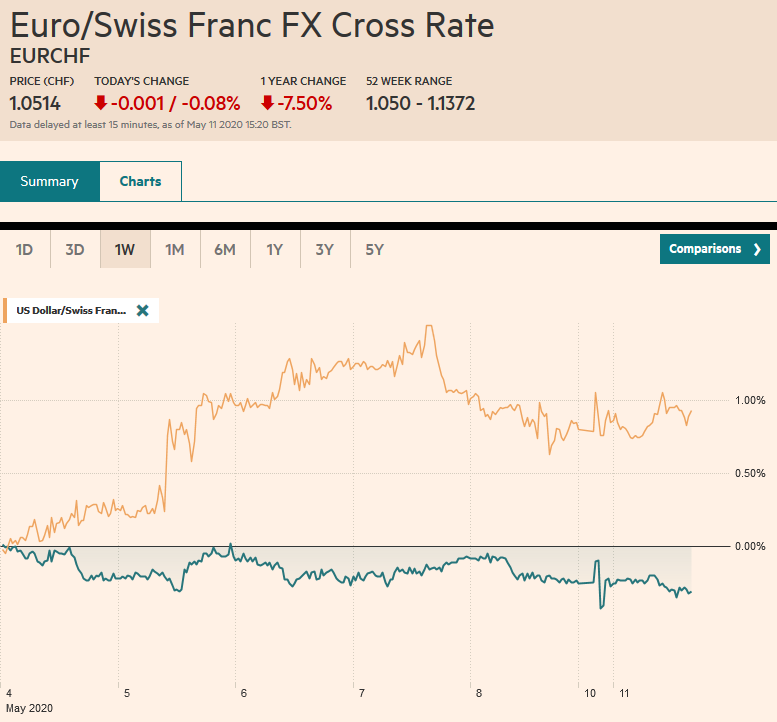

Swiss Franc The Euro has fallen by 0.08% to 1.0514 EUR/CHF and USD/CHF, May 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The new week begins slowly in the capital markets. Many markets in the Asia Pacific region, including Japan, Hong Kong, and Australia, gained over 1%, but European and US shares are heavier. Benchmarks off all three regions rallied by 3.4%-3.5% over the past two weeks. Bond markets are also little changed, with the US 10-year benchmark just below 70 bp ahead of this week’s record refunding. Core European yields are slightly higher, while the peripheral premiums have edged in. The dollar begins the new week firmer across the board, with the New Zealand dollar and Japanese yen the

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, Currency Movement, Featured, Italy, Mexico, newsletter, South Korea, Turkey, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.08% to 1.0514 |

EUR/CHF and USD/CHF, May 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The new week begins slowly in the capital markets. Many markets in the Asia Pacific region, including Japan, Hong Kong, and Australia, gained over 1%, but European and US shares are heavier. Benchmarks off all three regions rallied by 3.4%-3.5% over the past two weeks. Bond markets are also little changed, with the US 10-year benchmark just below 70 bp ahead of this week’s record refunding. Core European yields are slightly higher, while the peripheral premiums have edged in. The dollar begins the new week firmer across the board, with the New Zealand dollar and Japanese yen the weakest, off around 0.5%. Except for a handful of mostly currencies from smaller Asian countries, most emerging market currencies are also beginning the week with a heavier tone. Gold is a little lower as it tests $1700, and July WTI is heavy near $25.50 after stalling near $28 last week. |

