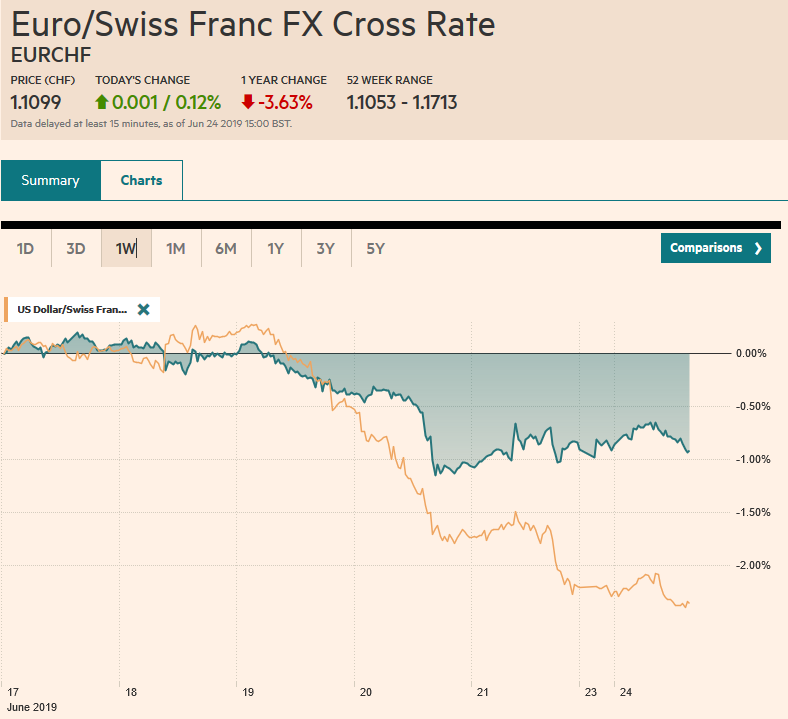

Swiss Franc The Euro has risen by 0.12% at 1.1099 EUR/CHF and USD/CHF, June 24(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The Trump-Xi meeting at the G20 this coming weekend and heightened tensions in the Gulf, with the US set to impose new sanctions on Iran’s crippled economy are keeping investors on edge. News the opposition won the re-do of the Istanbul mayoral election has lifted the Turkish lira. Most of the major Asia Pacific equity markets, including the Nikkei, Shanghai Composite, the Kospi, and Australia’s ASX were modestly higher, while Europe’s Dow Jones Stoxx 600 was a little heavier but looking for direction. US shares are trading with a

Topics:

Marc Chandler considers the following as important: 4) FX Trends, China, EUR/CHF and USD/CHF, Featured, Germany, Germany Business Expectations, Germany IFO Business Climate Index, Iran, newsletter, Russia, Turkey, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.12% at 1.1099 |

EUR/CHF and USD/CHF, June 24(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The Trump-Xi meeting at the G20 this coming weekend and heightened tensions in the Gulf, with the US set to impose new sanctions on Iran’s crippled economy are keeping investors on edge. News the opposition won the re-do of the Istanbul mayoral election has lifted the Turkish lira. Most of the major Asia Pacific equity markets, including the Nikkei, Shanghai Composite, the Kospi, and Australia’s ASX were modestly higher, while Europe’s Dow Jones Stoxx 600 was a little heavier but looking for direction. US shares are trading with a firmer bias in Europe. Asia Pacific benchmark 10-year yields pushed higher, but European bonds have continued their bull run, led by Italy’s four basis points decline to 2.10%, a new low and 15 bp drop in Greece (to 2.35%). The US 10-year yield that dipped below 2.0% in the middle of last week before closing the week at 2.05% is a touch lower at 2.04%. The US dollar is sporting a softer profile against most of the major currencies, but the Japanese yen, which is little changed. Most emerging market currencies, led by the 1.3% rally in the Turkish lira, are mostly firmer. The Chinese yuan is an exception. It is fractionally lower with the dollar a little below CNY6.88. Before the weekend, it briefly traded near CNY6.8350, its lowest level in over a month. Oil and gold are extending pre-weekend gains. |

