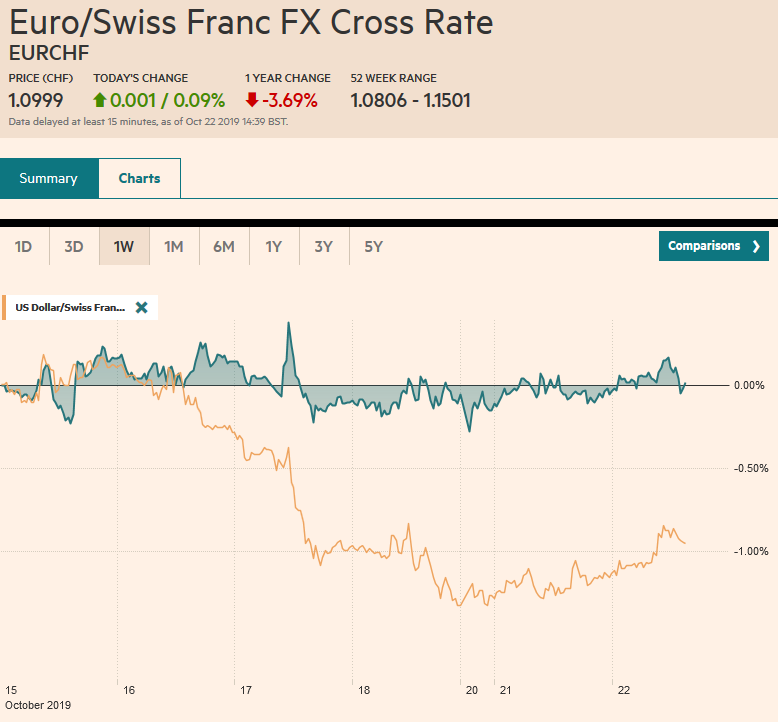

Swiss Franc The Euro has risen by 0.09% to 1.0999 EUR/CHF and USD/CHF, October 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Bismark is said to have warned that laws were like sausages, and to respect them, one ought not to see how they are made. The UK had a non-binding referendum more than three years ago, and although it won by 52%-48% and the party leaders committed to adhering to the results, it still cannot figure out how to leave. Prime Minister Johnson was dealt another setback in the House of Commons yesterday, but sterling remains near its highs as many hold on to the hope that the deal will eventually be approved. Asia Pacific shares were firm, though Tokyo markets were closed for a national

Topics:

Marc Chandler considers the following as important: 4) FX Trends, 4.) Marc to Market, Brexit, Canada, Chile, Currency Movement, EUR/CHF, Featured, FX Daily, newsletter, USD, USD/CHF

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Swiss FrancThe Euro has risen by 0.09% to 1.0999 |

EUR/CHF and USD/CHF, October 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Bismark is said to have warned that laws were like sausages, and to respect them, one ought not to see how they are made. The UK had a non-binding referendum more than three years ago, and although it won by 52%-48% and the party leaders committed to adhering to the results, it still cannot figure out how to leave. Prime Minister Johnson was dealt another setback in the House of Commons yesterday, but sterling remains near its highs as many hold on to the hope that the deal will eventually be approved. Asia Pacific shares were firm, though Tokyo markets were closed for a national holiday. South Korea’s Kospi led the advance, gaining over 1%, while India and Singapore were notable exceptions. The corrective pressures, we anticipated are evident in Europe, where the Dow Jones Stoxx 600 is paring yesterday’s gains, and US shares are trading softly. Yesterday was the seventh session in which the S&P 500 has alternated between gains and losses, gaining around 1% over the sawtooth run. A loss today keeps the pattern intact. Benchmark yields rose yesterday and are unwinding the gains today, leaving 10-year yields 3-5 bp lower. The US dollar is mostly firmer against the major currencies. Here the yen and New Zealand dollar are showing residual strength. Emerging market currencies are mixed, though the Turkish lira, perhaps helped by official action, and the Indian rupee are leading the advancers with about 0.3% gains. Central European currencies are heavy with the Hungarian forint’s 0.25% loss setting the pace, ahead of the central bank meeting (deposit rate is minus 5 bp, and the central bank rate is at 90 bp). December WTI is trading quietly, slipping a fractionally lower. Its 20-day moving average is near $53.70, and it has not been surpassed on a closing basis in nearly a month. Gold is firm but remains below $1500. |

