Risk assets came under pressure last week as the virus news stream worsened. It’s clear that large parts of the US will be forced to delay reopening until their virus numbers improve. Markets had gotten too bullish on the US recovery story and so this reality check soured sentiment. This is a very important week for US data, and we think risk sentiment will remain under pressure ahead of what we think will be a likely downside surprise in the US jobs number Thursday. AMERICAS Brazil reports central government budget data Monday, where a primary deficit of -BRL132.1 bln is expected. Consolidated budget data will then be reported Tuesday, where a primary deficit of -BRL135.0 bln is expected. Fiscal policy will become an increasingly bigger issue, as Lower House

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, emerging markets, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Risk assets came under pressure last week as the virus news stream worsened. It’s clear that large parts of the US will be forced to delay reopening until their virus numbers improve. Markets had gotten too bullish on the US recovery story and so this reality check soured sentiment. This is a very important week for US data, and we think risk sentiment will remain under pressure ahead of what we think will be a likely downside surprise in the US jobs number Thursday. AMERICAS

![]() Brazil reports central government budget data Monday, where a primary deficit of -BRL132.1 bln is expected. Consolidated budget data will then be reported Tuesday, where a primary deficit of -BRL135.0 bln is expected. Fiscal policy will become an increasingly bigger issue, as Lower House Speaker Maia would not rule out the possibility of revising the government spending cap as pandemic costs pile up. June trade data will be reported Wednesday. May IP will be reported Thursday, which is expected to contract -21.9% y/y vs. -27.2% in April.

Brazil reports central government budget data Monday, where a primary deficit of -BRL132.1 bln is expected. Consolidated budget data will then be reported Tuesday, where a primary deficit of -BRL135.0 bln is expected. Fiscal policy will become an increasingly bigger issue, as Lower House Speaker Maia would not rule out the possibility of revising the government spending cap as pandemic costs pile up. June trade data will be reported Wednesday. May IP will be reported Thursday, which is expected to contract -21.9% y/y vs. -27.2% in April.

Chile reports May retail sales, unemployment, and IP Tuesday. Central bank minutes will be released Thursday. The bank left rates steady at 0.5% then but expanded its credit line facility for local banks to $16 bln in order to boost lending. It also announced a plan to buy $8 bln of central bank and bank bonds over the next six months and has hinted that it may eventually buy government debt. As such, these minutes will likely be very important.

Colombia central bank meets Tuesday and is expected to cut rates 50 bp to 2.25%. Minutes will be released Wednesday. June CPI will be reported Saturday, with headline expected to rise 2.48% y/y vs. 2.85% in May. If so, inflation would be the lowest since February 2014 and further below the 3% target. Central bank language after this meeting will be particularly important. Some believe the easing cycle may be ending but we think it will leave the door open for further easing.

EUROPE/MIDDLE EAST/AFRICA

South Africa reports Q1 GDP and May trade, budget, money, and credit data Tuesday. The economy is expected to contract -4.0% SAAR vs. -1.4% in Q4. Last week’s emergency budget was as bad as expected and suggests that fiscal stimulus will be very difficult to enact. As a result, monetary policy will bear most of the load going forward. Next policy meeting is July 23 and another cut is expected then. Q1 current account data will be reported Thursday, where the deficit is expected at -0.2% of GDP vs. -1.3% in Q4.

Turkey reports May trade data Tuesday. A deficit of -$3.4 bln is expected. June CPI will be reported Friday. Headline is expected to accelerate to 12.02% y/y from 11.39% in May. If so, it would be the second straight month of acceleration and the highest since February. No wonder the central bank surprised markets last week with no cut vs. 25 bp expected. It had cut at every meeting since the easing cycle started in July 2019. Next policy meeting is July 23. While rising price pressures may keep the bank on hold near-term, we think it is too early to call an end to the easing cycle.

Poland reports June CPI Tuesday. Headline is expected to rise 2.8% y/y vs. 2.9% in May. If so, inflation would be the lowest since November but remain in the top of the 1.5-3.5% target range. Next policy meeting was pushed back to July 14 from July 8 and no change is expected then. This delay pushed back the release of its inflation projections to July 17 from July 13. The bank just left rates steady this month after delivering a surprise cut in May. We believe the bank is in wait and see mode for the time being.

ASIA

Hong Kong reports May trade data Monday. Exports are expected to contract -5.2% y/y vs. -3.7% in April, while imports are expected to contract -7.0% y/y vs. -6.7% in April. Retail sales will be reported Tuesday. Sales in volume terms are expected to contract -33.7% y/y vs. -37.5% in April. Despite the recovery under way on the mainland, the Hong Kong economy remains depressed. There may be some modest relief in June as some reopening has been seen. However, the lackluster mainland recovery (see below) is likely to keep the Hong Kong recovery modest as well.

Korea reports May IP Tuesday, which is expected to remain steady at -4.5% y/y. June trade data will be reported Wednesday. Exports are expected to contract -7.3% y/y vs. -23.6% in May, while imports are expected to contract -9.4% y/y vs. -21.0% in May. June CPI will be reported Thursday, with headline expected to fall -0.2% y/y vs. -0.3% in May. Bank of Korea last cut rates 25 bp to 0.5% in late May but signaled that this was close to the effective lower bound. Governor Lee has said the bank is considering unconventional policies to support growth but gave no further details. Next policy meeting is July 16 and will be closely watched for clues.

