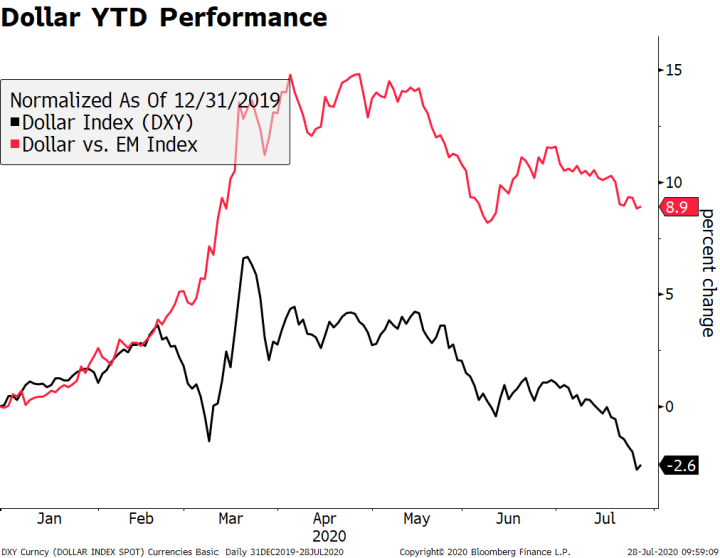

The dollar remains heavy; stimulus talks may or may not be dead; the White House is still sending mixed signals This is another quiet day in terms of US data; Canada reports September jobs data We got some more eurozone IP readings for August; following Greece yesterday, it’s Italy’s turn today to register another record low for its 10-year bond yield UK data came in significantly weaker than expected; Japan reported weak August real cash earnings and household spending Chinese assets had a strong re-opening after a week-long holiday, helped by a strong services PMI reading; India delivered a dovish hold, as expected The dollar remains heavy. DXY is trading at the lowest level since September 21 and is on track to test that day’s low near 92.749. A break below

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, Daily News, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

- The dollar remains heavy; stimulus talks may or may not be dead; the White House is still sending mixed signals

- This is another quiet day in terms of US data; Canada reports September jobs data

- We got some more eurozone IP readings for August; following Greece yesterday, it’s Italy’s turn today to register another record low for its 10-year bond yield

- UK data came in significantly weaker than expected; Japan reported weak August real cash earnings and household spending

- Chinese assets had a strong re-opening after a week-long holiday, helped by a strong services PMI reading; India delivered a dovish hold, as expected

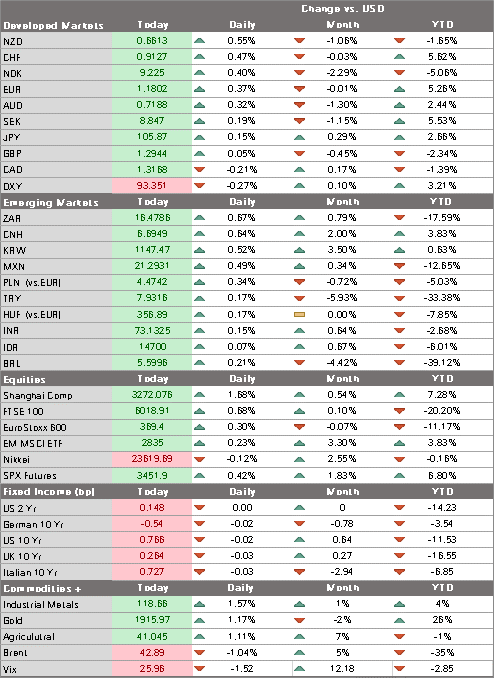

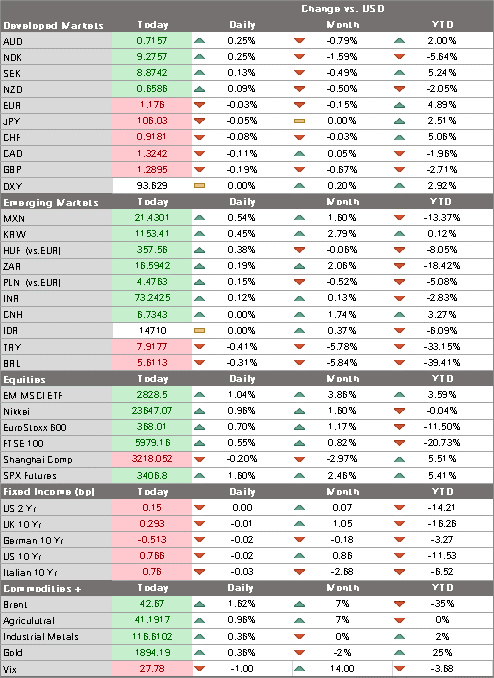

The dollar remains heavy. DXY is trading at the lowest level since September 21 and is on track to test that day’s low near 92.749. A break below would set up a test of the September 1 low near 91.746. The euro is testing the $1.18 area and a break above would set up a test of the September 21 high near $1.1870. After that, the next target would be the September 1 high near $1.2010. Sterling is having trouble breaking above the $1.30 area with Brexit still hanging over the UK. Lastly, USD/JPY is trading back below 106 area after trading above it this week for the first time since September 14.

