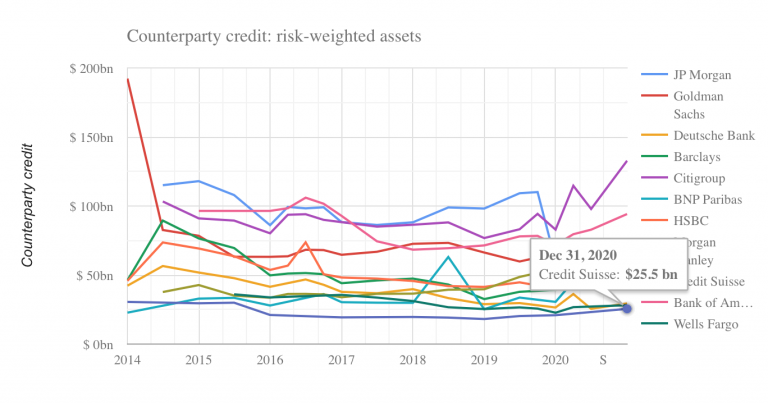

Authored by Nick Dunbar of Risky FinanceWhen the family office Archegos Capital abruptly imploded in late March, prompting billion in block trades and billion in losses at Credit Suisse, Nomura, UBS and Morgan Stanley, many bank analysts were taken by surprise. Last week, many of these analysts sounded frustrated listening to Credit Suisse’s earnings call in which senior management skirted round without giving any real detail about the disaster.“Do you think it’s possible that this could produce a very fundamental reset in how your IRB credit risk models work?” wondered Stefan Stalmann of Autonomous Research. “I mean you have only CHF20 billion to CHF25 billion of counterparty credit risk-weighted assets on literally hundreds of billions of equity swaps

Topics:

Tyler Durden considers the following as important: 1.) Zerohedge on SNB, 1) SNB and CHF, 3.) Swiss Banks, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Authored by Nick Dunbar of Risky Finance

When the family office Archegos Capital abruptly imploded in late March, prompting $50 billion in block trades and $10 billion in losses at Credit Suisse, Nomura, UBS and Morgan Stanley, many bank analysts were taken by surprise. Last week, many of these analysts sounded frustrated listening to Credit Suisse’s earnings call in which senior management skirted round without giving any real detail about the disaster.

“Do you think it’s possible that this could produce a very fundamental reset in how your IRB credit risk models work?” wondered Stefan Stalmann of Autonomous Research. “I mean you have only CHF20 billion to CHF25 billion of counterparty credit risk-weighted assets on literally hundreds of billions of equity swaps and repos”.

Risky Finance shares Stalmann’s bewilderment. Expressed as a capital requirement, Credit Suisse was able to satisfy regulators with just $2 billion of capital for counterparty credit losses – the lowest among the G-SIFI banks tracked by Risky Finance. Months later it reported a loss of $4.7 billion.

It should serve as a warning. 14 years ago, obscure corners of banking businesses became hotbeds of regulatory arbitrage, speculation and leverage. The contagion of US subprime brought the financial system to its knees. Now, after years of low or negative interest rates, equity finance may have become a similar hotbed.

The business is much larger than published estimates – Risky Finance believes there are more than $3 trillion of exposures. And the pressure to grow equity finance is leading banks to exploit loopholes in Basel rules. As in 2007, this is masked by the complexity of the models that Credit Suisse and other banks used to allocate capital to their prime brokerage business.

In following articles we will try to unpick the way Archegos was so damaging, and we will give a broad brush picture of how the risk models are supposed to work. And we will showcase some new data that reveals why this business is bigger and riskier than many imagined. Lastly we will identify a list of fixes for regulators to work on.

You Might Also Like

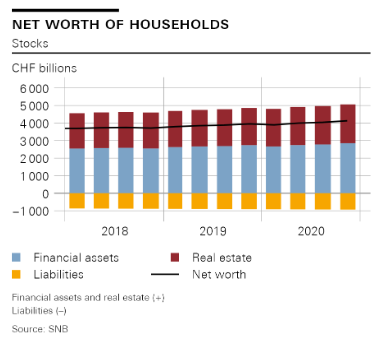

Swiss Financial Accounts: Household wealth in 2020 and focus article

Swiss Financial Accounts: Household wealth in 2020 and focus article

2021-05-01

Financial and real estate wealth of households increases. The Swiss National Bank is today publishing data on Q4 2020 as part of the financial accounts. Thus, household wealth data are now also available for the full year.

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

2021-04-26

Update April 26 2021: SNB intervening. Sight Deposits have risen by +0.2 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.2 bn. compared to last week.

Credit Suisse Slashes Bonuses After $4.7 Billion Archegos Disaster

Credit Suisse Slashes Bonuses After $4.7 Billion Archegos Disaster

2021-04-13

While all of the banks playing “pass the hot potato” with Archegos Capital’s now-dismantled equity book are undoubtedly still assessing the damage they incurred (or at least will report to shareholders), it looks like no one had it worse than Credit Suisse. The banking giant has now slashed its bonus pool by “hundreds of millions of dollars” according to FT, after the firm lost $4.7 billion in the Archegos implosion.

Credit Suisse Dumping Huge Archegos Blocks; Liquidating Millions In VIACS, VIPS And FTCH

Credit Suisse Dumping Huge Archegos Blocks; Liquidating Millions In VIACS, VIPS And FTCH

2021-04-06

Literally moments ago we said that the Archegos portoflio was being sold off all day on fears of "stealth" prime broker deleveraging, as tens of millions of shares were yet to be accounted for.

Credit Suisse Launches Probe Into Collapsed Greensill Trade-Finance Funds

Credit Suisse Launches Probe Into Collapsed Greensill Trade-Finance Funds

2021-03-11

Roughly a weekand a-half has passed since Credit Suisse gated funds containing $10BN in assets packaged by Greensill, the troubled financial innovator that suckered in former British PM David Cameron, SoftBank and legions of clients and investors with its stated mission to “democratize” supply-chain finance.

Gold Could Offer A Way Out Of Switzerland’s Failing Inflationist Experiment

Gold Could Offer A Way Out Of Switzerland’s Failing Inflationist Experiment

2021-02-08

Authored by Brendan Brown via The Mises Institute,Never mind that the US Treasury’s indictment late last year of Switzerland as a currency manipulator rested on some flawed evidence and does not identify the crime.

SNB-Jordan: Haben gute Lösung zu höheren Gewinnausschüttungen getroffen

SNB-Jordan: Haben gute Lösung zu höheren Gewinnausschüttungen getroffen

2021-02-02

“Wenn es der Nationalbank über die Jahre gut geht, kann sie viel ausschütten. Wenn es aber schlechter geht, werden wir die Ausschüttungen wieder reduzieren”, sagte Jordan weiter. Dabei stütze sich die neue, am vergangenen Freitag kommunizierte Vereinbarung auf die alten Abmachungen zur Ausschüttung an Bund und Kantone, nur dass die Bilanz und die Ausschüttungs-Reserve heute deutlich höher seien als vorher.

“Dirk Niepelt im swissinfo.ch-Gespräch (Interview with Dirk Niepelt),” swissinfo, 2020

“Dirk Niepelt im swissinfo.ch-Gespräch (Interview with Dirk Niepelt),” swissinfo, 2020

2020-12-16

Swissinfo, December 14, 2020. HTML, podcast.

We talk about CBDC, the Swiss National Bank, whether CBDC would render it easier to implement helicopter drops, and how central bank profits should be distributed.

Tags: Featured,newsletter