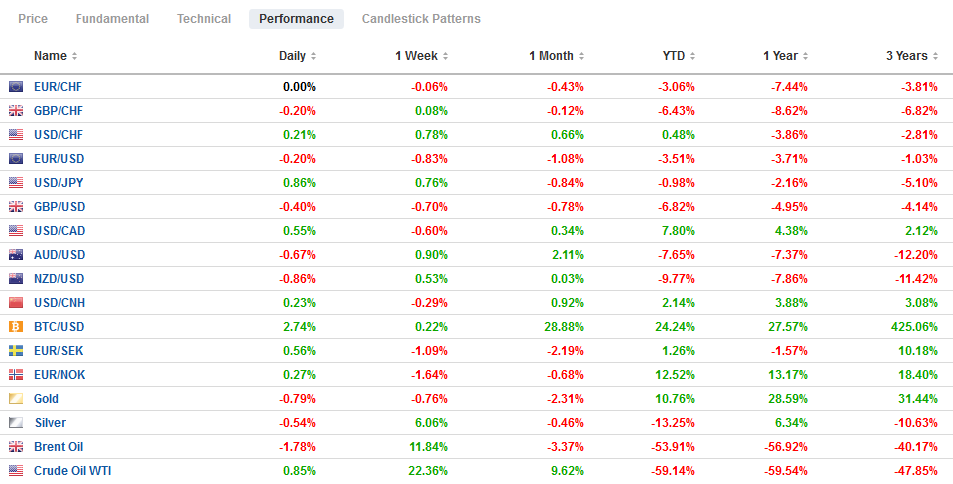

FX Performance, May 11 - Click to enlarge |

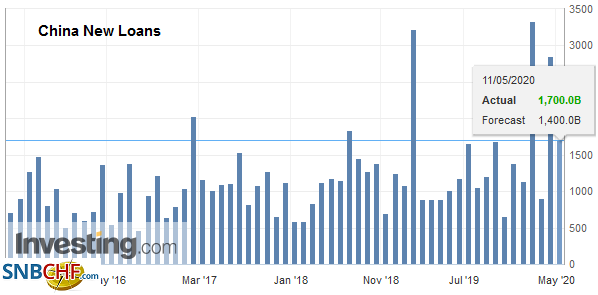

Asia PacificChina’s aggregate financing rose by nearly CNY3.1 trillion last month, a little stronger than most economists expected after a CNY5.1 trillion increase in March. The annual growth rate accelerated to 12% from 11.5% and is the highest in two years. |

China New Loans, April 2020(see more posts on China New Loans, ) Source: investing.com - Click to enlarge |

| The main catalyst was bonds issued by and lending to local governments, which is the vehicle of China’s stimulus, not the central government. Separately, the PBOC’s quarterly monetary policy statement promised more powerful policies to promote growth and job. What it did not say was also important: it did not repeat pledges about avoiding excess liquidity. Many expect new initiatives after the National People’s Congress in about ten days. |

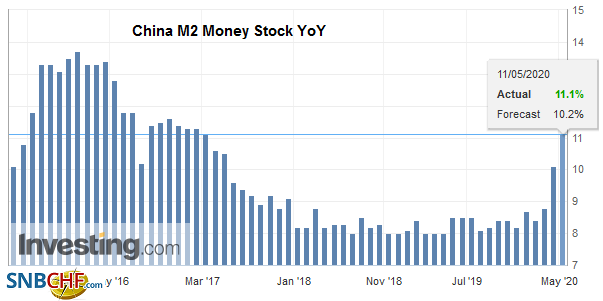

China M2 Money Stock YoY, April 2020(see more posts on China M2 Money Stock, ) Source: investing.com - Click to enlarge |

South Korea’s reported exports in the first ten days of May slumped 46.3% from a year ago. That followed a 24.3% decline last month. Average daily exports fell by a little more than 30%. Exports to the US were off almost 55%, while shipments to the EU were off 50.6%. Exports to China fell by 29.4%. In terms of products, the exports of semiconductor chips and wireless devices fell by 17.8% and 35.9%, respectively. Imports were off 37.2%, but the imports of chip fabrication equipment rose by almost 70%.