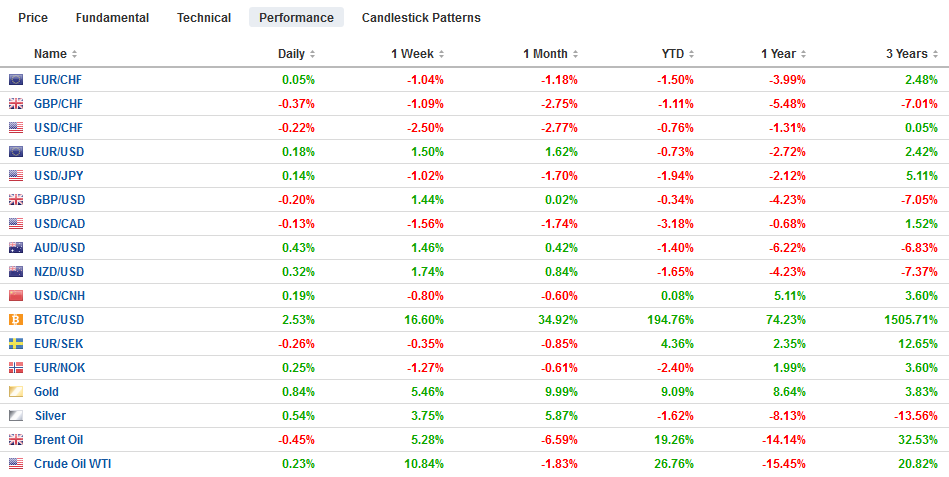

FX Performance, June 24 - Click to enlarge |

Asia Pacific

The focus is on Trump’s meeting with Xi at the G20 meeting later this week and if trade talks between the two largest economies can resume. We suspect the most that can be reasonably hoped for is another tariff truce and a new attempt to work out an agreement. However, the US is going forward, adding more companies involved with China’s supercomputer work to the blacklist preventing US companies from selling or buying from them. At the same time, Trump’s trade adviser Navarro reiterated the President’s claim that China is paying for the tariffs, by which it seems he means through lower demand for their products (weaker exports) and encouraging businesses to relocate out of China. Navarro also claimed that China is weakening the yuan to offset the tariffs, which most observers, including ourselves dispute.

The US is also in trade negotiations with Japan. Reports suggest Japan is pressing the US to eliminate its agriculture barriers, including rice and beef. This is a twist in the plot as the US has been pressing Japan to grant the US the same terms on agriculture trade that were granted Japan’s partners in the TPP and with Europe.

The market appears to have discounted around an 80% chance that the Reserve Bank of Australia cuts its cash rate target to a record low of 1.0% next week. This has not stopped the Australian dollar from extending its rally for the fifth consecutive session today, which appears to be the longest rally since the end of 2017. Today’s spark may have been comments from the central bank, Governor Lowe, who recognized the limitations of monetary policy. That said, the market is pricing in another cut after next week’s anticipated move in Q4.

The Aussie and Kiwi are the strongest of the majors through the European morning, gaining about a third of a cent against the US dollar. After stalling near $0.6935 in the last two sessions, the Australian dollar has been bid to $0.6960 before steadying. Initial support is seen near last week’s highs, which also corresponds to the 20-day moving average. The bottoming pattern that has been carved provides an initial target near $0.7000-$0.7030. The dollar is trapped in a 20-range against the yen (~JPY107.30-JPY107.50). Expiring options (~$370 mln at JPY107 and $1.3 bln at JPY107.50) may help continue to curtail the price action. That said, the intraday technicals favor the greenback’s upside, and the JPY108 area offers more formidable resistance.

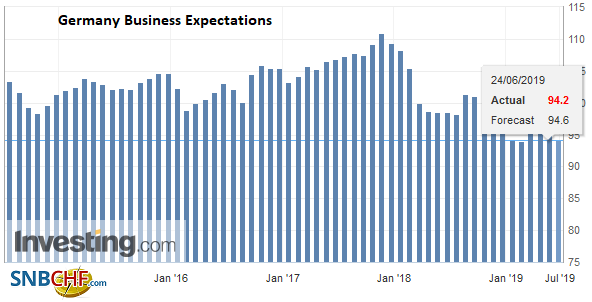

GermanyA disappointing German IFO survey did not prevent the euro from extending its recent gains to approached $1.14 for the first time in three months. The IFO survey showed that the current assessment edged slightly higher (100.8 from a revised 100.7–initially 100.6, a two-year low), but the expectations component continued to deteriorate (94.2 from a revised 95.2–initially 95.3). |

Germany Business Expectations, June 2019(see more posts on Germany Business Expectations, ) Source: Investing.com - Click to enlarge |

