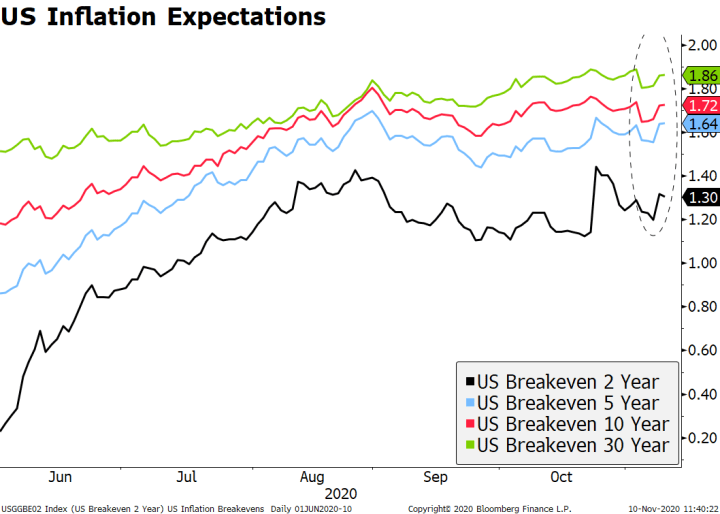

The interplay of a vaccine-driven reflation rally and the (likely) split government in the US are emerging as the driving themes for markets in the months ahead. We think reflation will win out in the end, but it could manifest itself differently this time around. While the policy-driven (fiscal and monetary) reflation theme from earlier in the year helped backstop the worst of the economic fallout, its reflationary impact was skewed towards asset price inflation. What if it’s different now? The pickup in US inflation breakeven hints at this possibility. If so, we may have a huge readjustment of Fed policy expectations in store. At stake is a massive sector rotation in global equities, a reconfiguration of the cross currents facing the dollar, and a huge new

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, developed markets, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The interplay of a vaccine-driven reflation rally and the (likely) split government in the US are emerging as the driving themes for markets in the months ahead. We think reflation will win out in the end, but it could manifest itself differently this time around. While the policy-driven (fiscal and monetary) reflation theme from earlier in the year helped backstop the worst of the economic fallout, its reflationary impact was skewed towards asset price inflation. What if it’s different now? The pickup in US inflation breakeven hints at this possibility. If so, we may have a huge readjustment of Fed policy expectations in store. At stake is a massive sector rotation in global equities, a reconfiguration of the cross currents facing the dollar, and a huge new force in fixed income markets. |

US Inflation Expectations, 2020 - Click to enlarge |

| As of this writing, markets are assuming a Biden presidency with a Republican Senate; we conform with the former, but we are not as convinced about the latter. Our understanding is that Trump doesn’t have enough arguments to bring a successful case to courts. Despite lingering Republican support, this issue should gradually fade away. On the Georgia Senate race, the landscape has changed so dramatically that it’s impossible to make any confident prediction. But Democrats are likely to feel invigorated by Biden and the absence of Trump to motivate turnout means Republicans will be on the defensive, in our view. In other words, the fabled Blue Wave is still very much a possibility.

Against this complex backdrop, here is how our thinking around some of the risks and main issues has evolved. (1) Investors might come around to the idea of a constructive relationship between Biden and the Republicans, but not before Georgia is resolved. This may sound farfetched at the height of the political drama and many Republicans still giving Trump the benefit of doubt for a contested election. But Biden has a good relationship with McConnell after years of working with him across the Senate aisle. Yes, Republicans will play the obstructionist long-game with an eye on the mid-term elections (and the Georgia Senate runoff), but there is plenty of room for a positive surprise down the line. With markets pricing in a minimal stimulus package, we think the risks are tilted towards a favourable outcome here, even with the vaccine news. Republicans will want to share the credit for the economic improvement that will come from a vaccine. |

