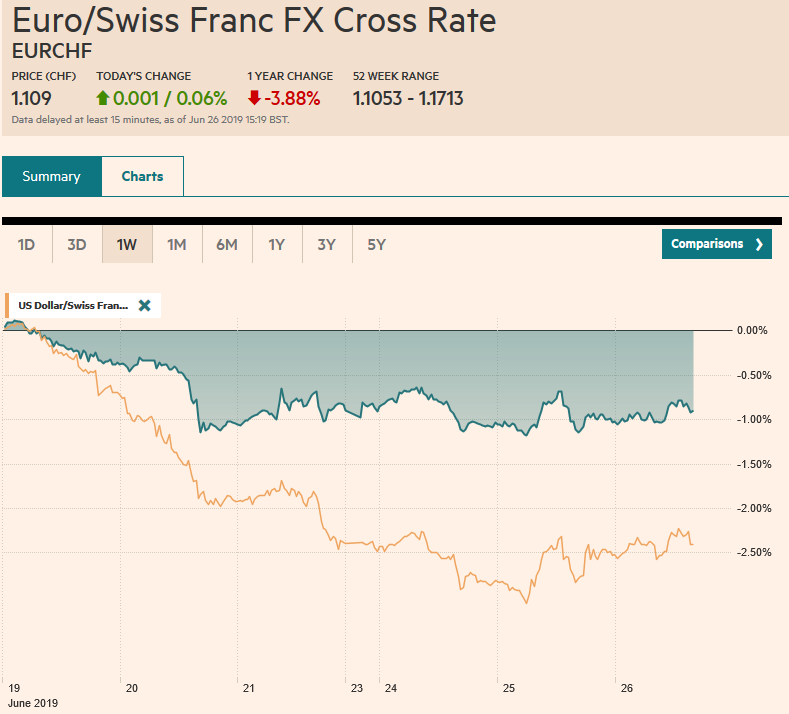

Swiss Franc The Euro has risen by 0.06% at 1.109 EUR/CHF and USD/CHF, June 26(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The S&P 500 fell nearly one percent yesterday, its steepest fall this month and this was a weight on Asia Pacific and European activity. Most markets have eased, though not as much as the US did. Hong Kong, India, and Singapore were notable exceptions in Asia, where the MSCI benchmark slipped for a second day. Led by health care and real estate, Europe’s Dow Jones Stoxx 600 is off for the fourth consecutive session. US shares have stabilized, but the gap created by the sharply higher opening on June 18 (~2897.3-2905.4) may still draw

Topics:

Marc Chandler considers the following as important: 4) FX Trends, Canada, China, EUR/CHF and USD/CHF, Featured, Italy, newsletter, USD

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Swiss FrancThe Euro has risen by 0.06% at 1.109 |

EUR/CHF and USD/CHF, June 26(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The S&P 500 fell nearly one percent yesterday, its steepest fall this month and this was a weight on Asia Pacific and European activity. Most markets have eased, though not as much as the US did. Hong Kong, India, and Singapore were notable exceptions in Asia, where the MSCI benchmark slipped for a second day. Led by health care and real estate, Europe’s Dow Jones Stoxx 600 is off for the fourth consecutive session. US shares have stabilized, but the gap created by the sharply higher opening on June 18 (~2897.3-2905.4) may still draw prices. Benchmark 10-year yields are one-two basis points firmer, while the US dollar is narrowly mixed in quiet turnover. The euro, sterling, and yen have softer profiles, while the New Zealand dollar is the strongest of the majors following the unsurprising decision by the central bank to keep rates steady. The Australian dollar has moved up in sympathy, but the RBA is widely expected to cut next week. The liquid accessible emerging market currencies (e.g., South Africa rand, Turkish lira, and Mexican peso) are firmer, while the Indonesian rupiah is ending a six-day rally. Gold pulled back to near the $1400 breakout level but recovered but is still set to snap its six-day surge. A large drawdown in US oil inventories, according to the industry estimate is boost oil prices. August WTI pushed briefly pushed above $59 a barrel for the first time this month. |

