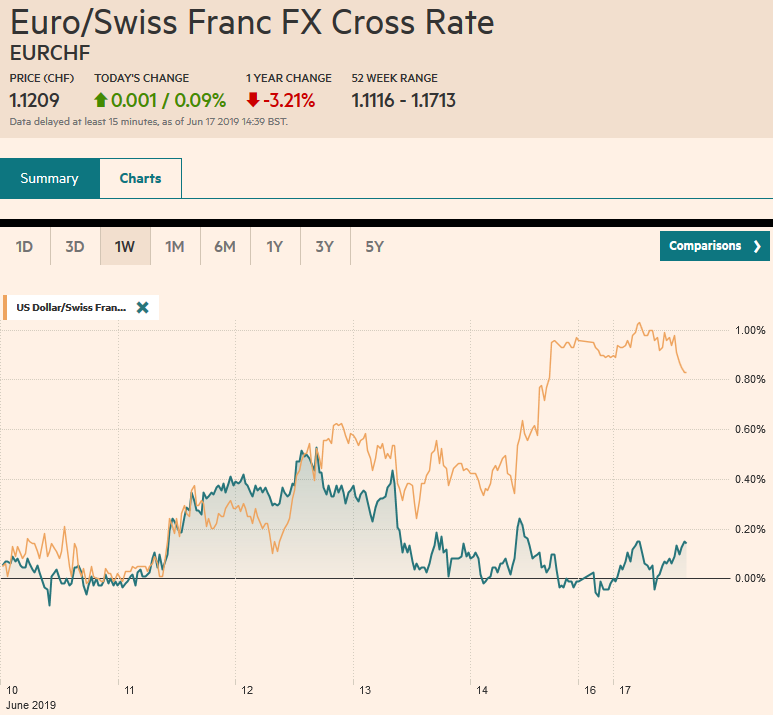

Swiss Franc The Euro has risen by 0.09% at 1.1209 EUR/CHF and USD/CHF, June 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The global capital markets are off to a subdued start to what promises to be a busy week, featuring the FOMC, BOE, BOJ meetings, and the flash June PMIs. Investors also expect some signal whether Presidents Trump and Xi will at the G20 meeting later this month. Asian equities were narrowly mixed. Hong Kong’s Hang Seng gained 0.4% despite continued protests seeking the termination of the extradition measure not just the suspension of its consideration, and the resignation of Chief Executive Lam. Indian shares led the decliners with a

Topics:

Marc Chandler considers the following as important: 4) FX Trends, Featured, Hong Kong, India, newsletter, Singapore, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.09% at 1.1209 |

EUR/CHF and USD/CHF, June 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The global capital markets are off to a subdued start to what promises to be a busy week, featuring the FOMC, BOE, BOJ meetings, and the flash June PMIs. Investors also expect some signal whether Presidents Trump and Xi will at the G20 meeting later this month. Asian equities were narrowly mixed. Hong Kong’s Hang Seng gained 0.4% despite continued protests seeking the termination of the extradition measure not just the suspension of its consideration, and the resignation of Chief Executive Lam. Indian shares led the decliners with a nearly 1% loss to test key chart support. European bourses struggling to stay in the green. The Dow Jones Stoxx 600 gained about 0.35% last week and is up about 0.1% in late morning dealings, led by the financial sector and real estate. Energy, utilities, and health care were among the weakest sectors. US shares are trading fractionally higher. Benchmark 10-year yields have edged higher. Italy is the main exception as its benchmark is four basis points lower. An index of Italian bank shares broke a five-week slide last week with around a 0.5% gain and is up about 0.6% today. The US dollar approach key retracement objectives ahead of the weekend but is confined to narrow ranges with a small downside bias today. Among the emerging market currencies, Turkish lira (+~0.25%) is leading the minor gains, following the decision to exempt exporters from the foreign currency transaction fee. Gold and oil are seeing their pre-weekend gains pared. |