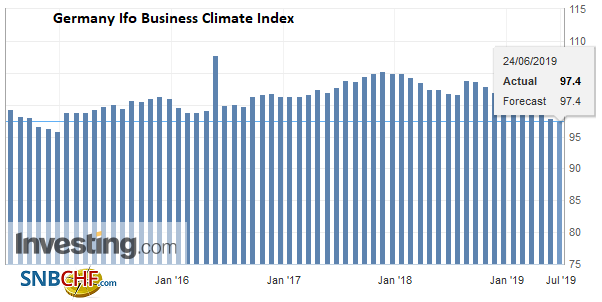

| In February the IFO expectations reached a seven-year low of 94.0. The overall assessment of the business climate fell to a new five-year low of 97.4 in June. The head of the IFO himself was pessimistic, warning that there were no green shoots in manufacturing and the economy was headed for the “doldrums.” |

Germany Ifo Business Climate Index, June 2019(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

Personal problems of Johnson is threatening to undermine his bid to become the new Tory Party leader. In one survey (The Daily Mail) showed Johnson slipping behind Hunt, while another (Sunday Telegraph) showed Johnson holding on to a lead. It will take a better part of the next month for the Tory rank-and-file to vote. Both Johnson and Hunt Brexit strategies are predicated on re-negotiating the Withdrawal Agreement with the EU. Even in the EC was willing to do this, which it is not, it gives the next leader, assuming he can survive a vote of confidence, three months best ahead of the October 31 deadline.

The opposition candidate (Imamoglu) won for the second time to become Mayor of Istanbul. President Erdogan, who was born in Istanbul, resisted the results of the March election and won the re-do, but his candidate lost the election again. Many see this as a decline of Erdogan’s broader support. Turkey’s stocks advanced by about 2%. Its 10-year bond yield is off around 55 bp to almost 15.25%, and the lira has gained 1% against the dollar (~TRY5.7560 after seeing TRY5.7130 earlier). The risk is that the market may be getting ahead of itself. Erdogan will not be deterred by the results and the confrontation with the US over the planned deployment of a Russian anti-aircraft system is not over.

The euro is flirting with the upper Bollinger Band (two standard deviations above the 20-day moving average) that is found just below $1.14. There are around 1.5 bln euros in options between $1.1395 and $1.1400 that will expire today. This may encourage some caution from North American dealers, who will inherit the book with the euro near session highs and intraday technicals a bit stretched. Support is pegged near $1.1360 today. The next upside target is the March high near $1.1450. Sterling has firmed to a new high for the month a little above $1.2765. Its gains seem to reflect dollar weakness more than sterling strength as it is trading heavier on the crosses, including against the euro. Resistance is seen near $1.28.

America

In recent days, the US has confirmed that it is using cyberweapons against Russia and Iran. It is little wonder that today Russia indicated it will support Iran and help it overcome US sanctions. China is thought to be circumventing the US embargo against Iran for gas and possibly oil as well. Meanwhile, many are concerned that the US public admission will spur an escalation of cyberwarfare and are concerned in particular that Iran will strike back in some fashion.

The US sees the Dallas Fed manufacturing survey. The Empire State and Philly Fed surveys for June disappointed, suggesting the US economy lost some momentum as Q2 winds down. The Chicago Fed’s national activity survey (May) is likely to remain in negative territory where it has been in three of the first four months of the year. Through April it averaged -0.295. In the same period last year, it averaged 0.285. Tomorrow Fed Chairman Powell speaks, as do four other Fed officials. The market has a 25 bp cut fully discounted, but the pricing of the fed funds futures contracts suggest that nearly a 30% chance of a 50 bp cut is priced in, and that is where we suspect Powell’s comments will impact. He is unlikely to show the kind of urgency that is consistent with a 50 bp move. The Canadian and Mexican economic calendars are sparse.

The US dollar is trading inside the pre-weekend range against the Canadian dollar, which was inside the previous session’s range, illustrating the consolidative tone. Initial resistance is seen around CAD1.3230. Support is pegged near CAD1.3150, but CAD1.3100 is likely stronger. The Mexican peso is little changed and also is in a consolidative mode. The dollar spiked to almost MXN18.89 last week, the day after the Fed’s statement and reached MXN19.16 ahead of the weekend. The MXN19.20 area may be sticky. Without a recovery today, it will be the second consecutive close of the Dollar Index below its 200-day moving average (96.65) since April 2018. Note that it is poised to begin the North American session near 96.00, where the lower Bollinger Band is found.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,China,EUR/CHF and USD/CHF,Featured,Germany,Germany Business Expectations,Germany IFO Business Climate Index,Iran,newsletter,Russia,Turkey