Since Japanese markets re-opened from the Golden Week holiday on May 7, the dollar has risen in all three sessions. The greenback bottomed last week just below JPY106.00. It climbed steadily in Asia and reached almost JPY107.30 in the European morning, its highest level since May 1. Initial resistance is seen near JPY107.50 then JPY108.00. Intraday technicals are stretched. A close below JPY107 would be disappointing. The Australian dollar’s gains were extended to $0.6560, just shy of the rebound high (~$0.6570 on April 30) but have reversed lower to test the $0.6500 area in Europe. A break, and ideally a close below, the pre-weekend low of about $0.6490, would be another opportunity to try picking a top. At the least, it may signal a test of $0.6400. The dollar rose by about 0.2% against the Chinese yuan to about CNY7.09 and remains within the range seen in recent weeks.

Europe

Moody’s did not change its credit assessment of Italy or Greece’s sovereign ratings at the end of last week. Moody’s gives Italy the lowest investment-grade rating. Recall that the ECB has indicated that it would ignore rating downgrades until September 2021. Moreover, the ECB accepts the highest rating of the top four agencies. DBRS gives Italy a high BBB rating. However, before the weekend, it cut the trend (outlook) to negative from stable, citing the deterioration of the government’s balance sheet.

The fallout from the German Constitutional Court ruling last week continues. Over the weekend, EU President von der Layen threatened to sue Germany over the verdict. The ECB is undeterred. The German court did not rule on the Pandemic Emergency Purchase Program, a 750 bln euro effort that is not bound by the capital key. However, press reports indicate that lawsuits are being prepared. Separately, ECB President Lagarde estimates that EMU members will be issuing 1-1.5 trillion of new bonds. Most seem to expect the ECB to expand its PEPP buying in the upcoming meetings by 250-500 bln euros.

The euro remains pinned near $1.08, where a nearly 900 mln option is set to expire today. There is also an option at $1.0850 for one billion euros that also will be cut today. Between the two, it likely marks the range. Sterling is finding support around $1.2350 in the European morning, and the intraday technicals are stretched, suggesting potential for a bounce in early North American activity. Initial resistance is seen near $1.2400. The dollar is slipping against the Turkish lira following the reversal of last week’s decision to ban three banks (Citi, UBS, and BNP).

America

The implied yield of the December 2020 Fed funds futures rose by 2.5 bp ahead of the weekend to pop back above zero, despite the simply dreadful jobs data. The yields through May 2021 also moved out of negative territory. Federal Reserve officials have repeatedly rejected such a course. Fed Chairman Powell will discuss “current economic issues” on the internet on Wednesday and is expected to push back against such speculation. Some hedgers may seek protection from the low probability but high impact possibility. Others might look at it as on a risk-reward basis, without attaching any special value attached to the zero bound. It is just “betting” on the chances of another rate cut. At the same time, the Federal Reserve signals that it recognizes that financial conditions are continuing to improve as it reduces the amount of Treasuries it will purchase this week will be $7 bln a day, down from a peak of $75 bln a day. Meanwhile, after the employment data, the Atlanta and NY Fed GDP trackers were revised sharply lower for Q2 to -34.9% and -31.2%, respectively.

The data highlight this week include the US April CPI retail sales (tomorrow) and retail sales and industrial production figures (Friday). The week, the US Treasury sells more than $90 bln in coupons for its quarterly refunding, which includes a 20-year bond. Canada has a light calendar, while the highlight of Mexico’s is the central bank meeting on May 14. The overnight rate is at 6.0% now, and at least a 50 bp cut is likely to be delivered. Ahead of the meeting, Mexico reports March industrial output (expect around a 4% decline on the month) and April job creation (after a loss of 130.6k jobs in March).

