Two days ago, when a platoon of clueless CNBC hacks said that stocks were extremely undervalued, and must be bought (on their fundamentals, not because the Fed was about to nationalize the entire bond market and is set to start buying equity ETFs in the next crash), we showed just how “undervalued” the market was. That’s when Credit Suisse chief equity strategist Jonathan Golub – usually one of the most bullish Wall Streeters – published a chart showing that any “temporary” cheapness in stocks hit in late March was long gone for the simple reason that forward earnings have plunged. As a result, as of noon on March 7, when the S&P 500 had risen as much as 22% from March 23 lows, forward stock multiples had surged right back 19.0x. Why is this notable? Because as

Topics:

Tyler Durden considers the following as important: 3.) Swiss Banks, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Two days ago, when a platoon of clueless CNBC hacks said that stocks were extremely undervalued, and must be bought (on their fundamentals, not because the Fed was about to nationalize the entire bond market and is set to start buying equity ETFs in the next crash), we showed just how “undervalued” the market was.

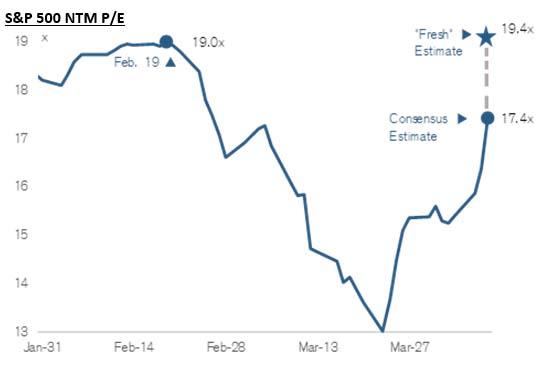

That’s when Credit Suisse chief equity strategist Jonathan Golub – usually one of the most bullish Wall Streeters – published a chart showing that any “temporary” cheapness in stocks hit in late March was long gone for the simple reason that forward earnings have plunged. As a result, as of noon on March 7, when the S&P 500 had risen as much as 22% from March 23 lows, forward stock multiples had surged right back 19.0x. Why is this notable? Because as Golub wrote, “this is the same level the S&P500 held on Feb 19, the all-time high.” In other words, at the start of the week stocks were valued the same as they were at the February all time highs. Fast forward to today when the Fed’s latest “shock and awe” nuclear bomb announcement which included purchases of junk bond ETFs and muni debt – and by implication terminally disonnects risk prices from any fundamental values and instead only the size of the Fed’s balance sheet matters – sent the S&P as high as 2,818. |

S&P 500 NTM, January-March 2020 - Click to enlarge |

| And, in doing so, the forward PE multiple on the S&P has risen from the record 19.0x reached in February to a new all time high of 19.4x.

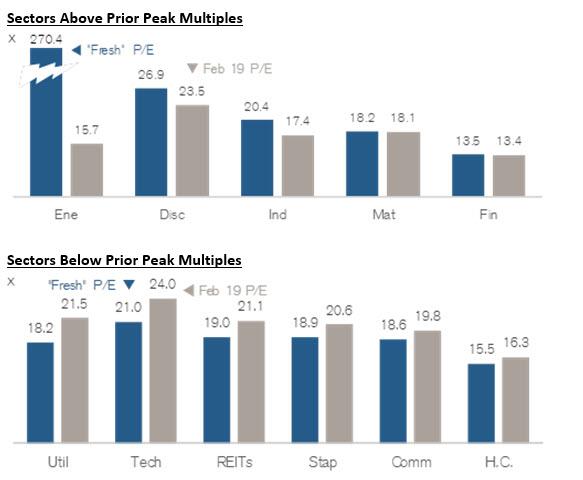

In other words, the market has never been more overvalued than it is right now. That’s not all. As Golub writes today, “we’ve expanded this analysis to cover sectors and sub-groups. Multiples for cyclical groups (Energy, Materials, Industrials, Discretionary, Financials) have surpassed prior P/Es. Valuations for defensive sectors (Staples, Utilities, Health Care, REITs) as well as Tech and Communications remain below Feb 19 levels.” |