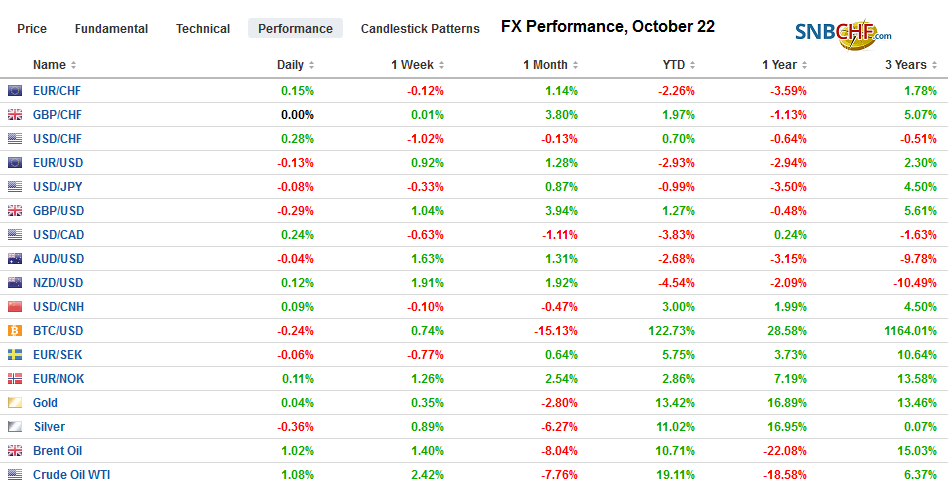

FX Performance, October 22 - Click to enlarge |

Asia Pacific

In a quiet session, the main talking point is the People’s Bank of China injecting CNY250 bln (~$35 bln) of liquidity into the banking system a day after leaving the newly introduced loan prime rate unchanged. The PBOC’s injection, like last week’s, appears designed to help prevent stress ahead of the corporate tax payment at the end of the month. Officials continue to signal a reluctance to provide large-scale economic stimulus despite forecasts that growth will slow below 6% next year.

Indications from China that the trade talks are proceeding was taken as a sign by US President Trump that it really wants a deal. However, the more China is said to want it, the more parts of the Administration want to press for more. Commerce Secretary Ross played the “bad cop,” insisting that the timing of the agreement was not as important as its content. Economic adviser Kudlow held out the possibility that a “phase one” agreement could lead to the suspension of the next set of US tariffs that have been threatened for the middle of December. During this third tariff freeze, the US has continued to press China on other fronts, including blocking the quota reform at the IMF, which would have increased the PRC’s voting weight. US Vice President Pence’s speech on Thursday is awaited for fresh signs of the Trump Administration’s intent. He has often taken a hardline on China.

The dollar is softer in the JPY108.30-JPY108.95 range that has confined it for several sessions. Although it remains in the upper end of the larger range, the technical indicators warn the market may soon give up hope of pushing through JPY109, and some of the late dollar longs (yen shorts) may be cut. It may take a break of the JPY108 area to confirm this. The 20-day moving average is just below there, and there is an $820 mln option struck there that expires today. The Australian dollar made a marginal new one-month high, but as we noted yesterday, the technical indicators were warning of a near-term setback. A break of $0.6840 would confirm the near-term high is in place, and a close below it warns of a potential test on $0.6785-$0.6800. The dollar has been extremely stable against the Chinese yuan in recent days. It set to close within the CNY7.75-CNY8.20 range for the fourth consecutive session.

Europe

UK Prime Minister Johnson struck a deal with the EU last week by surrendering a redline that the previous government insisted on–no hard border in the Irish Sea, separating Northern Ireland from the rest of the UK. Without a majority, he faces a House of Commons that is still smarting from his attempt to pull an end-run around it and his willingness to leave the EU without an agreement.Speaker Berkow prevented Johnson from breaking convention by requiring that the House of Commons vote on virtually the same bill on Monday. Two votes will be held later today. The first is a vote on the general principles of the Withdrawal Agreement (“second reading”} followed by a procedural motion that would expedite the process of approving the set laws necessary to implement the new agreement. The Letwin Amendment passed Saturday was aimed at avoiding a no-deal at the end of the month. The risk was that Johnson’s Agreement could be approved, but the implementation of it could have been rejected, leading to the crash-out. A loss of this procedural vote would shift the focus back to the EC to grant a delay. The procedural bill is subject to amendments, and this is where the opposition will make a stand, seeking the UK to remain in the customs union with Northern Ireland and/or require a confirming referendum. Faced with amendments, Johnson could pull the bill and seek a snap election.