. |

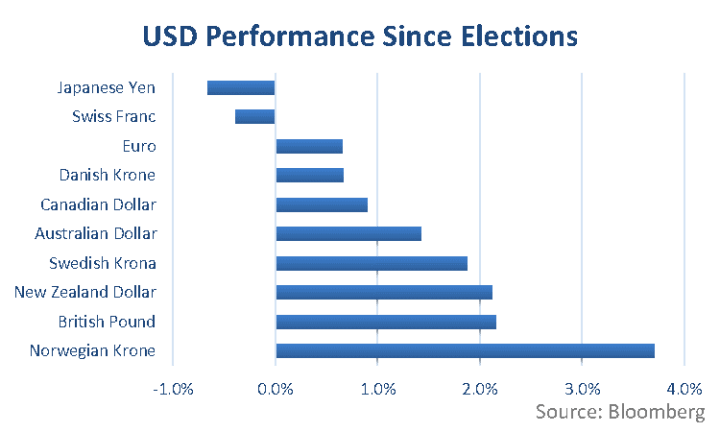

| (2) The Fed replaces fiscal stimulus as the ultimate backstop under a split government. If the economy falters, the Fed will save the day. So the punchbowl is half full again, but with another form of booze. The substitution of (potential) QE for fiscal stimulus has been an important driver for a weaker dollar (and higher gold and bitcoins) last week. Going forward, it means that the dollar impact of a big negative economic surprise will be a battle between risk aversion flows (dollar positive) and expected Fed easing (dollar negative). We expect the latter to prevail. In contrast, should the Democrats pull off a majority in the Senate, negative US economic news will be met with fiscal expenditure, which should be more effective in supporting growth, hence not as negative for the dollar (at least in the short term). |

USD Performance Since Elections - Click to enlarge |

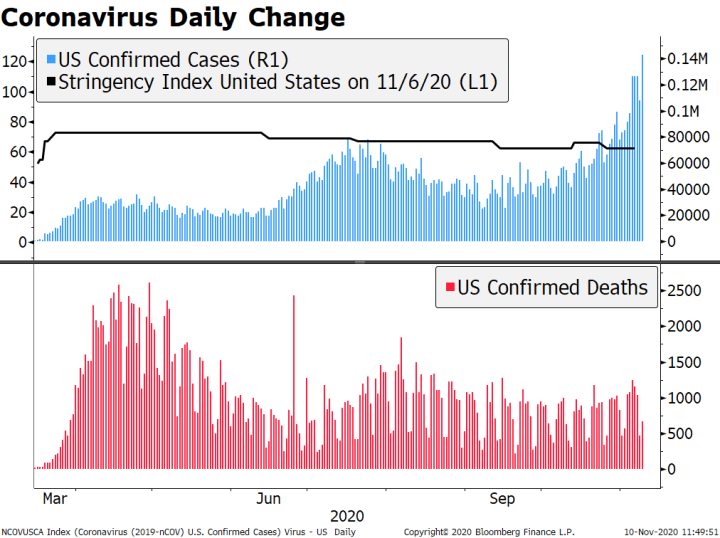

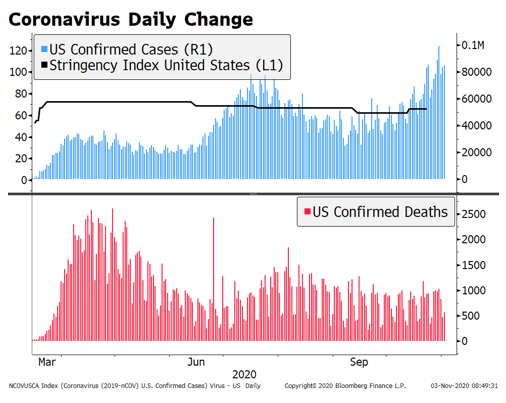

| (3) The US may fall behind the curve in the pandemic response with the transition of power. Biden is preparing a 12-member pandemic task force “built on a bedrock of science” that will “put our plan to control this virus into action.” The problem is that the Trump administration (and many elected Republican officials) may not cooperate. This could mean a worsening of the pandemic until the end of the year, forcing a more vigorous response by the Biden administration in terms of pushing for new restrictions. While this could be a longer-term positive for the US economic outlook, it would be a short-term negative. Here we assume that even if the Pfizer vaccine proves effective, the rollout will take time. |

