The virus news stream is negative today; the dollar is trying to build on its recent gains Weekly jobless claims are expected at 4.5 mln vs. 5.245 mln last week; regional Fed manufacturing surveys for April continue to roll out ECB confirmed reports that it will accept sub-investment grade debt as collateral; EU leaders will hold a video conference today Preliminary April eurozone PMI readings were awful; UK readings were even worse Japan reported weak preliminary April Japan PMI readings The dollar is mixed against the majors as global economic data continue to weaken. Nokkie and Kiwi are outperforming, while Swissie and euro are underperforming. EM currencies are also mixed. RUB and INR are outperforming, while HUF and RON are underperforming. MSCI Asia

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, Daily News, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

- The virus news stream is negative today; the dollar is trying to build on its recent gains

- Weekly jobless claims are expected at 4.5 mln vs. 5.245 mln last week; regional Fed manufacturing surveys for April continue to roll out

- ECB confirmed reports that it will accept sub-investment grade debt as collateral; EU leaders will hold a video conference today

- Preliminary April eurozone PMI readings were awful; UK readings were even worse

- Japan reported weak preliminary April Japan PMI readings

The dollar is mixed against the majors as global economic data continue to weaken. Nokkie and Kiwi are outperforming, while Swissie and euro are underperforming. EM currencies are also mixed. RUB and INR are outperforming, while HUF and RON are underperforming. MSCI Asia Pacific was up 0.8% on the day, with the Nikkei rising 1.5%. MSCI EM is up 0.4% so far today, with the Shanghai Composite falling 0.2%. Euro Stoxx 600 is up 0.2% near midday, while US futures are pointing to a lower open. 10-year UST yields flat at 0.62%, while the 3-month to 10-year spread is flat to stand at +53 bp. Commodity prices are mostly higher, with Brent oil up 7%, WTI oil up 11%, copper up 0.2%, and gold up 0.7%.

The virus news stream is negative today. Spain’s government extended the state of emergency to May 9. Singapore remain in focus as the case count rises further (over 1,000 yesterday). But perhaps the greatest surprise came from Trump’s comments reprimanding Georgia Governor Kemp’s decision to soften social-distancing. Earlier this week, Trump’s tweets were calling on many governors to “liberate” their states.

The dollar is trying to build on its recent gains. DXY is edging higher after a toehold above 100. It is trading at the highest level since April 7 and the next target is the April 6 high near 100.931. The euro is trading at the lowest level since March 25 and is on track to test the March 23 low near $1.0635. Elsewhere, sterling is holding up relatively better near the $1.2350 area and so the EUR/GBP cross is coming under renewed pressure. Lastly, USD/JPY remains stuck in narrow ranges just below the 108 area. We remain constructive on the dollar.

| AMERICAS

Weekly jobless claims are expected at 4.5 mln vs. 5.245 mln last week. If so, this would mean that nearly 27 mln have become jobless over the last five weeks, which is close to 18% of the labor force. Unemployment was 3.5% in February, just before the crisis. If we add these together, the US is likely already over 20% unemployment after barely over a month. May is unlikely to bring any relief. Note that this week’s claims data is for the BLS survey week that includes the 12th of each month. Keep an eye on the state-by-state readings, with data likely to continue showing that some of the key swing states are getting hit very hard. The regional Fed manufacturing surveys for April continue to roll out. Kansas City Fed survey will be reported and is expected at -37 vs. -17 in March. Last week, the Empire survey came in at -78.2 vs. -35.0 expected and -21.5 in March, while the Philly Fed survey came in at -56.6 vs. -32.0 expected and -12.7 in March. Markit also reports preliminary April US PMI readings. Manufacturing PMI is expected at 35.0 vs. 48.5 in March, while services PMI is expected at 30.0 vs. 39.8 in March. March new home sales (-15.8% m/m expected) will also be reported today. Mexico placed $6 bln in debt at relatively strong demand, especially given the recent downgrades. The 5-year issuance was priced to yield 4.125%, the 12-year at 5.0% and the 31-year at 5.5%. The sale was 4.75 times oversubscribed, but rates came in higher than previous sales, as has been the case with other EM borrowers. It’s no surprise that EM borrowers, especially oil producers, are facing challenges in the funding markets, but it’s important to remember that there is a lot of help available between the Fed swap lines and IMF/World Bank programs. This can help both with liquidity issues and as a bridge over the difficult economic times ahead. |