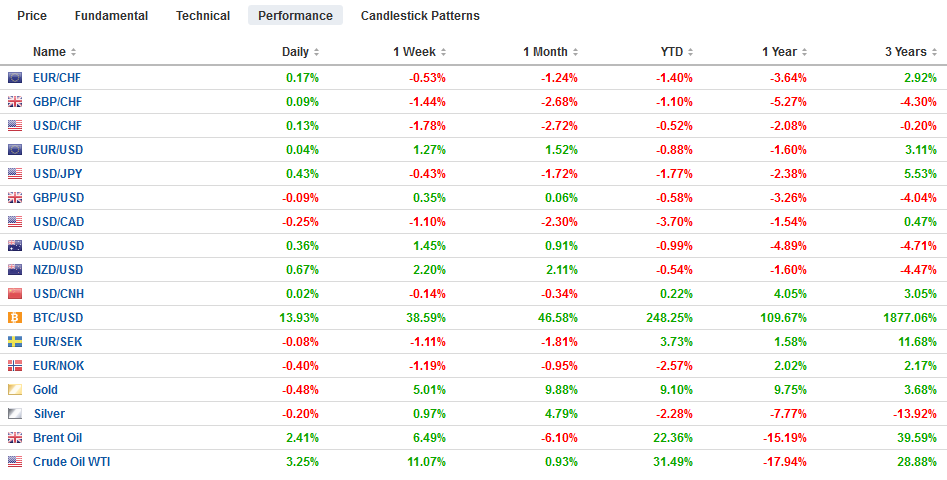

FX Performance, June 26 - Click to enlarge |

Asia Pacific

Ever since Canada agreed to cooperate with the US over the Huawei executive, it has been the recipient of China’s ire. China had arrested a couple Canadians and taken some trade action (canola and pork). As of today, it is halting the importation of meat from Canada, ostensibly for finding trace elements of a banned additive and there was a problem with some forms. The Huawei officer was wanted to violating the embargo against Iran, but usually, such violations are punished by a fine, not an arrest. Moreover, given that Trump has politicized the case by claiming it could be resolved in a trade agreement, Canada would seem to have the cover to turn down the US request.

The market had discounted about a one-in-five chance that the Reserve Bank of New Zealand would cut rates earlier today. It passed on the opportunity but issued a dovish statement that suggested that the downside risks posed by the international considerations would lead to another rate reduction later this year. The market continues to price in about an 80% chance of a cut at the next meeting, August 7. The Reserve Bank of Australia meets on July 2 and interpolating from the OIS suggest 80% of a 25 bp cut has been discounted. Note that since the middle of May when the US two-year premium over Australia peaked just beyond 105 bp, the spread has fallen to 80-85 bp as US rates fall faster than Australia’s.

The dollar has recovered against the yen after falling to almost JPY106.75 yesterday. It has been bumping up against JPY107.50 in Asia and the European morning. There are some chunky option expirations today: JPY107 for $2 bln, JPY107.30 for $1.3 bln, JPY107.50 for $1.2 bln, and JPY107.70 for about $615 mln. The dollar had forged a shelf earlier this month near JPY107.75-JPY107.85, and that offers good resistance now. The Australian dollar is at its best level in a couple of weeks as it draws near $0.7000. The month’s high was set closer to $0.7025. It seems vulnerable ahead in the second half of the week as the buying is likely to dry up ahead of RBA meeting. The Chinese yuan edged higher for the first time this week. The dollar has held below CNY6.90 for the fifth session.

Europe

News from Europe is light. There are two main talking points today. First, Brexit and the prospects of a no-deal exit continue to be discussed. Johnson, who is favored to win the Tory leadership contest, has indicated that his first steps, such as renegotiating the Withdrawal Bill and jettisoning the backstop for the Irish border have been rejected. If that doesn’t work, Johnson suggests invoking a little-used WTO rule (Article 24) that would obligate continued free-trade. The EU and the WTO says the rule does not apply. That leaves Johnson’s ultimate strategy as ” Do or Die. Come what may.” The UK will leave on Oct 31. However, even some Tory MPs aim to block a no-deal exit, and PredictIt.Org has only about a one-in-three chance that the UK leaves then.