| AMERICAS

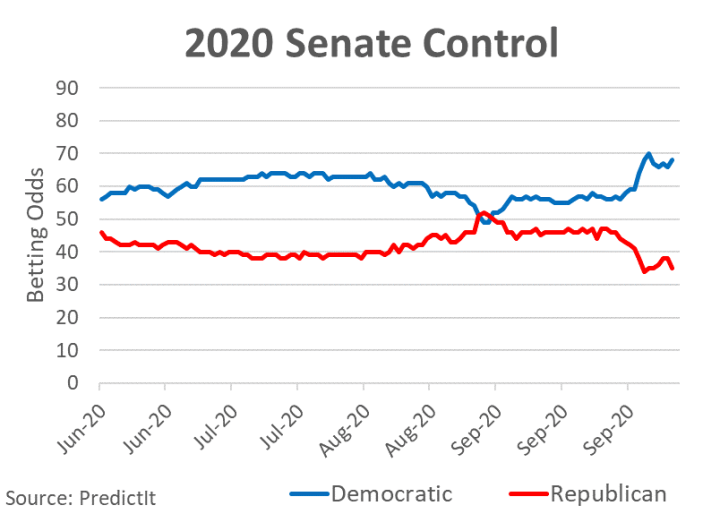

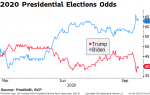

Stimulus talks may or may not be dead. House Speaker Pelosi said there will be no standalone bill to support airlines or any other industry without a broader aid plan. She added that she’s hopeful for more stimulus but noted that she has yet to get a full counteroffer for the last $2.2 trln package passed by the House. Our take is that Trump blinked first and now Pelosi feels she has the upper hand. It remains to be seen how she plays it. We think she wants to get a big deal done so she is likely taking a hardline stance now to extract more concessions from the Republicans. The two sides remain far apart and so we are skeptical that a deal can be reached. Stay tuned. The White House is still sending mixed signals. Treasury Secretary Mnuchin reportedly told Pelosi that Trump wants an agreement on a comprehensive stimulus package. However, White House spokesperson Alyssa Farah later said, “we’ve made very clear we want a skinny package,” though she later said the administration is “open to going with something bigger” but reiterated opposition to the $2.2 trln plan passed by House Democrats. It is remarkable to us that a party that is down in the polls so much ahead of an election is resisting fiscal stimulus. Besides possibly losing the presidency, Republicans may also lose control of the Senate as betting odds are giving Democrats a near 70% chance of taking the Senate. This is another quiet day in terms of US data. August wholesale trade sales and final wholesale inventories will be reported. The only Fed speaker is Barkin. Fed officials have been unified this week in calling for more fiscal stimulus. Without another aid package, the US economy faces even stronger headwinds on top of the rising virus infections. This economic underperformance is likely to continue feeding into dollar underperformance. Canada reports September jobs data. A gain of 150k is expected, down from 245.8k in August but still strong. Unemployment is seen falling to 9.8% from 10.2% in August. USD/CAD is trading at its lowest level since September 18 and a break of the 1.3155 area would set up a test of the September 1 low near 1.2995. |