Mexico Bond and CDS, 2020 - Click to enlarge |

| EUROPE/MIDDLE EAST/AFRICA

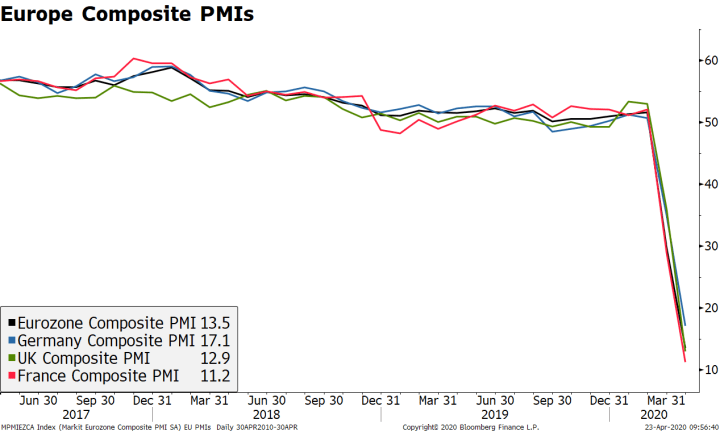

The ECB confirmed reports that it will accept sub-investment grade debt as collateral in its operations. To be eligible, however, the issuer had to be rated at least the lowest investment grade on April 7. The decision comes ahead of S&P’s scheduled review of Italy tomorrow, where the agency may decide on a sovereign downgrade. If this happens, corporate and financial sector bonds will also be downgraded along with the sovereign. Note that in the most recent update for Q2, our own sovereign ratings model shows Italy’s implied rating slipping into BB+ territory. There was no official statement about whether the ECB will buy these bonds through its asset purchase program, but we are confident they will if necessary. EU leaders will hold a video conference today to discuss its coronavirus response. The discussion now moves towards the rumored €2.2 trln economic stimulus plan. The plan would be funded by combination of budget spending and a new financing mechanism. However, joint debt issuance (coronabonds) still seems to be off the table. Separately, Germany is coming out with a new €10 bln stimulus package. It will include a temporary cut on VAT for certain businesses and wage support. The government expects the budget to widen by more than 7% this year, with growth falling by at least 5%. Preliminary April eurozone PMI readings were awful. Headline manufacturing PMI came in at 33.6 vs 38.0 expected and 44.5 in March, services PMI came in at 11.7 vs. 22.8 expected and 26.4 in March, and the composite came in at 13.5 vs. 25.0 expected and 29.7 in March. Looking at the country breakdown, Germany and France saw their composite readings dropping to 17.1 and 11.2 vs. 28.5 and 24.5 expected, respectively, with most of the damage seen in the services sector. Preliminary April UK PMI readings were even worse. Manufacturing PMI came in at 32.9 vs. 42.0 expected and 47.8 in March, services PMI came in at 12.3 vs. 27.8 expected and 34.5 in March, and the composite came in at 12.9 vs. 29.5 expected and 36.0 in March. CBI industrial trends for April were also reported, with all readings plunging further from March. |

Europe Composite PMIs, 2017-2020 - Click to enlarge |

ASIA

Japan reported weak preliminary April Japan PMI readings. Manufacturing PMI came in at 43.7 vs. 44.8 in March, services PMI came in at 22.8 vs. 33.8 in March, and the composite came in at 27.8 vs. 36.2 in March. Not surprisingly, the Cabinet Office said the economy was in an “extremely severe situation” and “getting worse rapidly” as it cuts its economic outlook for the second straight month. It added that the severe conditions were expected to continue as the impact of the pandemic spreads. Elsewhere, preliminary April Australia PMI readings were also reported. Manufacturing PMI came in at 45.6 vs. 49.7 in March, services PMI came in at 19.6 vs. 38.5 in March, and the composite came in at 22.4 vs. 39.4 in March.

You Might Also Like

Dollar Firm in Thin Holiday Trading

Dollar Firm in Thin Holiday Trading

The virus news stream is mostly positive today; yet risk assets are starting the week under some modest pressure. The dollar took a hit last week but we think it will recover; some US data releases from Good Friday are worth repeating. With most of Europe closed today, the news stream from the region is very light; oil prices could not extend their gains today after OPEC+ finalized output cuts over the weekend.

Dollar Under Modest Pressure as Europe Returns from Holiday

Dollar Under Modest Pressure as Europe Returns from Holiday

The tug of war between extending vs. softening lockdowns continues. The dollar remains under modest pressure but we think it will eventually recover; Bernie Sanders has endorsed Joe Biden. Europe reopens from holiday today but the news stream remains light; South Africa surprised with an emergency 100 bp rate cut.

Dollar Firm as Equities and Oil Start the Week Under Pressure

Dollar Firm as Equities and Oil Start the Week Under Pressure

The lockdown vs. opening debate continues in just about every country; the dollar is consolidating recent gains. Reports suggest the White House and House Democrats are nearing a deal on another aid package worth nearly $500 bln; the extra fiscal stimulus will add to downward ratings pressure on the US.

{kind=link}

The virus news stream remains mixed; oil remains at center stage with still extreme volatility. The White House and House Democrats struck a deal on a new aid package worth $484 bln. Canada reports March CPI; Mexico delivered a surprise 50 bp cut to 6.0% yesterday afternoon.

Tentative Stabilization

Tentative Stabilization

Risk-off continues in Asia, but moves have been less dramatic. European market jittery but stable. Implied rates now pricing in a full Fed cut by September. The UK will announce its decision on Huawei’s access to the country’s 5G network.

Dollar Firm Ahead of US Jobs Report

Dollar Firm Ahead of US Jobs Report

The number of confirmed coronavirus cases and deaths continue to rise; the dollar continues to climb. The January jobs data is the highlight for the week; Canada also reports jobs data. The Fed submits its semiannual Monetary Policy Report to Congress today; Mexico and Brazil report January inflation data.

Virus Concerns Resurface

Virus Concerns Resurface

Markets are reacting badly to upward revisions to coronavirus cases in China. The euro fell to the weakest level since mid-2017 against the dollar. UK housing data adds to relatively upbeat figures since the December elections. Malaysia’s government is joining in the counter-cyclical fiscal effort.

Dollar Firm as Global Financial Markets Calm

Dollar Firm as Global Financial Markets Calm

Global financial markets are finally seeing a measure of calm return; local Chinese media is sounding more confident that the situation is now under control. The White House will announce fiscal measures today; five states hold primaries and one holds a caucus with 352 total pledged delegates up for grabs.

Tags: Articles,Daily News,Featured,newsletter