China reports official June PMI readings Tuesday. Manufacturing is expected at 50.5 vs. 50.6 in May, while non-manufacturing is expected at 53.7 vs. 53.6 in May. Caixin manufacturing PMI will be reported Wednesday, which is expected to remain steady at 50.7. Caixin services and composite readings will be reported Friday, with services expected at 53.3 vs. 55.0 in May. If so, this would likely drag the composite lower from 54.5 in May. Despite manufacturing PMI readings moving back above 50 since March, the composite PMI only moved above 50 in May and signs suggest the overall recovery has been lackluster. Further stimulus seems likely.

Indonesia reports June CPI Wednesday. Headline inflation is expected at 1.85% y/y vs. 2.19% in May. If so, inflation would be the lowest since May 2000 and further below the 2.5-4.5% target range. Bank Indonesia just cut rates 25 bp to 4.25% this month. Next policy meeting is July 16 and another 25 bp cut is expected. Last week, the government approved a revised budget that lifted spending to a record $193 bln this year. Revenues are projected to drop and so the deficit is expected to widen to -6.3% of GDP.

Thailand reports June CPI Friday. Headline is expected to fall -3.00% y/y vs. -3.44% in May. If so, inflation would remain far below the 1-4% target range. Bank of Thailand last cut rates 25 bp to 0.50% in May and signaled that further cuts were unlikely. It left policy unchanged last week. Next policy meeting is August 5 and no change in rates is expected, but growing concern about the strong baht may lead to some measures to weaken the currency.

You Might Also Like

Recent Trade Developments Suggest Some Caution Ahead Warranted

Recent Trade Developments Suggest Some Caution Ahead Warranted

There’s never a good time for a trade war. Yet here we are on the cusp of one between the US and the EU over unfair aircraft subsidies and comes at a time when renewed COVID-19 outbreaks are making the global economic outlook even cloudier. These developments suggest some caution ahead is warranted for risk assets like EM and equities.

The spread of the coronavirus continues and is likely to weigh on risk assets and EM. Most markets in Emerging Asia are closed for all or part of this week due to the Lunar New Year holiday. China has extended the holiday until February 2 as it struggles to contain the virus.

Seven Big-Picture Considerations for Covid-19

Seven Big-Picture Considerations for Covid-19

Below is a non-exhaustive list of medium- and long-term implications from the Covid-19. We discuss the yuan, China’s competitiveness, its position in the global production chains, the impact on the Phase One trade deal, and rising financial stability risks. Globally, the virus will bring about a new wave of fiscal spending and revive the discussions about the limits of monetary policy.

Market sentiment is likely to open this week on an upswing after the Fed’s emergency rate cut and expanded QE were announced Sunday afternoon local time. Yet as we have seen time and again this past couple of weeks, added stimulus has had little lasting impact on markets as the virus numbers continue to worsen. Europe is now reporting more daily cases than China did at its peak. We remain negative on EM until the global growth outlook becomes clearer.

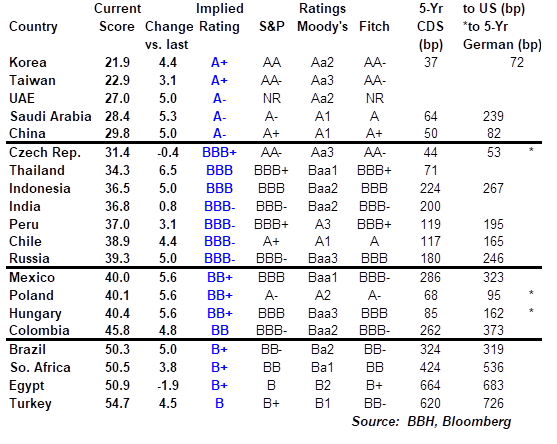

EM Sovereign Rating Model For Q2 2020

EM Sovereign Rating Model For Q2 2020

The major ratings agencies are punishing Emerging Markets (EM) credits much more than their DM counterparts. Our own sovereign ratings model suggests that there is still more pain to come.

We have produced this interim ratings model to assist investors in assessing relative sovereign risk across the major EMs.

Some Thoughts on Recent Foreign Exchange Intervention

Some Thoughts on Recent Foreign Exchange Intervention

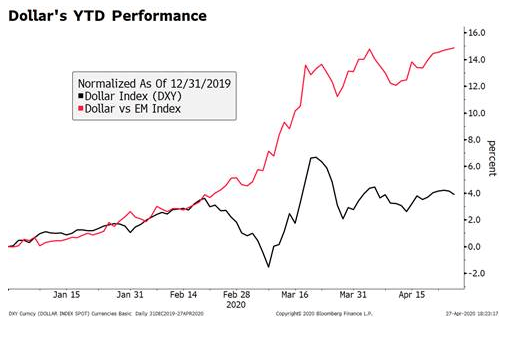

Dollar softness this week will take some pressure off of the foreign currencies but it’s too early to sound the all clear. This piece focuses on how central banks around the world may be intervening to influence their currencies. Most of the world, particularly EM, is grappling with supporting weak currencies but a select few are dealing with stronger currencies. This is a very opaque process and so we are simply making our best guesses.

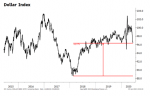

Our Latest Thoughts on the Dollar

Our Latest Thoughts on the Dollar

The dollar remains under pressure, due in large part to the Fed’s aggressive efforts to inject stimulus. We see dollar weakness persisting near-term. From a longer-term perspective, we note that the greenback remains largely rangebound and is unlikely to fall below its 2018 lows.

Weekly SNB Sight Deposits and Speculative Positions: After SNB Meeting

Weekly SNB Sight Deposits and Speculative Positions: After SNB Meeting

Update June 29, 2020: After SNB Meeting. Sight Deposits have risen by +2.9 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +2.9 bn. compared to last week.

Tags: Articles,Emerging Markets,Featured,newsletter