durable and inclusive economic recovery.”

By not hiking rates now, they run the risk of being late once again.

Given the Fed waited too long to hike rates previously, such will be the same this time as they start hiking rates just as economic growth peaks due to the roll-off of stimulus.

There have been ZERO times in history when the Fed started a rate hiking campaign that did not lead to a negative outcome.

Something Is Going To Break

The “frenzy” of investors to get into the market is unlike anything we have seen since 1999.

The Fed’s problem is that in 1999 there was a bubble in “Dot.com” stocks but not in many other areas of the market. In 2007, it was a mortgage market bubble, but valuations were not extremely elevated in stocks.

Today, we are:

- Pushing the second-highest level of valuations in history

- Many other valuation measures such as Price-to-Sales, Tobin’s-Q, and Market-Cap to GDP are at a record.

- Investors are rushing to buy the most speculative assets from various Cryptocurrencies, to Non-Fungible Tokens (NFT’s), to highly speculative companies.

- Wall Street is rushing IPO’s to market at the fastest pace on record.

- SPAC’s are the new asset class.

- A large portion of the Russell 2000 companies have no income.

- The bonds with the highest risk of default are trading at historically low rates.

- Individuals are rushing to pay the highest prices on records for housing and used cars.

- And, it’s all done with the highest margin debt levels in history.

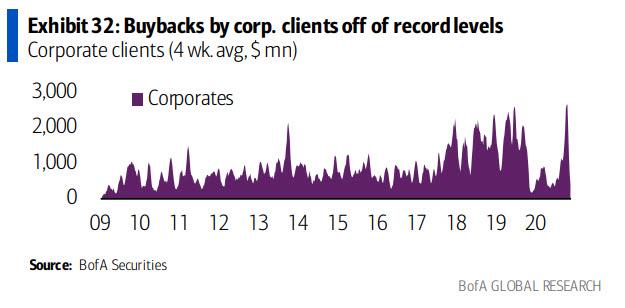

Of course, corporations are in on it as well, buying back their shares at a record pace (just after asking the government for a taxpayer-funded bailout in March 2020.)

Trapped With No Escape

In other words, it isn’t just one bubble the Fed will have to deal with during the subsequent market melt-down. It will be all of them. The magnitude of the meltdown of multiple asset classes at one time will likely be larger than the Fed can bailout.

Importantly, I believe they know this already and hope that an inflationary push will help deflate some of the risks before the bubble bursts. As my colleague Doug Kass wrote on Thursday:

“From my perch, and in the end, of course, all violation of the fundamental laws of economic and financial common sense are paid for – but every Bull thinks he will unload before the break.

John Kenneth Galbraith once wrote that “What we do know is that speculative episodes never come gently to an end. The wise, though for most the improbable, course is to assume the worst.”

I believe that there are numerous other bubbles or inflated values. Moreover, I see numerous headwinds that could reset broad valuations lower. Such includes higher corporate and individual tax rates, inflation, and inflated bullish investor sentiment.

It is easy enough to burst a bubble. To incise it with a needle so that it subsides gradually is an operation of undoubted delicacy.”

I agree.

The bottom line is the Fed is trapped. If they hike rates, they bust the bubble and destroy economic growth. If they do nothing, the bubble inflates to a point it breaks under its weight.

In my opinion, not that it matters; it seems the risk of doing nothing far outweighs doing something. Taking small actions today to slowly deflate risk seems a much better alternative to the eventual bust.