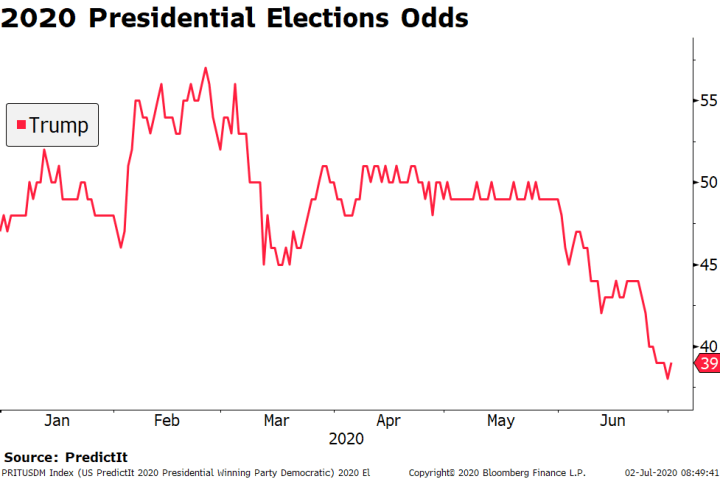

2020 Senate Control - Click to enlarge |

| EUROPE/MIDDLE EAST/AFRICA

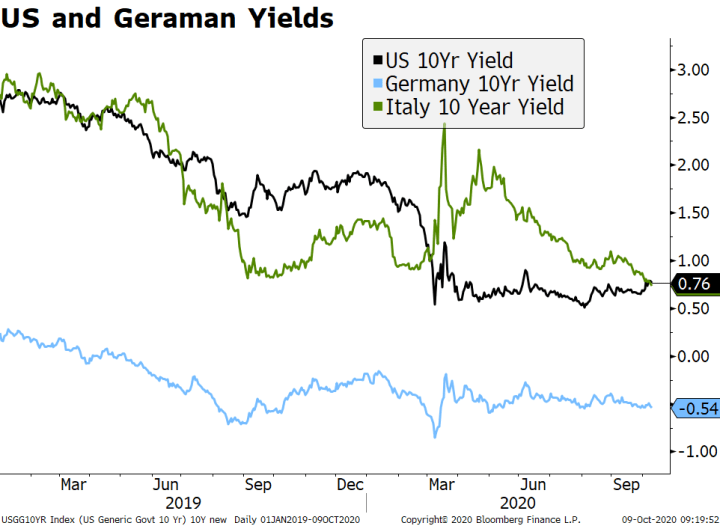

We got some more eurozone IP readings for August. France’s rose 1.3% vs. 1.7% expected while Italy’s jumped 7.7% vs. 1.4% expected. Eurozone aggregate IP for August will be reported next Wednesday and is expected to rise 0.6% m/m vs. 4.1% in July. Earlier this week, Germany IP came in weaker than expected at -0.2% m/m while Spain came in slightly better than expected. Momentum in Europe is clearly slowing, which supports our view that the ECB will add more stimulus before year-end. Following Greece yesterday, it’s Italy’s turn today to register another record low for its 10-year bond yield. Also, the Italian 10-year around 0.75% is now lower than the US 10-year Treasury for the first time since the pandemic started taking its grip on markets. There seems to be quite a few tailwinds in play from ECB buying to positive political news. Recall last month the ruling alliance scored an important victory in local elections against opposition forces led by Matteo Salvini. UK data came in significantly weaker than expected. August GDP, IP, construction output, services index, and trade were all reported. GDP rose 2.1% m/m vs. 4.6% expected, IP rose 0.3% m/m vs. 2.6% expected, construction output rose 3.0% m/m vs. 5.0% expected, and services rose 2.4% m/m vs. 5.0% expected. What’s worse, the July readings revised lower. Looking ahead to this fall, a more abrupt deceleration may be seen when many government support programs end. Viral infections are surging, which makes the need for further fiscal and monetary support even greater. We continue to expect the BOE to increase its asset purchases before year-end. |

US and Germany Yields, 2019-2020 - Click to enlarge |

| ASIA

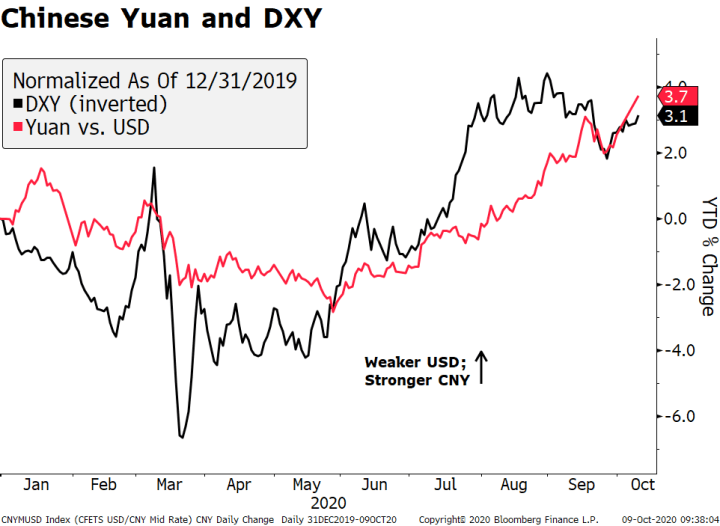

Japan reported weak August real cash earnings and household spending. Earnings fell -1.4% y/y, as expected and compares to a revised -1.5% (was -1.3%) in July. Elsewhere, spending fell -6.9% y/y vs. -6.7% expected and -7.6% in July. The savings rate rose to 44% in the five months through August this year, up from 33% for the same period in 2019. Overall, recent data suggest the economy is improving slightly but still facing strong headwinds. We continue to expect another slug of fiscal stimulus from new Prime Minister Suga in the coming months. Chinese assets had a strong re-opening after a week-long holiday, helped by a strong services PMI reading. The Shanghai Comp was up 1.6% today and the spot CNY appreciated over 1% to the strongest level since April 2019. The yuan has an appreciated about 3.5% this year, but the move has been largely in line with the broad dollar trend. The news flow from China remains supportive. The Caixin services PMI for September ticked higher to 54.8 vs. 54.3 expected and 54.0 in August. Elsewhere, reports from the Tourism Agency claim that travel during the holiday has normalized about 80%. When all is said and done, the mainland economy remains on firm footing and is leading the recovery in the region. |