Before the weekend and again today, the US dollar found good bids near CAD1.3900. Initial resistance is seen near CAD1.40, which is about the middle of the recent range. The Canadian dollar is more sensitive to the risk environment (equities) than the price of commodities (oil proxy). Near MXN23.55, the US dollar was at the lower end of its recent range against the peso. After falling for the last two sessions, the greenback is firm. Initial resistance is seen near MXN24.00 and then MXN24.15.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

Overview: The ring of containment of Covid-19 has grown from China. The new frontline is Japan, South Korea, Italy, and Iran. A lockdown of around 50k people near Milan and Austria blocking trains from Italy is scaring investors. Asian markets fell, but South Korea bore the brunt with a nearly 4% decline. The national holiday in Japan spared local equities.

FX Daily, April 29: Heavy Dollar amid Month-End Pressure

FX Daily, April 29: Heavy Dollar amid Month-End Pressure

Overview: The dollar is lower across the board as dealers attribute the selling to month-end pressures ahead of the FOMC today and ECB tomorrow and long-holiday weekend for many. Japan’s Golden Week holiday has already begun. Despite the loss in US equities yesterday, despite the higher opening, it has not spilled over, as Alphabet earnings helped lift sentiment.

FX Daily, May 7: China Reports an Unexpected Jump in Exports, While Norway Surprises with a Rate Cut

FX Daily, May 7: China Reports an Unexpected Jump in Exports, While Norway Surprises with a Rate Cut

Overview: There is a sense of indecision in the air today. There have been several developments, but investors seem mostly reluctant to extend positions. China reported a surge in exports in April and an increase in the value of reserves. Australia reported a rise in exports in March. The Bank of England left policy steady, but clearly signaled it was prepared to boost its asset purchases.

FX Daily, May 8: Jobs and Negative Fed Funds Futures

FX Daily, May 8: Jobs and Negative Fed Funds Futures

Overview: The S&P 500 closed near its session lows for the third day running yesterday but failed to deter the bulls in Asia-Pacific, where most markets rose by more than 1%. Taiwan, Korea, and Australia lagged a bit though closed higher. Europe’s Dow Jones Stoxx 600 is firm, and the modest gains (~0.5%) would be enough to ensure a higher weekly close if it can be maintained.

FX Daily, February 19: Investors’ Confidence Snaps Back

FX Daily, February 19: Investors’ Confidence Snaps Back

Overview: After shunning risk yesterday, investors re-entered the fray today, and the animal spirits returned. The MSCI Asia Pacific Index snapped a four-day slide, and China’s markets were among the few losers in the region today. Europe’s Dow Jones Stoxx 600 recovered yesterday’s losses in full and is again at record highs. US shares are also trading firmer and are poised to recoup yesterday’s decline.

FX Daily, February 25: Capital Markets Remain Fragile after Yesterday’s Bloodletting

FX Daily, February 25: Capital Markets Remain Fragile after Yesterday’s Bloodletting

Overview: Yesterday’s bloodletting in global equities has calmed, but investors remain on edge. Despite all the concerns that the markets were under-appreciating the implications of the new coronavirus, there is a sense that yesterday’s moves were in excess. Japanese markets, which were closed on Monday, played catch-up today, and the Nikkei shed 3.3%.

FX Daily, February 26: Dramatic Investor Adjustment Continues

FX Daily, February 26: Dramatic Investor Adjustment Continues

Overview: The warning by the US Center for Disease Control and Prevention that Americans should prepare for an outbreak of Covid-19 sent the S&P 500 tumbling to an 11-week low and the 10-year Treasury yield to a record low near 1.30%. The volatility of the S&P (VIX) jumped to its highest level since 2018. The sell-off in global equities continues unabated.

FX Daily, May 4: Monday Blues

FX Daily, May 4: Monday Blues

Overview: The constructive mood among investors in April has given way to new concerns as May gets underway. Japan and China are still on holiday, but most of the other markets in Asia fell, led by 4.5%-5.5% declines in Hong Kong and India, and more than 2% in most other local markets. Australia bucked the trend a gained 1.4% after shedding 5% before the weekend.

Tags: #USD,China,Currency Movement,Featured,Italy,Mexico,newsletter,South Korea,Turkey