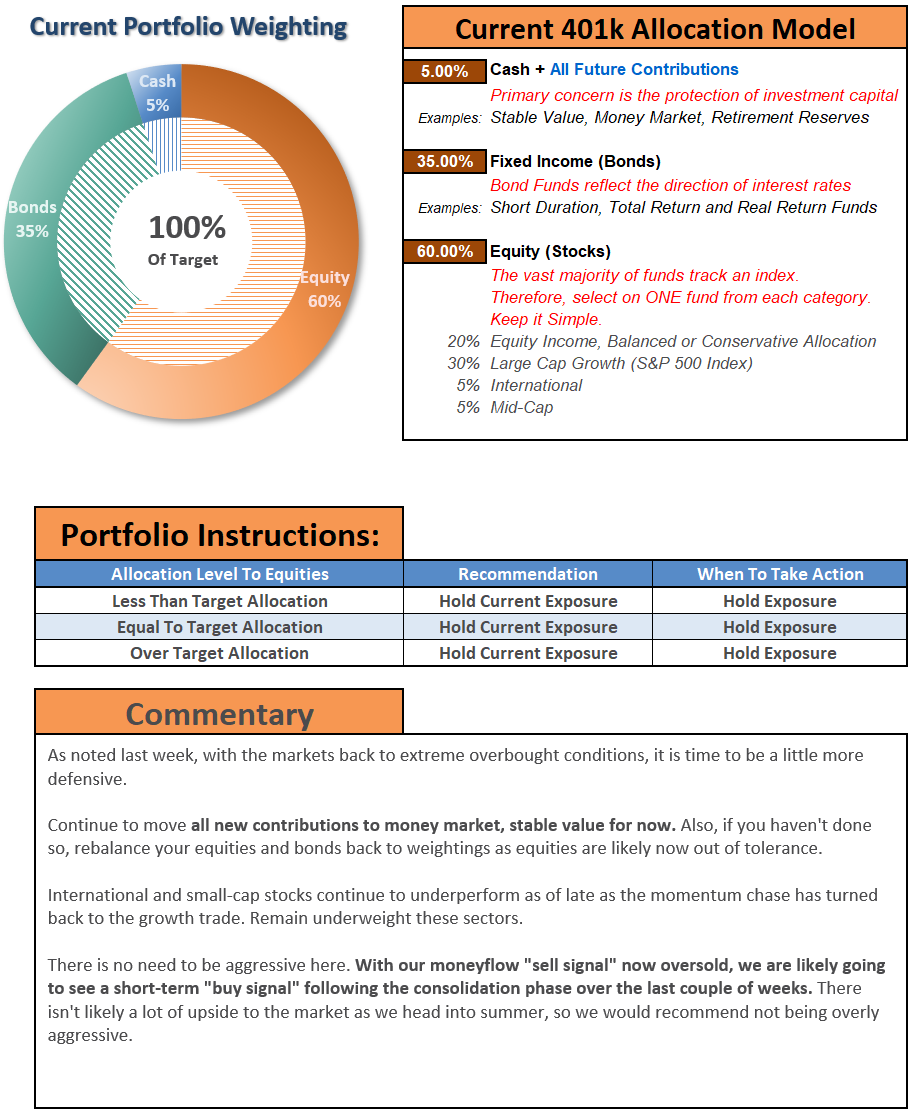

Portfolio Update

As noted above, we will trigger the next short-term “buy signal,” likely next week. As we have discussed regularly, given the daily “sell signal” was offset by a weekly “buy signal,” there was little downside risk. Such turned out to be the case.

We can now start adding some additional exposure to areas that we need, but with equity holdings at near target weights, only minor adjustments need to get done. We still carry a very short-duration bond portfolio currently as interest rates continue to push towards our target of 1.8-1.9%. At that level, we will start accumulating long-duration bonds and increasing portfolio hedges.

Another reason we don’t expect a lot of upside to markets because the recent “consolidation” failed to work off any of the overbought conditions. Notably, the market remains more than 5% above its 50-dma, which is historically extreme. Such gets corrected, usually through a price decline or a consolidation.

Over the last two weeks, we had suggested cleaning up portfolios and rebalancing risk. With that complete, portfolios should be in an excellent position to participate in whatever rally we get over the next couple of weeks.

As we head into summer, we will likely see our weekly and daily signals align with “sell signals” in late May or early June. Such will likely coincide with a realization of peak earnings and economic growth. While we don’t expect a significant reversion at this juncture, given the ongoing liquidity support, a 7-10% correction is possible and well within annual norms.

Could it be more? Absolutely.

But that is something we will navigate once we get there.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Analysis & Stock Screens Exclusively For RIAPro Members

Discover All You Are Missing At RIAPRO.NET

This is what our RIAPRO.NET subscribers are reading right now! Risk-Free For 30-Day Trial.

- Sector & Market Analysis

- Technical Gauge

- Fear/Greed Positioning Gauge

- Sector Rotation Analysis (Risk/Reward Ranges)

- Stock Screens (Growth, Value, Technical)

- Client Portfolio Updates

- Live 401k Plan Manager

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert, do not hesitate to contact me.