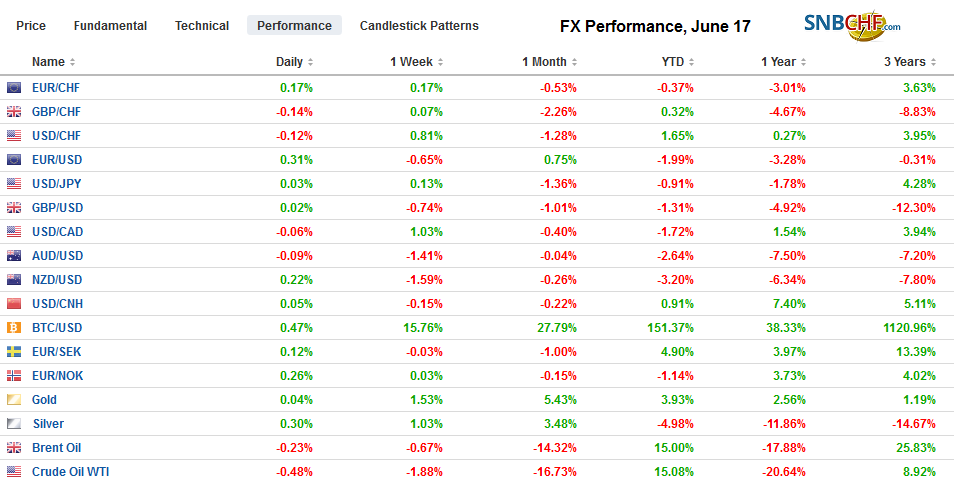

FX Performance, June 17 - Click to enlarge |

Asia Pacific

Hong Kong officials suspended the controversial extradition law, but it was insufficient to end the protests, which are calling for Lam’s resignation. Although the public outrage appears to have won the battle, the larger issue of the special administrative region’s independence is not resolved. There is also a real and practical issue: A person commits a crime in China and flees to Hong Kong. Currently, China cannot extradite the person. At the same time, people are rightfully concerned that the simply authority can be applied broadly, even though the bill precluded extradition for political crimes. Many of the same issues about the future of Hong Kong’s relative independence arose during the Umbrella Movement (protest of the selection process for the Chief Executive) lasted much of Q4 2014. The challenge to Hong Kong’s rose as a financial center appears somewhat exaggerated, though over time, it seems broadly recognized that Shanghai will eclipse it.

As a financial and commercial center, what happens in Singapore is often reflective of broader economic trends. The city-state report May export figures, confirming that the regional adjustment continues. Non-oil exports fell by double-digits, year-over-year for the third consecutive month (-15.9% after a 10% fall in April, and -11.8% in March). A Reuters poll found a median forecast for a 16.5% decline. Electronics is an important culprit. Electronic exports plunged 31.4% year-over-year after a 16.3% decline in April. Exports to China and Hong Kong were off 23.3% and 24.8% respectively, but double-digit declines were experienced broadly (e.g., Japan, Taiwan, and the EU). The US was the exception. Singapore exports to the US rose by 0.2%.

The combination of the US steel and aluminum tariffs and the removal of its preferential trade status by the US has seen India retaliate with tariffs on 28 US products which it imports. The tariff on some products, like apples and almonds are as high as 70%. The US Secretary of State is due to visit India later this month. He seemed to hold out the potential for a resolution. Meanwhile, the late monsoon is raising questions about the government’s ability to stimulate the economy.

The dollar has been mostly confined to a 15 tick range on either side of JPY108.55. Last week’s high was near JPY108.80, and it did not trade below JPY108.15. A move above JPY109 is needed to lift the dollar’s tone. Optionality may protect the downside. There is a $675 mln option at JPY108.25 that will be cut today and a $2.6 bln option at JPY108.00 that expires in the middle of the week. The Australian dollar is consolidating the pre-weekend losses and is in less than a 20 tick range, holding above the $0.6860 level approached at the end of last week. The Chinese yuan edged slightly lower.

Europe

The next narrowing of the field for the next Tory leader will take place tomorrow. Johnson did not participate in the debate among the other candidates, but this did not appear to cost him. Observers and betters have long seen Johnson as May’s successor. What ultimately at stake now is second place, as the rank and file will get to choose between the two candidates that the members of parliament select. Johnson, like others, wants to renegotiate the Withdrawal Agreement, but the EC has rejected this appeal. Johnson, like, others, threaten to leave without an agreement at the end of October. While the no-deal Brexit, which some are trying to rename the WTO deal, is understood to be disruptive to the EU, many see it as being a greater disturbance for the UK, and its immediate neighbors, especially Ireland. The BOE may talk hawkishly but it cannot deliver tighter monetary policy in this environment.

The fallout from the resignation of the French candidate to succeed Junker has yet to be fully digested. The two main groupings in the EU Parliament, the center-right and center-left failed to secure a combined majority for the first time and need a third party. The pro-business liberals are the likely group and the French candidate Loiseau was seen as a compromise candidate to be the next EC President. This would seem to increase the likelihood that the center-right’s Weber from German gets the nod. However, in the horse-trading that goes on, it would seem to increase the pressure France will exert to secure the ECB Presidency (for technical reasons, de Galhau, the current head of France’s central bank appears more likely the current executive board member Coeure). If Merkel pushes hard, the compromise candidate may still be a Finn.

The euro has held above $1.1200, an important chart point and the site of an 850 mln euro option that is expiring today. Yet it has not been able to make much headway and has been capped at $1.1225. It is hard to get excited the euro ahead of the outcome at the middle of the week of the FOMC meetings. Calls for a rate cut this week were re-thought after the firm retail sales and industrial production data released before the weekend. Sterling slipped to a marginal new low for June just above $1.2570. The low from the end of May (~$1.2560) was the low point since the flash crash (~$1.2440).

America

With today’s Empire State manufacturing survey, insight into how the world’s biggest economy is finishing, Q2 will begin being reported. However, the focus is squarely on trade and the Fed. Public hearings on Trump’s threat to impose 25% levies on the remaining $300 bln of so of Chinese imports begins today. More than 600 companies and industry groups have signed a letter opposing the tariffs. About 20% of the goods that would face the new tariff account for around 90% of the US imports of 273 product categories, suggesting there may not be an immediate alternative.

Press reports have highlighted Vice President Pence’s speech next Monday at the Wilson Center. Apparently, hopes for a Trump-Xi meeting may have tempered the speech that commemorates the Tiananmen Square Massacre. If the speech is as aggressive as some of Pence’s speeches have been, it will be seen as a sign that Xi and Trump will not meet and an escalation is likely.

Canada reports May CPI and April retail sales later this week. There are few fresh incentives today, and the US dollar is trading in a 10 pip range around CAD1.3410. The CAD1.3435 is a (61.8%) retracement of the decline seen earlier this month. The Mexican peso is quiet as well, trading comfortably within the pre-weekend range (~MXN19.11-MXN19.23).

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Featured,Hong Kong,India,newsletter,Singapore