Sectors Peak Multiples - Click to enlarge |

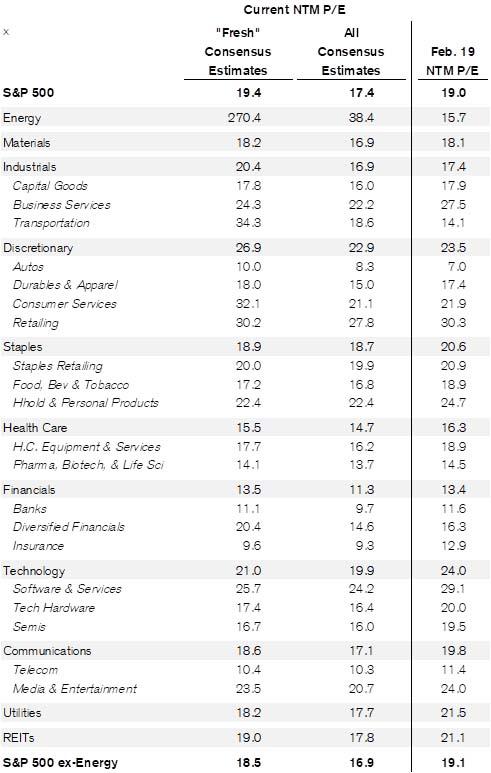

| And a full sector breakdown.

So congratulations Jerome Powell: you have succeeded in the impossible – with the US economy entering a depression, with US GDP set to plunge as much as 50%, with US unemployment already 15% and set to hit 20% or more, the Fed chair has single-handedly disconnected stocks from all fundamental anchors and made the S&P the most overvalued in history as its forward P/E hits the highest number ever recorded. |

Record high valuation - Click to enlarge |

You Might Also Like

Swiss economy could lose up to CHF35 billion to pandemic

Swiss economy could lose up to CHF35 billion to pandemic

Coronavirus will cost the Swiss economy CHF22 billion ($22.7 billion) in lost productivity in the best-case scenario, economists have warned. Losses could easily mount up to CHF35 billion between March and June. A nationwide lockdown of non-essential high street shops and services has been accompanied by partial closures of industrial plants in some cantons.

Fragile, Not Fortified

Fragile, Not Fortified

On Sunday, Argentina’s government announced it was postponing payment on any domestically-issued debt instruments denominated in foreign currencies. That means dollars, just not Eurobonds. At least not yet. In response, ratings agencies such as Fitch declared the maneuver a distressed debt exchange.In other words, technically a default.

Dollar Firm as Europe Fails to Deliver

Dollar Firm as Europe Fails to Deliver

The dollar is stabilizing; reports suggest the White House is developing a plan to reopen the US economy sooner rather than later. Both Hong Kong and Singapore just tightened restrictions on gathering and movement. FOMC minutes for the March 15 decision will be released today.

Nothing Is What It Seems

Nothing Is What It Seems

My latest interview about Corona, Liberty, Private Property, Authoritarism, and a fear-mongering global media campaign, which I call borderline criminal

[embedded content]

Why Mexico Is Reluctant to Shut Down Its Economy to Combat COVID-19

Why Mexico Is Reluctant to Shut Down Its Economy to Combat COVID-19

Mexico’s president Andrés Manuel López Obrador has been reluctant to impose mandatory "social distancing" orders on the Mexican population. According to USNews, López Obrador "has maintained a relaxed public attitude" toward COVID-19, and the Mexican government did not impose a ban on "non-essential" work until March 30, long after health officials in other countries insisted Mexico must do so.

Jp Cortez joins Phillip Kennedy on Kennedy Financial

Jp Cortez joins Phillip Kennedy on Kennedy Financial

Sound Money Defense League Policy Director Jp Cortez joins Phil Kennedy of Kennedy Financial to discuss sound money on the state and federal level, and the harms of inflation.

Buy The Tumor, Sell the News

Buy The Tumor, Sell the News

The fictitious valuation of the stock market will eventually re-connect with reality in a violent decline. No, buy the tumor, sell the news ™ is not a typo: the stock market is a lethal tumor in our economy and society.

All of the Economic Recovery Models Will Be Wrong Too

All of the Economic Recovery Models Will Be Wrong Too

“All of the projection models were wrong. All of them,” admitted New York Governor Andrew Cuomo in an interview last week with MSNBC. Governor Cuomo had been issuing frantic demands for tens of thousands of ventilators… that turned out not to be needed as the rate of new hospitalizations for COVID-19 infections in New York plunged with surprising speed.

Tags: Featured,newsletter