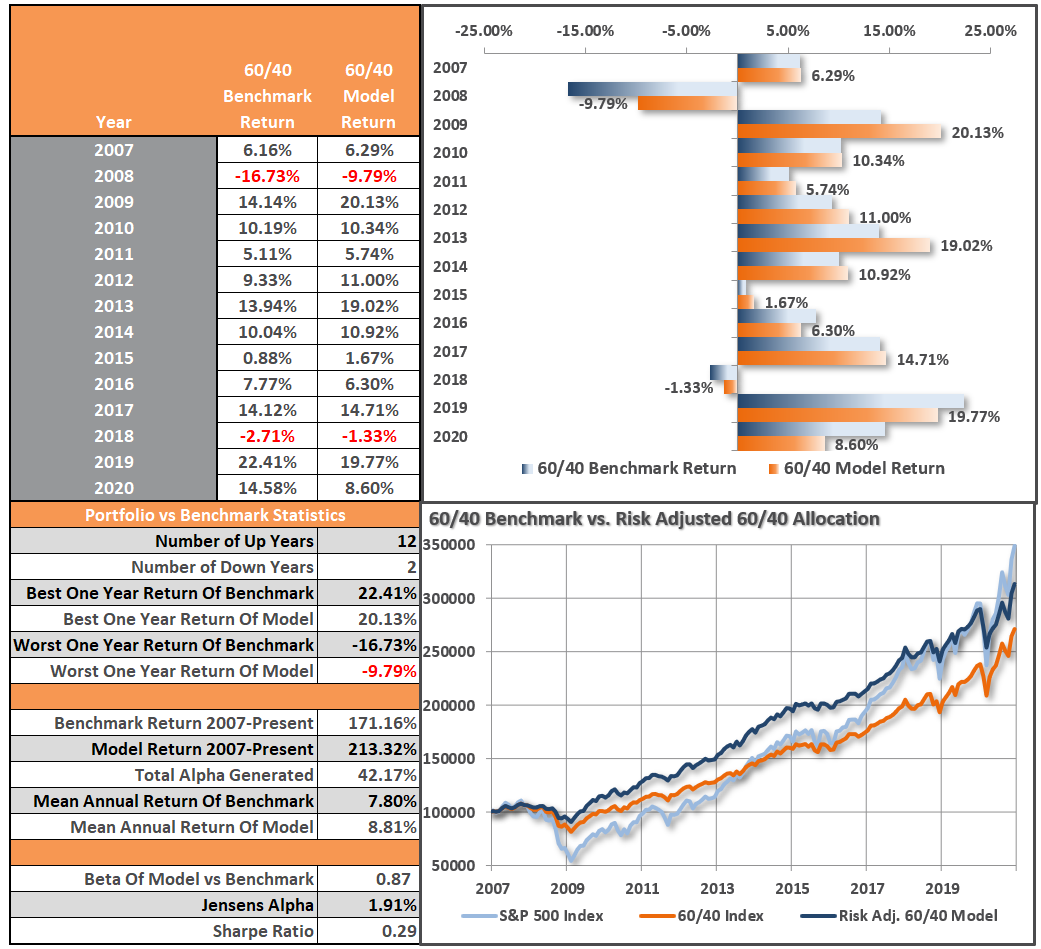

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only, and one should not rely on it for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

Have a great week!

The post All Inflation Is Transitory. The Fed Will Be Late Again. 04-30-21 appeared first on RIA.

You Might Also Like

Seth Levine: Bitcoin Doesn’t Fix Defi, Defi Fixes Bitcoin

Seth Levine: Bitcoin Doesn’t Fix Defi, Defi Fixes Bitcoin

2021-05-02

Does Bitcoin Fix Defi (Definancialization)? “Bitcoin fixes this.” I cringe every time I see this popular meme. I find it worse than nails on a chalkboard. Bitcoin and other cryptocurrencies (crypto) supporters seem to wheel this tired trope out for every problem they see, particularly at economic ones. To their credit, they genuinely want to fix the financial system’s problems.

The Battle Royale: Stocks vs. Bonds (Which Is Right?)

The Battle Royale: Stocks vs. Bonds (Which Is Right?)

2021-04-28

The Battle Royale: Stocks vs. Bonds. The S&P 500 is at valuations higher than those in 1929 and rival those of 1999. Despite a recession, the index is 25% above where it was trading before the pandemic. The equity stampede is undoubtedly bullish about corporate earnings prospects and, by default, economic growth.

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

2021-04-26

Update April 26 2021: SNB intervening. Sight Deposits have risen by +0.2 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.2 bn. compared to last week.

Introduction to short selling: How to bet against a stock?

Introduction to short selling: How to bet against a stock?

2021-03-30

Many of you have probably heard of the Gamestop saga. A lot of hedge funds were short selling Gamestop stocks. And some investors found out about that and decided to fight against the big hedge funds by massively buying into this stock.

But what is shorting a stock? When you are shorting a stock, you are betting against this stock. But why and how to do that?

A Major Support For Asset Prices Has Reversed

A Major Support For Asset Prices Has Reversed

2020-12-24

In 2019, we wrote about how corporate share repurchases, or “stock buybacks,” had accounted for nearly all buying in the market. A year later, that significant support for asset prices has reversed.

You should invest every month not every quarter

You should invest every month not every quarter

2020-12-04

I have recently read a recommendation to invest only once a quarter instead of more frequently. I think investing every quarter is bad advice and I want to explain why in this article.

Free by 40 in Switzerland – Book Review

Free by 40 in Switzerland – Book Review

2020-11-27

I just finished reading Free by 40 in Switzerland, a book about financial independence, in Switzerland, by fellow blogger Mr. Mustachian Post, alias Marc Pittet. Mr. MP was kind enough to send me a version that I could review before the release date. So I can have this review ready now that the book is available!

2020-11-20

Investing is incredibly hard. Mapping observations to security price movements are complex. Often, the relationships governing these moves are unknown. Yet, this is the investor’s task. I’ve used this blog as a tool for exploring some of these connections. It’s been incredibly rewarding.

Tags: 401-k Plan Manager,Featured,Investing,newsletter,Technical Analysis