May you live in interesting times. Although that sounds like an ancient blessing, it’s believed to be a Chinese curse casting instability and uncertainty on the person who hears it. Blessing or curse, it’s a great description of the year we’ve just come through, and in spite of all the turmoil, there are some things you can do before the end of 2020 to take advantage of all the madness. Strauss Attorneys PLLC has come up with a list of estate planning insights, cautions, and opportunities for you to consider. • Falling Values: some assets, be they business, real estate, or stock, have decreased in value over the past year. It may be a good time to transfer those depreciated assets to a younger generation and let the assets regain their value in their hands, and

Topics:

Bob Williams considers the following as important: 5.) Alhambra Investments, Estate Planning, Featured, Financial Planning, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

May you live in interesting times. Although that sounds like an ancient blessing, it’s believed to be a Chinese curse casting instability and uncertainty on the person who hears it.

May you live in interesting times. Although that sounds like an ancient blessing, it’s believed to be a Chinese curse casting instability and uncertainty on the person who hears it.

Blessing or curse, it’s a great description of the year we’ve just come through, and in spite of all the turmoil, there are some things you can do before the end of 2020 to take advantage of all the madness. Strauss Attorneys PLLC has come up with a list of estate planning insights, cautions, and opportunities for you to consider.

• Falling Values: some assets, be they business, real estate, or stock, have decreased in value over the past year. It may be a good time to transfer those depreciated assets to a younger generation and let the assets regain their value in their hands, and not yours.

• Pause Button: The CARES Act of 2020 allows retirement plan participants to avoid taking minimum distributions for 2020. While you must pay income tax on the conversion, not taking distributions from a Traditional IRA may mean this is a perfect time to convert your traditional IRA to a ROTH IRA, because it might keep or put you in a favorable tax bracket by reducing your taxable income.

• How Low Can You Go: interest rates are at an all-time low, creating ideal planning opportunities for intra-family loans, Grantor Retained Annuity Trusts, Intentionally Defective Grantor Trusts, and Charitable Lead Annuity Trusts.

• Accumulation, Not Conduit: The SECURE Act of 2019 eliminated most of your beneficiaries’ ability to stretch out your retirement plans (with certain exceptions, like your spouse and individuals less than 10 years younger than you). Now, rather than being able to stretch the plan out over the life of the beneficiary, all the proceeds need to be distributed within 10 years (unless an exception applies).

Your trust needs to be reviewed to make sure it is no longer a conduit trust that simply pushes the distributions through as that may not be tax advantageous. A possibly better path is for your trust to be an accumulation trust because it is more flexible and does not hamstring your beneficiary’s ability to do effective income tax planning with your plan.

• Estate Taxes—Riding Into The Sunset: Right now, a married couple can transfer up to $23.16 million without transfer tax, but that is set to sunset at the end of 2025 at which time it will return to the 2017 amount of $5 million (indexed for inflation). However, it may be lowered sooner than that, and to a lower rate, for political reasons. We may be in a situation, for some, where “use or lose it” may be an appropriate phrase. The IRS has said they will not “claw back” your use of the exemption amounts if you use those amounts now. There is a myriad of ways to take advantage of this high threshold.

• The Step-Up Dance May Be Over: Currently, a beneficiary’s tax basis in an asset, if they receive the asset due to the death of another is the asset’s fair market value when a decedent dies. This is called the “step-up” in basis. It is a potentially huge tax savings to beneficiaries because if they sell the asset shortly after the death of the decedent they may not need to owe much, if any, capital gains on the sale. That may be changing. It has been rumored that the Biden administration is considering doing away with the step-up in basis.

• Be Charitable (But Maybe Not Now): While charitable intentions are good, it may serve you to wait until next year. The Biden administration has indicated it is going to increase income tax rates—thus, any charitable deductions will be worth more when the rates are higher. Of course, if taxes are not of paramount importance, then there is no need to delay your giving.

These are just a few of the “highlights” from this past year. As always, the end of the year is a good time to review your beneficiary designations as well as your estate planning documents to be sure that the trusted parties you named are still appropriate and the documents reflect your intentions.

You Might Also Like

5 Estate Planning Myths That Can Derail Your Estate Plan

5 Estate Planning Myths That Can Derail Your Estate Plan

2020-10-18

You spend a lifetime earning, saving, acquiring. But the old adage is true—you can’t take it with you. So, what do you do with your assets when you’re gone? How do you want them distributed? That’s where a good estate plan comes in.

