The rosy US employment picture helped push equities to a new high as US inflation moderated in July. Those looking to fill roles now exceed those looking for work, compelling some small and mid-sized companies to raise wages. Higher prices seem to be keeping the US consumer in check, however, with consumer sentiment hitting its lowest level in a decade. We will be watching how this evolves given the US consumer’s key to the growth recovery story. The US earnings season concluded on a high note, with an impressive 88% year-on-year (y-o-y) earnings per share (EPS) growth for the S&P500 index. For the full year, EPS growth for the index is expected to be 45.8% in 2021, followed by 9.4% for 2022. However, depending on how President Biden’s tax plan pans out, the 2022

Topics:

Cesar Perez Ruiz considers the following as important: 2.) Pictet Macro Analysis, 2) Swiss and European Macro, Featured, Macroview, newsletter, Pictet

This could be interesting, too:

investrends.ch writes Pictet als Bester Schweizer Asset Manager im Bereich Nachhaltigkeit und Markenführung ausgezeichnet

investrends.ch writes Vom Ölschock zum Stromsuperzyklus

investrends.ch writes Pictet steigt in den Schweizer Treuhandmarkt ein – Partnerschaft mit Tretor

investrends.ch writes Die Schweiz an der Schwelle zur digitalen Transformation der Fondsindustrie

The rosy US employment picture helped push equities to a new high as US inflation moderated in July. Those looking to fill roles now exceed those looking for work, compelling some small and mid-sized companies to raise wages. Higher prices seem to be keeping the US consumer in check, however, with consumer sentiment hitting its lowest level in a decade. We will be watching how this evolves given the US consumer’s key to the growth recovery story. The US earnings season concluded on a high note, with an impressive 88% year-on-year (y-o-y) earnings per share (EPS) growth for the S&P500 index. For the full year, EPS growth for the index is expected to be 45.8% in 2021, followed by 9.4% for 2022. However, depending on how President Biden’s tax plan pans out, the 2022 figure could be revised lower. We prefer the outlook for developed-market equities as the reopening of these economies boosts corporate earnings.

In the world’s second largest economy, deleveraging continues with weaker-than-expected credit figures in China. The highly-leveraged developer, China Evergrande, received some fresh oxygen in the form of new bank loans and some breathing room for its embattled shares, which jumped on news that it would offload some assets. Chinese high-yield spreads tightened to some degree but the market remains wary of the potential for further problems in other companies and the risk of contagion. Meanwhile, China’s president Xi Jinping unveiled a new five-year plan to “strengthen and control” the economy, extending the central oversight of key sectors. We are neutral emerging markets.

The end of the international Bretton Woods monetary system marked its 50th anniversary. That makes the floating rates regime that followed 50 years old, and while it has been largely successful, the recent rise of crypto and other digital currencies could raise some questions about its future. Last week, hackers stole USD600 mn of digital tokens… before returning a portion of them and committing to return the rest. The entire bizarre incident reminds us how the related risks and consequences are as novel as the cryptocurrencies themselves. In the black and white fiat world, the USD strengthened last week and the US Senate passed Biden’s USD550 bn infrastructure plan with another even larger spending plan (USD 3.5 trillion in total) in the congressional pipeline.

You Might Also Like

SNB Sight Deposits: Inflation is there, CHF must Rise

SNB Sight Deposits: Inflation is there, CHF must Rise

2021-08-16

Sight Deposits have risen by +2.7 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

Weekly View – Staying on script

Weekly View – Staying on script

2021-07-20

Big US banks released their 2Q earnings last week. The figures were good thanks to robust growth in investment-banking income as well as a drop in loan-loss provisions. But banks also reported that wage costs were beginning to rise, and while a booming housing market has boosted mortgage-loan business, the renewed retreat in long-term yields has been a drag on interest income.

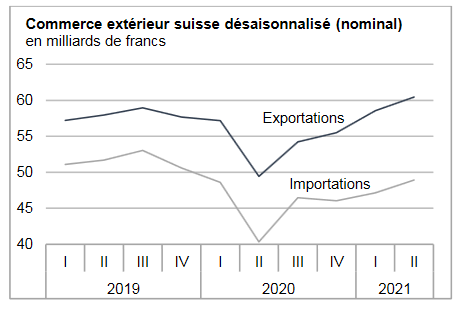

Swiss Trade Balance Q2 2021: export record

Swiss Trade Balance Q2 2021: export record

2021-07-20

Swiss foreign trade showed dynamism in the second quarter of 2021. Exports rose 3.2% to a record level. They posted a fourth consecutive quarterly increase since the drop recorded at the start of the coronavirus pandemic. Imports continued the momentum of the previous quarter and increased 3.8%. The trade surplus stood at 11.5 billion francs.