Coronavirus Daily Change, 2020 - Click to enlarge |

|

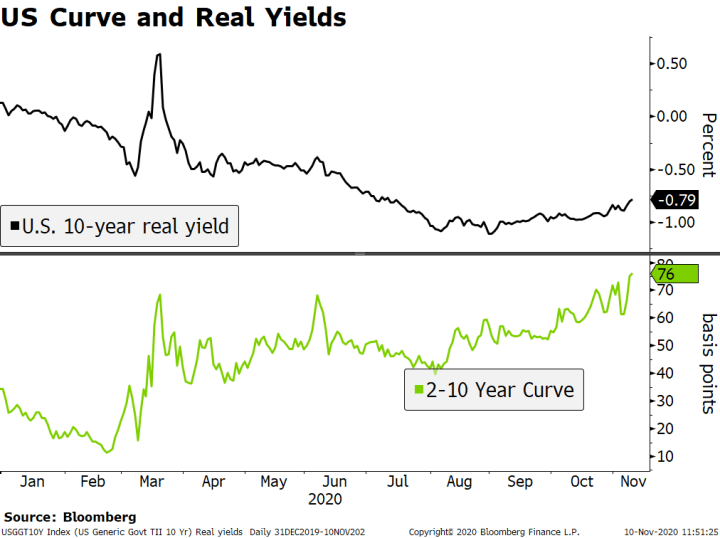

(4) The inflation shock scenario became more vivid, but still arguably under-priced. Imagine the combination of events: (1) Vaccine(s) are successfully being rolled out; (2) reopening is underway, consumer and corporate behaviour start to normalize; (3) Democrats win the Senate and seize the window to deliver stimulus and infrastructure spending; (4) dollar weakness provides an extra inflationary boost; and (5) markets grow concerned that Fed might fall behind the curve, having given up some degrees of freedom for announcing its new brand new average inflation targeting (AIT) framework. Even a more limited combination of these events is likely to require a substantial repricing in markets. For example, it could revive discussions of YCC by the Fed, or concerns about MMT. We would expect the Fed’s response to escalate over time, with jawboning the first line of defence, but it will be an awkward conversation to have with markets so soon after AIT. After that, adjustments to its QE would be the next line, with potential increases or shifts in the composition towards the long end. YCC should be seen as a very last resort. |

US Curve and Real Yields, 2020 - Click to enlarge |

You Might Also Like

Where Has All the Carry Gone?

Where Has All the Carry Gone?

Despite broad-based dollar weakness, EM currencies have not fully participated in the risk on environment that’s now in place. The good news is that fundamentals matter again. The bad news is that there are a lot of EM countries with bad fundamentals, and the secular decline in carry no longer gives these weaklings any cover.

The dollar is likely to remain under pressure after Powell’s dovish message at Jackson Hole. August jobs data Friday will be the data highlight of the week. The Fed releases its Beige Book report Wednesday; Powell will face many questions about the Framework Review that he unveiled at Jackson Hole.

ECB Preview

ECB Preview

The ECB meets tomorrow and is widely expected to stand pat. Macro forecasts may be tweaked modestly and there are some risks of jawboning against the stronger euro, but it should otherwise be an uneventful meeting. Looking ahead, a lot of room remains for further ECB actions.

Dollar losses are accelerating; the virtual IMF/World Bank meetings begin Monday. A big stimulus package before the election still seems unlikely; there are a fair amount of Fed speakers during this holiday-shortened week.

Some are holding out hope but we think the stimulus package remains dead; Fed releases its Beige Book report Wednesday; there is a full slate of Fed speakers this week. Fed manufacturing surveys for October will continue to roll out; weekly jobless claims will be reported Thursday; BOC releases results of its Q3 Business Outlook Survey Monday.

ECB Preview

ECB Preview

The ECB meets Thursday and is widely expected to stand pat until the next meeting. Macro forecasts won’t be updated until the December 10 meeting, but the bank will have to acknowledge the deteriorating outlook now.

FOMC Preview: Coronavirus Daily Change

FOMC Preview: Coronavirus Daily Change

The two-day FOMC meeting starts tomorrow and wraps up Thursday afternoon. While no policy changes are expected, we highlight what the Fed may or may not do. We expect a dovish hold, with Powell underscoring the growing downside risks facing the US economy in Q4.

The virus numbers in the US show no signs of slowing; the dollar should continue to soften. October retail sales Tuesday will be the US data highlight for the week; Fed manufacturing surveys for November will start to roll out; the Senate will hold a procedural vote this week to advance Judy Shelton’s nomination to the Fed Board of Governors.

Tags: developed markets,Featured,newsletter