Chinese Yuan and DXY, 2020 - Click to enlarge |

| Reserve Bank of India delivered a dovish hold, as expected. It kept the repo rate steady at 4.0%. However, the bank doubled the amount of open market bond purchases to INR200 bln, offered to buy state debt, and provided cheap long-term funding to banks to invest in corporate bonds and commercial paper. Governor Das said the bank would remain accommodative “as long as necessary, at least through the current financial year and into the next year to revive growth on a durable basis and mitigate the impact of Covid-19 while ensuring that inflation remains within the target going forward.” The bank cuts its GDP forecast for the current FY to – 9.5%, the first official forecast since the pandemic hit. Das hinted at further rate cuts, which we think are likely in the coming months. |

. |

You Might Also Like

Dollar Soft Ahead of Jobs Report

Dollar Soft Ahead of Jobs Report

Re-shutdowns continue to spread across the US; the dollar has come under pressure again. Jobs data is the highlight ahead of the long holiday weekend in the US; weekly jobless claims will be reported. FOMC minutes were revelatory; the Fed for now will rely on “outcome-based” forward guidance and asset purchases to achieve its goals; US House passed the latest China sanctions bill.

Dollar Rangebound in Quiet Start to an Eventful Week

Dollar Rangebound in Quiet Start to an Eventful Week

Today marks a relatively quiet start to what is likely to be one of the most eventful weeks we’ve seen in a while; the dollar remains within recent well-worn ranges. The US continues to ratchet up trade tensions; the only US data report today is the June budget statement.

Dollar Stabilizes but Further Losses Likely

Dollar Stabilizes but Further Losses Likely

The dollar is stabilizing today but further losses are likely. Senate Republicans have proposed a sharp cut to weekly unemployment benefits; Senator Collins will oppose Judy Shelton’s nomination to the Fed. Regional Fed manufacturing surveys for July will continue to roll out; early July reads for the US economy support our view that Q3 is off to a rocky start.

Dollar Bounce Ends Ahead of ECB Decision

Dollar Bounce Ends Ahead of ECB Decision

The dollar rally ran out of steam; US Senate will hold a vote today on its proposed “skinny” bill. US reports August PPI and weekly jobless claims; US will sell $23 bln of 30-year bonds today after a sloppy 10-year auction yesterday

BOC delivered a hawkish hold yesterday; Peru is expected to keep rates steady at 0.25%.

Dollar Soft as Markets Ignore Virus Numbers and Switch to Risk-On Mode

Dollar Soft as Markets Ignore Virus Numbers and Switch to Risk-On Mode

Virus numbers are rising across Europe and the US; the dollar is softening as risk-off sentiment ebbs. It is a fairly quiet day in the US; there is a glimmer of hope about a fiscal deal in the US; recent US data support the widely held view that more stimulus is needed.

Dollar Softens as Risk-Off Sentiment Ebbs

Dollar Softens as Risk-Off Sentiment Ebbs

The dollar continues to soften as risk-off sentiment ebbs; the first presidential debate will take place tonight. House Democrats have staked out their latest position at $2.2 trln; there is a fair amount of US data out today; Brazil has come under renewed pressure from fiscal concerns.

Dollar Softens and US Curve Steepens as Odds of Democratic Sweep Rise

Dollar Softens and US Curve Steepens as Odds of Democratic Sweep Rise

The dollar remains under pressure; the US curve continues to steepen; a compromise on fiscal stimulus before the election still seems unlikely; this is another quiet day in terms of US data. President Lagarde said the ECB is prepared to inject fresh monetary stimulus to support the recovery; we expect the ECB to increase its PEPP in Q4.

Dollar Remains Heavy as Markets Await Fresh Drivers

Dollar Remains Heavy as Markets Await Fresh Drivers

The US Vice Presidential debate was a comparatively cordial affair, though the impact on the election is likely to be limited; polls continue to move in favor of Biden, including in swing states. The weak dollar narrative under a Democratic sweep continues to play out; the outlook for fiscal stimulus is as cloudy as ever; FOMC minutes contained no big surprises.

Tags: Articles,Daily News,Featured,newsletter