The other talking point is Italy. The EC does not want a confrontation with Italy. It would play into the anti-EU camp’s hands. There is speculation that the EC may find a face-saving resolution this year, but it is next year’s budget that will likely be the source of new tension. The League’s Salvini is insisting on a flat tax, which implies a tax cut, and it is not clear how it would be financed. Many observers who argue that Italy has the output gap that justifies more fiscal stimulus do not seem to appreciate that investors will demand higher interest rates for fiscal stimulus given the country’s large debt legacy and that the risk is that the higher rates offset the fiscal stimulus. This practical problem seems more potent than the theoretical constructs of non-observable economic variables.

The euro has been unable to distance itself from yesterday’s lows (~$1.1345). It is vulnerable to additional selling in North America today. Support is likely to be seen in the $1.1300-$1.1325 area. There is a 1.8 bln euro at $1.13 that expires today. The upside also appears blocked by options. There are roughly four billion euro is in expiring options struck between $1.1375 ad $1.1390. Sterling slipped to a new low for the week near $1.2665, after posting a potential key reversal yesterday (new highs for the move were recorded before sterling sold off and closed below the previous session’s low). There are about GBP480 mln in $1.2645-$1.2660 options that will be cut today. The former corresponds to a 50% retracement of sterling’s recovery from the June 18 low just above $1.25.

America

Fed officials have not told us anything new. Powell himself was explicit. His comments were intended to sketch out the Fed’s thinking, as expressed last week. More officials think a reduction of interest rates will be needed than thought so a month ago. At the same time, Powell explained that he did not want to overreact. This seems to argue against the 50 bp that Minneapolis Fed President Kashkari advocated. The sole vote in favor of an immediate rate hike from the decision to keep rates on hold, the first dissent under Chair Powell, Sr. Louis Fed President Bullard was straightforward. He favors a 25 bp move, not a 50 bp cut. Yet, according to the CME’s model, the fed funds futures market continues to price in about a 25% chance of a 50 move at the end of next month. This seems way too high, given an economy that still appears to be growing faster than the Fed’s estimate of the trend even if slower than in the first quarter. Job growth has also slowed, but it is still quick enough to keep the unemployment rate at a generation low and to pull down the underemployment rate. Inflation is below target, but it is not that far from it. As Dallas Fed President Kaplan noted this week, financial conditions are robust. Richmond Fed’s Barkin noted that policy was already mildly accommodative.

The most likely outcome of the Trump-Xi talks is a renewed tariff freeze. Any more than that is not reasonable given the level of discord and the wide range of conflicting interests. Rather than ease China’s fear that the US is committed to holding it back–to containing it–, actions and statements by the Trump Administration have justified these concerns. Although Trump thought that a speech by Vice President Pence that was bound to be critical of China’s human rights, was too aggressive, blacklisting a few companies for helping develop China’s supercomputer a week before the talks are nothing short of an affront.

China closes the technology gap the same way the US did in the 19th century, and the US (and the world) understandable do not approve. It attempts to build it itself, and the US tries to block it. At the same time, President Xi is not a reformer and is not pursuing policies associated with what former President Hu Jintao dubbed “peaceful development,” which prompted the US to call China a “responsible stakeholder.” The ideological bias of many Americans leads them to conclude that Communism is monolithic and they, therefore, miss the opportunities that exist precisely because there forces of order and forces of movement in China as there are in the US, and that China also changes over time.

The US reports May durable goods orders and the preliminary estimate of May’s trade balance for goods. These are probably not the data that will sway Fed officials. The personal consumption report due at the end of the week is more important and the jobs data on July 5 (early estimates are around 165k (vs. 75k in May and a six-month average of about 175k) as seen as key. Canada’s calendar is light, while Mexico reports May unemployment figures today after a better than expected April retail sales report yesterday. The US dollar is extending its decline against the Canadian dollar today, and it is now at its lowest level in almost four months. We suspect that if the US dollar has not recorded the session low near CAD1.3140, it has come pretty close. The dollar rose for the past three sessions against the Mexican peso but is coming in better offered today. The MXN19.12-MXN19.15 provides initial support.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Canada,China,EUR/CHF and USD/CHF,Featured,Italy,newsletter