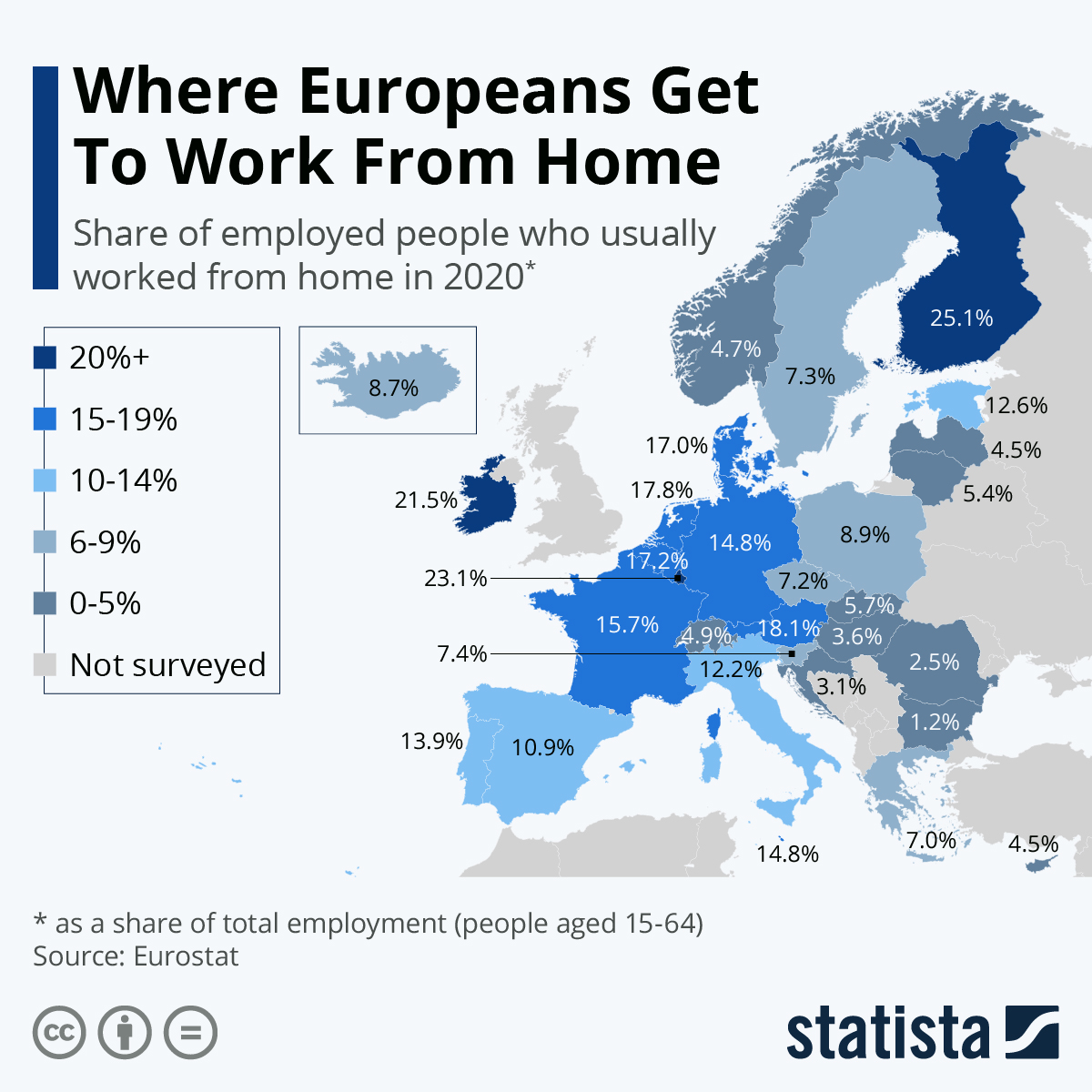

Where Europeans Get To Work From Home

Where Europeans Get To Work From Home

2021-05-20

The social distancing measures introduced in response to the Covid-19 pandemic has forced many people to work from home and accelerated the trend of remote working. Eurostat have released some interesting new data showing the share of employed people aged between 15 and 64 in Europe who usually do home office.

Weekly View – M&A Boom

Weekly View – M&A Boom

2021-04-13

M&A (mergers and acquisitions) activity is on the rise, as companies coming out of the pandemic with strong balance sheets shop for buying opportunities. Last week ACS, a Spanish construction group, approached Italian transport company Atlantia to buy Italy’s largest motorway network. Two big funds are also eyeing Dutch telecommunications company KPN as a potential acquisition target.

House View, April 2021

House View, April 2021

2021-04-06

We believe that robust earnings growth will overcome concerns about rate increases. Within a neutral position on developed-market equities, we believe sectoral rotation will continue and we remain overweight cyclical markets like the UK and Japan. But while we believe the attractiveness of stocks subject to wild valuation swings will fade, we continue to like cash-rich ‘structural grower’ stocks.

Swiss Producer and Import Price Index in January 2021: -2.1 percent YoY, +0.3 percent MoM

Swiss Producer and Import Price Index in January 2021: -2.1 percent YoY, +0.3 percent MoM

2021-02-23

23.02.2021 – The Producer and Import Price Index rose in January 2021 by 0.3% compared with the previous month, reaching 100.3 points (December 2020 = 100). The rise is due in particular to higher prices for scrap, petroleum products, as well as for basic metals and semi-finished metal products. Compared with January 2020, the price level of the whole range of domestic and imported products fell by 2.1%.

Secondary sector with strong production and turnover losses in the 4th quarter and for the whole of 2020

Secondary sector with strong production and turnover losses in the 4th quarter and for the whole of 2020

2021-02-19

Secondary sector production declined 3.1% in 4th quarter 2020 in comparison with the same quarter a year earlier. Turnover fell by 4.4%. For 2020 as a whole which was shaped by the Covid 19 pandemic, there were strong decreases in production (-3.3%) and turnover (-5.2%).

Tags: Featured,Macroview,newsletter,Pictet