Despite scare tactics, there is little reason why the EC would not grant an extension, especially given a commitment to hold new elections. There is some sense of Brexit exhaustion, and to be clear, the divorce agreement (still think amputation is a better metaphor for what is happening after all the UK is part of Europe) does not end it. Brexit will be a gift that keeps giving. A new relationship will still need to be negotiated during the near standstill transition period. The failure to reach an agreement in those talks could still see the UK-EU return to WTO rules. Meanwhile, votes about the Queen’s Speech, which is ostensibly why Johnson had improperly sought to suspend Parliament for five weeks, were supposed to take place this week, and no timeframe has been given.

Two forces are in ascendancy in Europe, and neither is nationalistic populism. The first, as we noted yesterday, environmental issues have supplanted immigration is a more salient issue for many Europeans. Second, there is recognition that fiscal policy is needed to boost aggregate demand, and that monetary policy is not sufficient. There are pockets of resistance, of course, but the thrust of the new European Commission will likely review and modify its stance toward fiscal expansion. This was the message from the new Economics and Financial Affairs Commissioner (as of November 1), former Italian Prime Minister Gentiloni (replacing Moscovici). Italy itself will be a crucial litmus test. The 2020 budget was submitted belatedly last week. It projects the structural deficit (adjusted for growth) to expand by 0.1% instead of shrinking by 0.6%, as previously indicated. There may be a gentle push back, seeking clarification of intentions, but not the acrimonious affair seen in the recent past.

The euro reached almost $1.1180 yesterday, its best level in nearly two months, before coming off.Some follow-through selling extended the pullback a little through $1.1135 in early European turnover. The five-day moving average is a touch lower (~$1.1130), and the euro has not closed below it in two-weeks. This is cited not so much as a support area but as a mile mark of the recent uptrend.Late longs seem vulnerable ahead of the flash PMI data and ECB meeting on Thursday. That said, we expect a small increase in composite PMI and for the ECB, of course, not to unveil new initiatives after last month’s broad moves. Sterling is trading well within yesterday’s ranges as many participants lack near-term conviction, apparently content to see how the parliamentary process plays out shortly today.

America

Canada’s Prime Minister Trudeau looks to stay in Ottawa another term. His Liberal Party narrowly lost its majority, winning about 156 seats in the 338-member lower chamber. This will force a coalition, most likely with the New Democrats, which won about 24 seats. A potential area of disagreement is oil pipeline policies, with the New Democrats being more green than the Liberals. Separately, Canada reports August retail sales figures today. The median forecast from the Bloomberg survey expects a 0.4% increase, which would match the July rise. It looks to be mostly autos, and without which retail sales could be flat. Our bias is to shade the consensus to the downside slightly. The Bank of Canada will also release the results of its survey, including senior loan officers.

The US sees the Richmond Fed manufacturing survey. The Bloomberg survey shows expectations for improvement after the -9 reading in September, but the other regional surveys have disappointed. The US also reports September’s existing-home sales. The August pace of 5.49 mln was the highest since March 2018. While sales are expected to have slowed a little in September, they are expected to remain well above last September’s 5.18 mln pace. Judging from the derivatives market, expectations for a Fed rate cut next week consider it a nearly done deal.

The US dollar fell CAD1.31 yesterday for the first time in three months. Follow-through selling extended the greenback’s dollar loss toward CAD1.3070 in early Asia before the consolidating. We look for it to test the CAD1.3100-CAD1.3130 band. The dollar is trapped near its two-day lows against the Mexican peso near MXN19.10.Mexico reports September unemployment figures today, but they are not typically market-movers. The MXN19.00-level has not been seen since the end of July. We think risk-reward considerations auger against chasing the dollar lower now. We anticipated a dollar bounce toward MXN19.20-MXN19.25. Lastly, we note that protests in Santiago, Chile (where next month’s APEC meeting is to be held) weighed on the Chilean peso and equity market yesterday. The dollar jumped almost 2.15% against the peso, the most in at least several years. The high for the year was set at the start of the month a little above CLP731 and finished yesterday slightly above CLP7.27. Some fear a disruption of copper, but there is little reflection of this in the futures market so far.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,Canada,Chile,Currency Movement,EUR/CHF,Featured,FX Daily,newsletter,USD/CHF