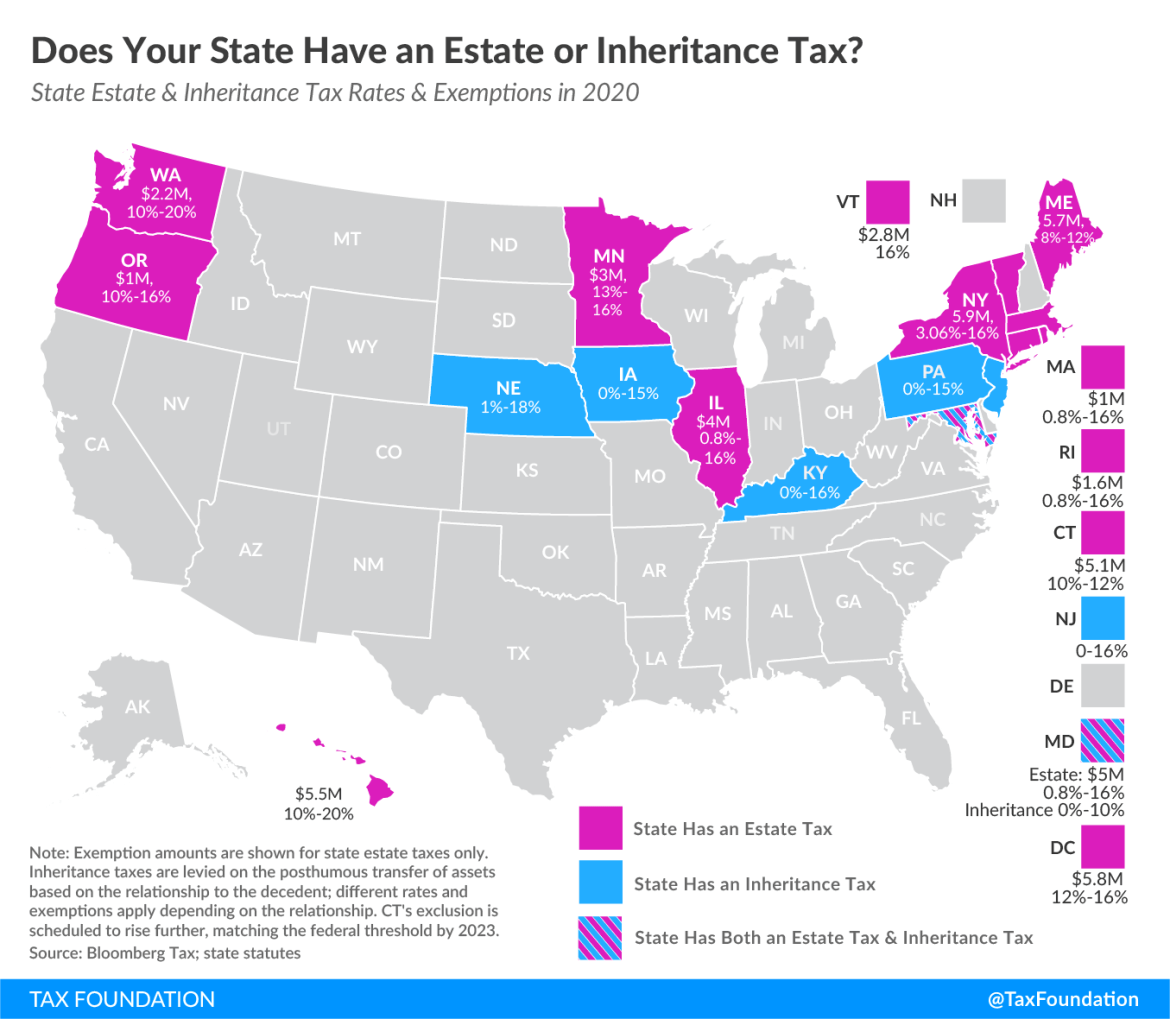

17 States that Charge Estate or Inheritance Taxes

17 States that Charge Estate or Inheritance Taxes

2020-11-03

Death tax, inheritance tax, estate tax—call it what you will, they all mean that some government entity wants to put its hand in your pocket or your heirs’ pockets, after your demise.

5 Tax Strategies to Help you Hold on to Your Money in Retirement

5 Tax Strategies to Help you Hold on to Your Money in Retirement

2020-08-05

What is retirement, really? We think we know. So, we do our best to prepare for both current circumstances and as many surprises as we can conjure up. After all, with people living longer than ever before your money has to last longer than ever before.

12 States That Keep Retirement Dollars in Your Pocket

12 States That Keep Retirement Dollars in Your Pocket

2020-09-18

“Will I outlive my money?” That’s one of the biggest concerns for most retirees. There’s the high cost of medical care, which gets more expensive all the time. There’s inflation, which raises the cost of goods and services, eating into your retirement budget.

How Much Taxes Will Retirees Owe on Their Retirement Income

How Much Taxes Will Retirees Owe on Their Retirement Income

2020-11-10

Planning for retirement. We spend most of our working career preparing for it, saving for it, covering every contingency. When you finally wave goodbye to the company, you’re ready for all that planning to take over. But does your planning take into account the taxes you’ll have to pay on your retirement income? It’s one of the biggest retirement planning mistakes people make.

Retirement Income Planning Truth with Jim Otar. Part 1.

Retirement Income Planning Truth with Jim Otar. Part 1.

2020-10-11

Income is the lifeblood of retirement. In Part 1, wisdom from the early chapters of Jim Otar’s new book about retiree income challenges is explored. A one-person revolutionary.

Writing Rebound in Italian

Writing Rebound in Italian

2020-09-04

As the calendar turned to September, the US Centers for Disease Control and Prevention (CDC) issued new guidelines expanding and extending existing moratoriums previously put in place to stop evictions during the pandemic.

Tags: Estate Planning,Featured,Financial Planning,newsletter