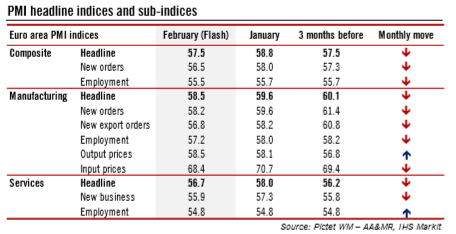

The IHS Markit flash composite purchasing managers’ index (PMI) for the euro area eased to 57.5 in February from 58.8 in January, below consensus expectations (58.4). The index marked its the largest monthly decrease since August 2014. Activity in both services PMI (-1.3 points to 56.7) and manufacturing (-1.1 points to 58.5) cooled in February. But while the breakdown by sub-indices showed that the pace of growth in new orders and output slowed (see Table), it remains close to record highs, and consistent with solid growth. Momentum in job creation remained brisk, with Markit mentioning that “new business was sufficiently strong to encourage companies to boost staffing levels to one of the greatest extents seen

Topics:

Nadia Gharbi considers the following as important: Featured, Macroview, newslettersent, Pictet Macro Analysis, Swiss and European Macro

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

| The IHS Markit flash composite purchasing managers’ index (PMI) for the euro area eased to 57.5 in February from 58.8 in January, below consensus expectations (58.4). The index marked its the largest monthly decrease since August 2014. Activity in both services PMI (-1.3 points to 56.7) and manufacturing (-1.1 points to 58.5) cooled in February. But while the breakdown by sub-indices showed that the pace of growth in new orders and output slowed (see Table), it remains close to record highs, and consistent with solid growth. Momentum in job creation remained brisk, with Markit mentioning that “new business was sufficiently strong to encourage companies to boost staffing levels to one of the greatest extents seen over the past 17 years”. Capacity continued to show signs of being stretched, but to a lesser extent than in previous months, “reflecting the combination of recent hiring and slower inflows of new work”, according to Markit. Price pressure remained elevated in February. |

Euro Area PMi Indices, Dec 2017 - Feb 2018 - Click to enlarge |

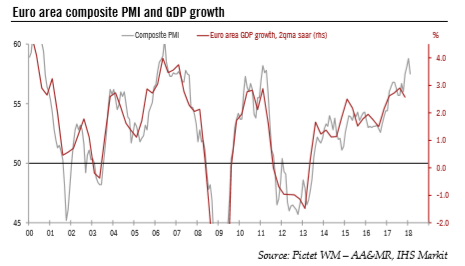

| Overall, average (January and February) composite PMI points to solid growth in Q1 of close to 0.9%, accelerating from the quarter-over-quarter (qo-q) rate of 0.6% posted in Q4 2017. That said, the fall in forward-looking indices is consistent with our forecast of a gradual slowdown in the pace of growth in the euro area in the second half of 2018. Still, February PMIs confirm that growth is improving in terms of quantity as well as quality, with job creation and investment continuing to improve. We forecast euro area GDP growth of 2.3% in 2018, after 2.5% in 2017. |

Euro Area Composite PMI and GDP Growth, 2000 - 2018 - Click to enlarge |

The French PMI indices eased in February after having reached cyclical highs between November (for services) and January (for manufacturing). The composite PMI index dropped from 59.6 to 57.8 in February, a four-month low, with the slowdown broad based across sectors. At first sight, business sentiment would seem to be signalling a modest slowdown from the pace of GDP growth recorded in Q4 2017 (+0.6% q-o-q), although activity expansion is likely to remain fairly sustained overall. Last year, France posted its strongest growth rate in six years (1.9%). Looking at PMI details, the February setback was led by weaker output growth and new orders. However, the rate of job creation accelerated in February, coming close to the November 2017 peak (which saw the highest monthly rise in employment since 2000), while Markit noted that “another marked accumulation of unfinished work suggests that further jobs growth is likely in the months ahead”.

In Germany, the flash composite PMI index fell to 57.4 in February from 59.0 in January, below consensus expectations (58.5). In contrast with France, the main hit in Germany came from the services PMI (-2.0 points to 55.3). Manufacturing PMI cooled down as well, but to a lesser extent (-0.8 points to 60.3). The breakdown by sub-indices showed that new orders growth was strong in both services and manufacturing, but fell noticeably from the brisk pace set the previous month. On a more positive note, the degree of optimism about future business activity reached its highest point since July 2012. But whereas there was a marked improvement in future expectations in the services sector, German manufacturers were less optimistic. Momentum in employment remained brisk in February, while delivery times lengthened further. Importantly, inflation pressures continued to mount. Overall, the February PMI reading for Germany was still among the highest seen since early 2011 and continues to point to robust private-sector expansion. Firms remain strongly optimistic about 2018 despite lingering political uncertainty.

Outside the two largest euro area countries, Markit noted that “business activity growth meanwhile also slowed across the rest of the eurozone, though still registered the second-largest expansion in nearly 12 years”.

Tags: Featured,Macroview,newslettersent